- Concerns emerge over potential price drops as imports rise

- Trading activity expected to slow ahead of festive season

India’s stainless steel (SS) finished flats and longs prices remained stable w-o-w amid muted trading activity, particularly in the longs segment.

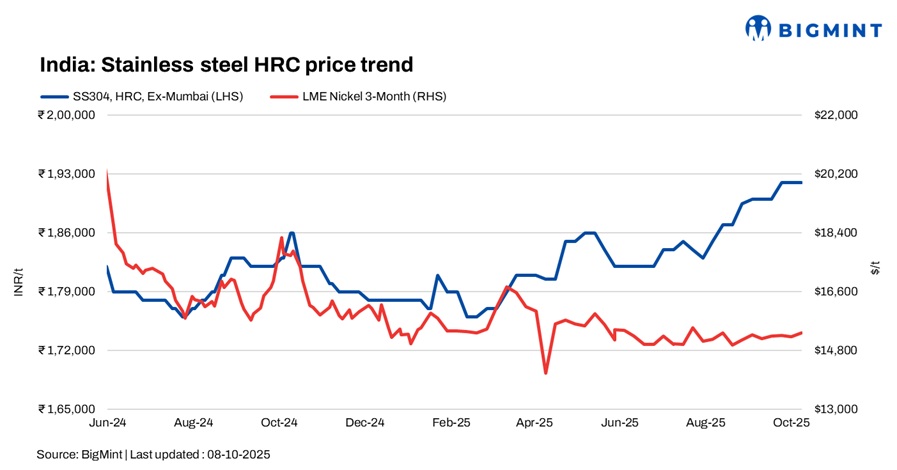

BigMint assessed 304-series hot rolled coils (HRCs) at INR 192,000/t ex-Mumbai, unchanged w-o-w, while 304L black round bars (25-100 mm) also remained stable at INR 160,000/t. In contrast, 316-series hot-rolled coils (HRCs) stood steady at INR 345,000/t and cold-rolled coils (CRCs) were firm at INR 351,000/t w-o-w.

Additionally, the Ministry of Steel has granted a temporary exemption from mandatory BIS certification for stainless steel flat products under IS 6911, IS 5522, and IS 15997 until 31 December 2025. The decision, issued on 6 October 2025, aims to ease import disruptions and address limited domestic supply, especially in 200 and 300 series stainless steel grades.

Market sentiments

Demand remained weak overall. According to market participants, “The stainless steel finished flats segment is expected to remain largely stable, with some relief for importers sourcing from BIS-approved firms. However, concerns persist over a possible price correction as imports and material inflows increase. Prices may see a marginal decline of around INR 2,000-3,000/t this week, with improving supply and cautious market sentiment.”

Another source noted, “Overall, the finished longs segment has underperformed this year, with exports remaining subdued. However, domestic demand has shown notable improvement over the past couple of weeks, driven by seasonal restocking and project-related buying ahead of the Diwali festive period.”

Global SS market sentiment

Taiwan’s stainless steel export offers surged during China’s National Day holiday, driving up Asian CRC prices. With China’s market closed, Taiwan leveraged the opportunity to lift prices. However, overall demand across Asia remained subdued, as buyers limited purchases to immediate needs. China’s nickel pig iron prices stayed firm, supported by steady raw material costs. Market participants expect stainless steel prices to remain volatile in the near term amid weak downstream demand and cautious buying activity.

Global SS finished longs indicative offers

Indicative FOB prices for stainless steel longs, with India’s 304 bright bars at $2,050-2,100/t and 316 bright bars at $3,600-3,650/t, while Vietnam’s 304 bright bars are quoted at $1,880-1,950/t and 316 bright bars at $3,440-3,450/t. On the other hand, Europe domestic stainless steel 304 bright bars indicative levels were heard at $2,800-2,850 and 316 bright bars were heard at $4,000-4,300/t.

LME nickel tags remain largely stable w-o-w

At the time of reporting, three-month nickel prices on the London Metal Exchange (LME) stood at $15,355/t, up by $120/t compared to last week’s $15,235/t. Nickel stocks at LME-registered warehouses stood at 231,630 t, up 0.5% compared to 231,312 t in the previous week.

Raw materials scenario

Ferro molybdenum: Indian ferro molybdenum prices stayed range-bound this week, declining marginally by INR 36,000/t ($405/t) in comparison to the previous assessment on 1 October. Regular domestic trades, along with unchanged market sentiments, kept prices largely steady.

As per BigMint’s assessment on 8 October, ferro molybdenum prices in India were at INR 3,032,000/t ($34,150/t) exw.

Ferro chrome: Indian high-carbon ferro chrome (HC-60%) prices dropped by INR 200/t w-o-w to INR 118,500/t ($/t) exw-Jajpur.

Ferro silicon: Indian ferro silicon (70%) prices dropped by INR 1,300/t ($15/t) as compared to the previous assessment on 29 September. The decline was primarily driven by most sellers adjusting their offers to Bhutan’s October 2025 prices of INR 87,000/t ($980/t) exw.

As per BigMint’s assessment on 6 October, ferro silicon prices in India were at INR 87,000/t ($981/t) exw-Guwahati. In Bhutan, prices inched down by INR 600/t ($7/t) w-o-w to INR 87,400/t ($985/t) exw.

Ferrous scrap: India’s imported scrap market remained largely muted throughout the week, with offers holding steady across origins. Shredded was quoted around $360/t CFR, HMS 80:20 near $330-335/t, busheling at $370-375/t, and PNS at $360-370/t, though workable bids were consistently below these levels. Market sentiment was weighed down by sluggish finished steel demand, cheaper domestic scrap (about INR 1,500-1,800/t lower than imports), and seasonal disruptions from monsoon rains.

Outlook

The stainless steel market is likely to remain subdued in the coming days, as trading activity slows ahead of the festive season. Overall, market participants maintain a cautiously optimistic outlook, expecting stability in prices with limited movement until post-festival demand resumes.

Leave a Reply