- European Commission sets annual quota at 18.3 mnt

- Imports exceeding these volumes to attract 50% duty

The European Commission has proposed a new regulation to replace the existing steel safeguard mechanism, aiming to strengthen protection for the EU steel industry amid mounting global overcapacity and trade distortions. The new framework, announced on 7 October 2025 in Strasbourg, will take effect after the current safeguard expires on 30 June 2026.

Structured tariff quota system

Under the proposal, the existing safeguard mechanism would transition into a tariff rate quota (TRQ) regime covering 28 steel product categories, including flat, long, and tubular products. The total annual quota is fixed at around 18.3 million tonnes (mnt), benchmarked to 2013 import levels and 2024 consumption patterns. Imports exceeding these volumes will attract a 50% ad valorem duty, double the current out-of-quota rate.

Quotas will be administered quarterly to prevent front-loaded import surges, with no carry-over of unused allocations. Exemptions are extended to Norway, Iceland, and Liechtenstein under EEA provisions, while imports from Russia and Belarus remain excluded due to ongoing sanctions.

The full TRQ list covers 28 steel product categories, as detailed in the annexe.

Transparency, traceability

A key feature of the new framework is the mandatory “melt and pour” origin declaration, requiring importers to disclose the country where the steel was originally produced. This measure seeks to curb circumvention through re-rolling or minimal processing in third countries — a persistent loophole under current safeguards.

Market context, rationale

Global crude steel overcapacity is projected to rise from 602 million tonnes (mnt) in 2023 to 721 mnt by 2027, primarily driven by expansion in Asia and the Middle East. With other major economies — notably the US and China — maintaining their own restrictive trade policies, the EU market faces heightened exposure to diversionary inflows.

The European steel sector has witnessed a steady erosion of competitiveness, with crude steel production declining by over 30 mnt since 2018. Capacity utilisation has dropped to 67%, reflecting weaker operational efficiency. Elevated energy costs, carbon compliance expenses, and sluggish demand recovery have further constrained margins and delayed investment in green steel projects.

Policy alignment

The proposed regulation supports broader EU strategies such as the Steel and Metals Action Plan (SMAP), Competitiveness Compass, and ReArm Europe Plan, emphasising industrial resilience, defence readiness, and low-carbon transformation. It also reinforces the EU’s objective of maintaining strategic autonomy in critical industrial inputs.

Industry response, economic impact

The proposal follows an extensive consultation process involving over 500 industry participants, including producers, traders, and associations. While the Commission has not released a full impact assessment, a Staff Working Document provides analytical backing for the regulation. Market participants have generally welcomed the continuity and predictability offered by the quota-based system, though concerns persist regarding administrative complexity and potential cost pass-through for downstream users.

The regulation is expected to generate additional customs revenue from out-of-quota imports, though the magnitude will depend on import trends and quota utilisation rates. An initial performance review is slated for July 2031, with subsequent evaluations every five years.

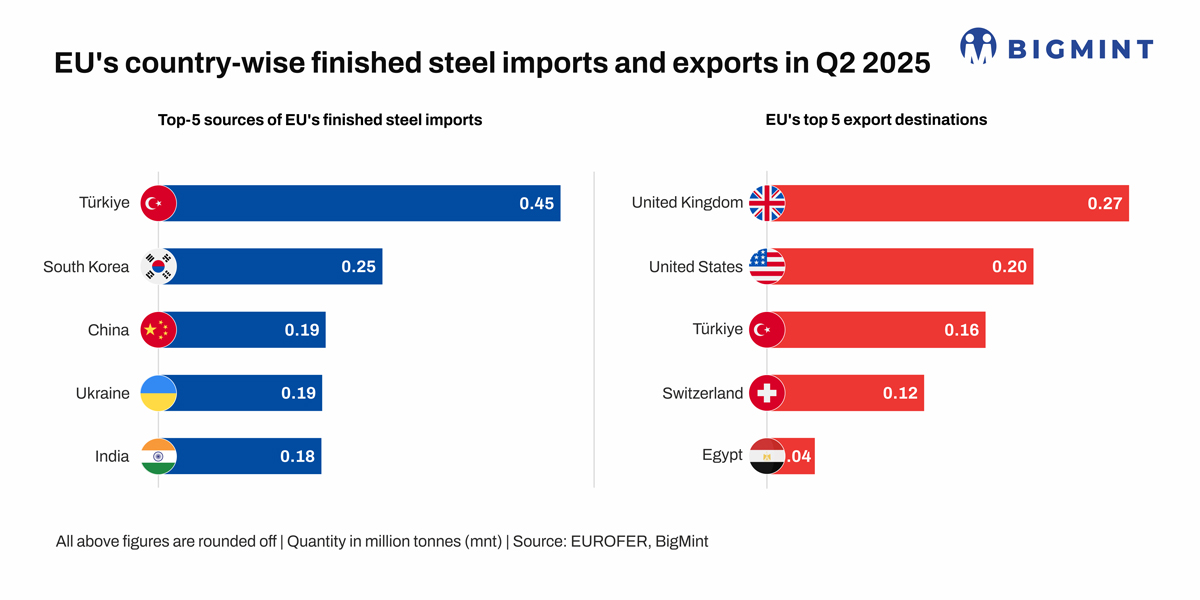

Imports

Steel imports (including semis) edged down by 3% y-o-y in Q2CY’25, following a 1% drop in the preceding quarter. Flats imports decreased by 9%, while longs were down by 2%. Despite the overall decline, imports remained elevated, accounting for 25% of apparent steel consumption.

Leading finished steel exporters into the EU were Turkiye (41% increase y-o-y), South Korea (-16%), China (+11%), Ukraine (+44%), India (-50%), and Taiwan (-17%).

Outlook

The EU’s move underscores a decisive policy shift from short-term safeguard extensions to a long-term, rules-based protection mechanism. For global trade flows, this could reshape traditional supply routes — particularly for hot-rolled coils, coated flats, and rebars — while tightening compliance obligations for exporters targeting the European market.

Given the EU’s sizeable import footprint, the regulation’s implementation could influence price differentials across major export origins, including India, Turkey, and Vietnam, where producers may face reduced flexibility in shipment scheduling. Market observers expect the new quota system to temper import-driven price volatility and stabilise regional spreads in the medium term.

Leave a Reply