- Mill procurement stalls, liquidity issues keep buyers cautious

- Mills operating at 35-40% capacity amid weak rebar demand

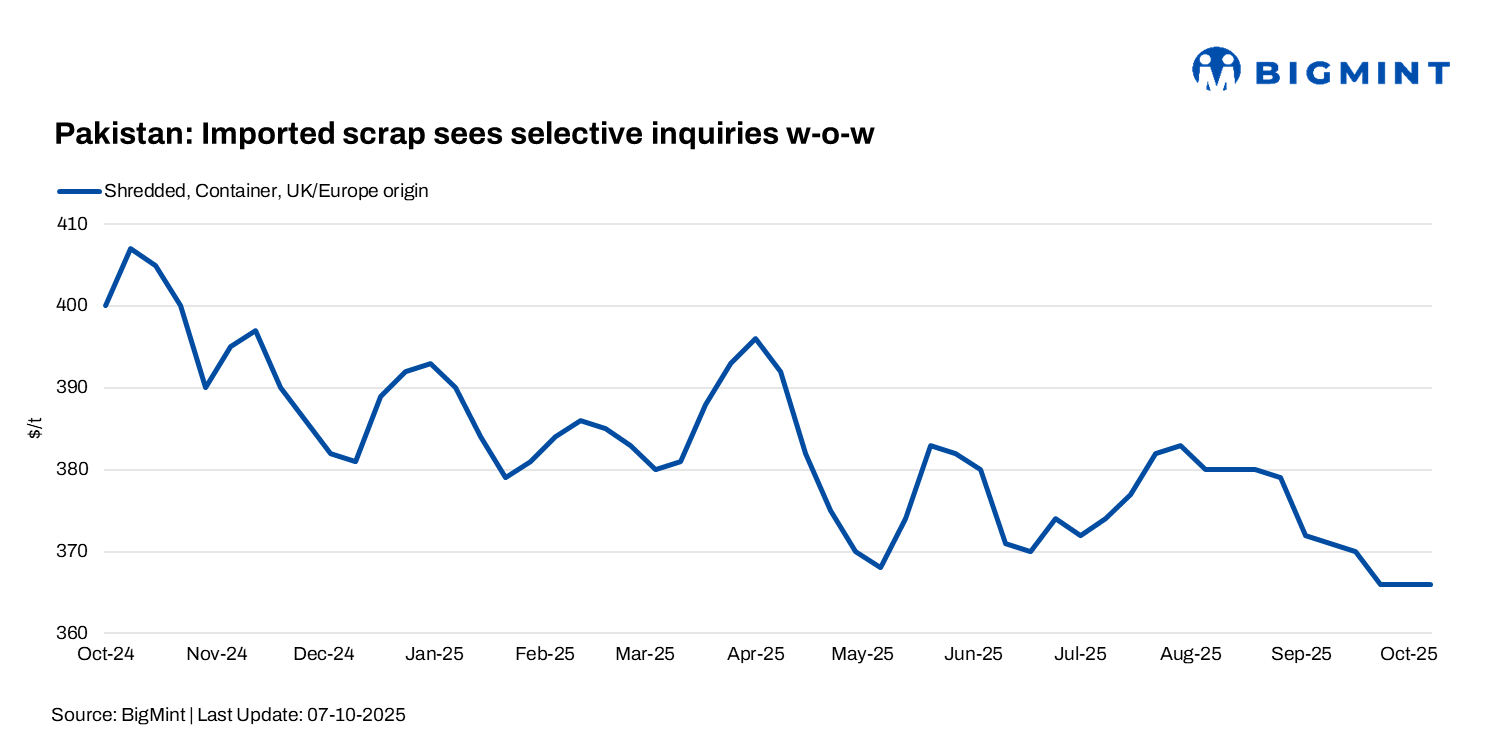

Pakistan’s imported scrap prices remained stable w-o-w amid limited inquiries. EU/UK shredded scrap hovered within $365-370/t CFR Qasim, with UAE material slightly higher at $385-388/t amid limited deals. Mills operated at 35-40% capacity, with weak steel demand and falling rebar prices curbing buying. Some participants offered shredded as low as $362-363/t, citing halted mill procurement and increasing market pressure.

BigMint assessed European/UK-origin shredded at $366/t CFR Qasim, stable w-o-w.

Market comments

A Europe-based supplier informed BigMint that EU/UK shredded offers held steady at $365-370/t CFR Qasim as mills continued operating at just 30-35% capacity, with weak rebar demand and liquidity issues keeping buyers cautious. He added that HMS/PNS from the Middle East was heard at around $360-362/t CFR, but overall buying sentiment remained dull.

Recent trades include 3,000-4,000 t of EU/UK shredded booked at $366/t CFR Qasim. The market remained stable with limited fresh buying activity.

A UAE-based scrap supplier said no major trades were heard this week, with EU/UK shredded at $365/t CFR and UAE shredded at $385/t CFR. Domestic scrap was at around PKR 135,000/t ($477/t), bala at PKR 185,000/t ($655/t), billet at PKR 195,000/t ($690/t), and rebar at PKR 230,000/t ($814/t). He added that mill capacity utilisation remained low at 35-40% across major regions.

A Karachi-based mill source stated that domestic scrap was moving at PKR 135,000‑138,000/t ($474‑488/t), with rebar at PKR 230,000/t ($814/t), billet at PKR 195,000‑200,000/t ($690‑707/t), and bala at PKR 185,000‑188,000/t ($655‑667/t).

Gadani ship-recycling sector remains muted

At the Gadani ship-recycling yard, market activity remained subdued despite securing some handymax bulkers. Large LDT vessels such as Capes and Panamax have been largely avoiding Pakistani yards, often opting for India, even though Gadani offers the highest regional prices.

Yard upgrades are ongoing, but full HKC approval is still pending. Small LDT units faced pricing pressure due to delayed approvals, high financing costs, and currency volatility, keeping activity limited. Local steel plates held steady at ~$620/t, though the weakening PKR added pressure. Gadani received just 1,444 LDT this week versus 2,894 LDT previously, signalling a tight October supply.

Outlook

Market insiders indicate rising pressure, as most buyers remain inactive. Selective trades are being done, with some mills facing liquidity issues for fresh bookings. No price improvement is expected this week, and further declines seem likely.

Leave a Reply