- Sep’25 sees slow demand, oversupply amid festive period

- Cautious market sentiment may continue in short term

Leading Indian steel manufacturers have decreased the prices of hot-rolled coils (HRCs) and cold-rolled coils (CRCs) by INR 750-1,500/tonne (t) ($8-17/t) for October 2025 sales as compared to the list prices of early-September 2025. However, from the net sales prices of end-September, prices have been raised by around INR 500/t ($6/t) for October 2025.

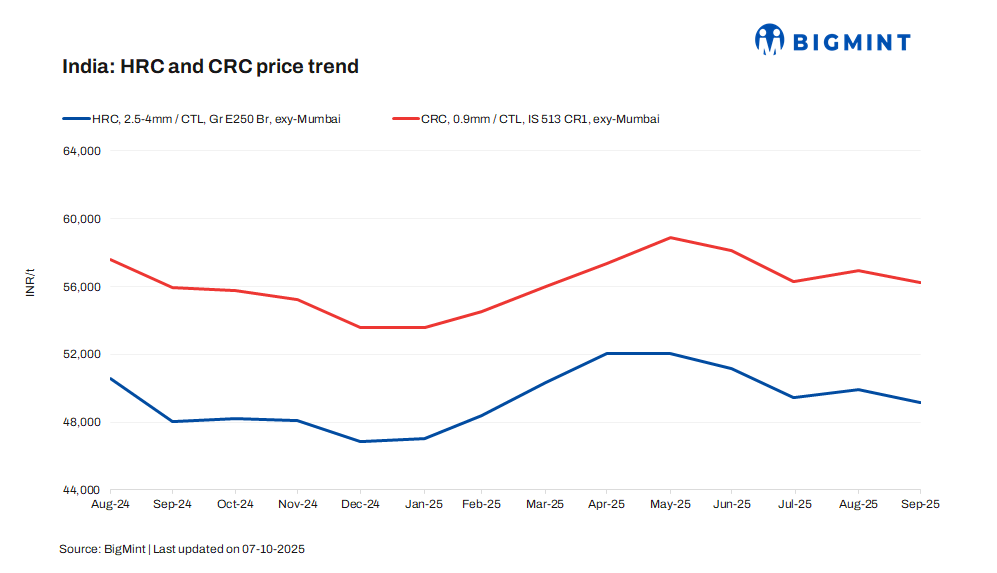

List prices of HRCs (2.5-8 mm, IS2062, Gr E250 Br) ranged within INR 49,400-50,500/t ($557-569/t) ex-Mumbai. CRCs (0.9 mm, IS513 CR1) were listed at INR 54,900-57,250/t ($619-645/t).

BigMint’s benchmark assessment (bi-weekly) for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) dropped by INR 200/t ($2/t) w-o-w to INR 48,300/t ($544/t) on 7 October 2025 against INR 48,500 ($546/t) on 30 September 2025. Moreover, CRC (IS513, Gr O, 0.9 mm/CTL) prices fell by INR 200/t ($2/t) w-o-w to INR 55,700/t ($628/t) on Tuesday against INR 55,900/t ($630/t). These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

On an m-o-m basis, trade-level prices of HRCs fell by INR 800/t ($9/t) to INR 49,100/t ($553/t) in September 2025 against INR 49,900/t ($562/t) a month ago. Similarly, CRC prices fell by INR 600/t ($6/t) to INR 56,300/t ($635/t) in September 2025 against INR 56,900/t ($641/t) in August 2025.

Factors behind reduction in prices

Slow demand amid festive lull: India’s HRC market remained subdued in September as sluggish demand, oversupply, and high inventories pressured prices. Buyers limited purchases to immediate needs, avoiding bulk bookings. Thin margins, heavy stocks, and festive holidays such as Durga Puja further dampened trading activity and delayed recovery prospects.

Raw material price uncertainty: The proposed export duty on iron ore remains undecided, creating uncertainty around raw material costs and adding near-term volatility to steel price expectations.

Import, export volumes

Import volumes: India’s bulk imports of HRCs touched 464,694 t as of 30 September 2025, based on vessel line-up data. Around 144,709 t of additional cargoes are expected by the first week of October.

Export volumes: India’s bulk exports of HRCs touched 203,541 t as of 30 September 2025, based on vessel line-up data with BigMint. Around 10,000 t of additional cargo are in transit.

Outlook

The Indian HRC market is likely to remain in a wait-and-watch mode as the market adjusts to mills’ revised pricing. The post-festivity demand recovery in early October has been sluggish, with buyers remaining cautious due to high inventory levels and muted trading sentiment, which is delaying any notable price movement. However, towards the end of October, a demand revival can be expected as market activity normalises, and activities may pick up post-festivities.

Leave a Reply