- Weak demand, supply overhang weigh on market

- Monsoon disruptions, festive holidays curb trades

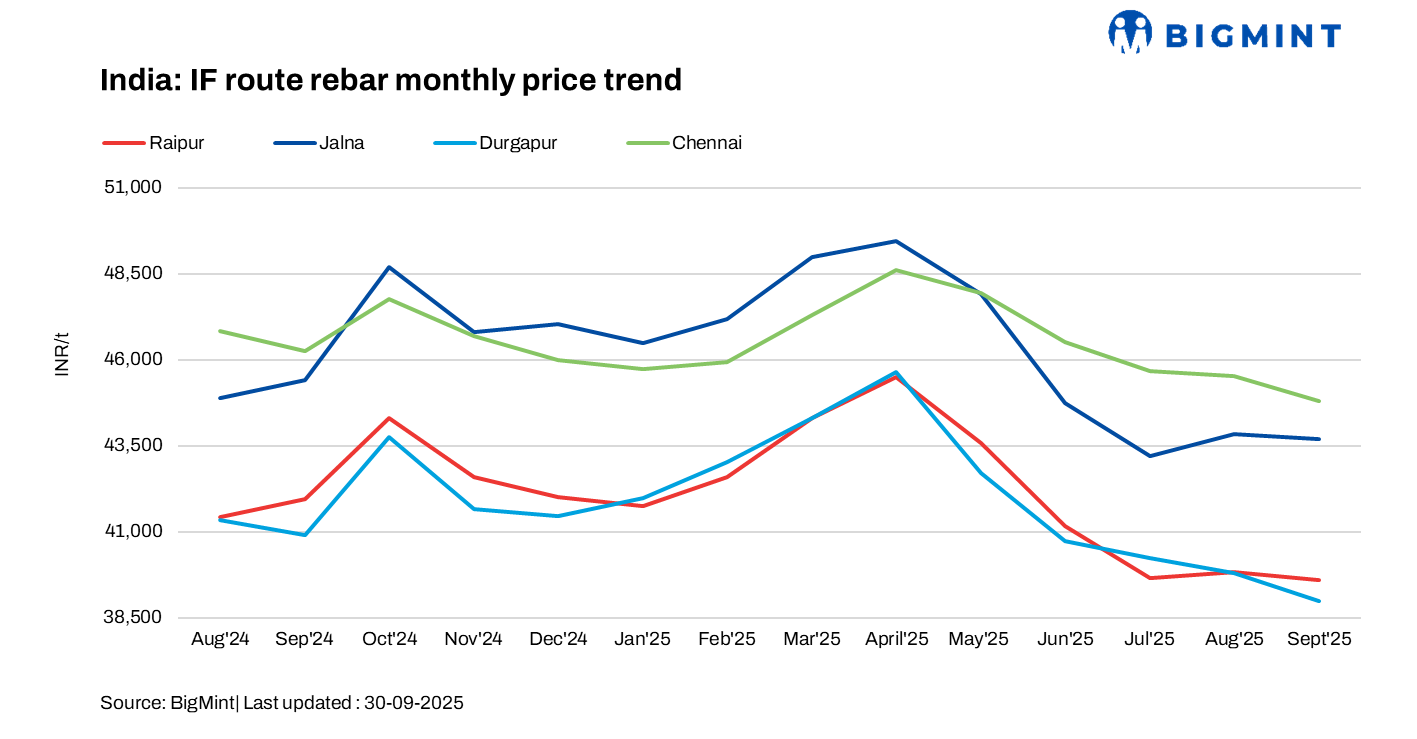

India’s induction furnace (IF) rebar prices witnessed a downtrend in September 2025, in the range of INR 100-1,800/tonne (t) m-o-m across regions, as per BigMint’s assessment.

Sluggish market conditions prevailed in the induction furnace route steel rebar sector as a result of dual pressures from ongoing festivals and heavy rainfall. This confluence of factors led to the closure of several markets and significantly pressured trading activity across the country. Consequently, buyers adopted a cautious procurement strategy, limiting purchases strictly to immediate requirements and eschewing large bulk orders.

This slow rate of material lifting ultimately resulted in an inventory buildup, with stock levels reportedly increasing from a typical 10–12 days supply to approximately 12–15 days.

As per Joint Plant Committee (JPC) data, India’s total rebar production through the IF and BF routes stood at 21.7 million tonnes (mnt) in April-August of FY’26, marking a significant 11% rise from around 19.6 mnt in the same period of FY’25, indicating continued growth momentum.

Region-wise price movements

Prices saw the most significant drop in the western region. The Mumbai market experienced a decrease of INR 1,800/t, while Ahmedabad saw a reduction of INR 400/t. South India, too, witnessed a notable price drop, with Chennai recording a reduction of INR 1,500/t and Hyderabad INR 1,000/t.

In central India, prices experienced an INR 300/t decline in Raigarh, while Raipur, a major production hub, saw a more modest decrease of INR 100/t m-o-m. Additionally, markets in northern India also saw a drop, with prices falling by INR 400/t in Delhi.

In east India, the same trends prevailed. Rourkela recorded a decline of INR 300/t, while the Durgapur market remained stable.

Factors impacting market

Raw material prices drop m-o-m: The drop in finished steel prices was largely driven by lower prices of key raw materials — steel billets and sponge iron — used in IF-route production. Dull buying interest and slow trade activity across markets prompted manufacturers to reduce their prices.

Considering Raipur as the benchmark, billet prices declined by INR 350/t m-o-m to INR 36,150/t exw, while sponge iron (PDRI FeM 80% ±1) saw a sharper decline of INR 1,000/t m-o-m to INR 24,100/t exw (prices taken from 30 August to 30 September 2025).

Market challenges: The extended monsoon severely curtailed construction activity, forcing buyers to restrict purchasing to immediate needs, thus leading to a rise in inventory levels. Market sluggishness was exacerbated by weak material lifting, tight payment cycles, and the disruptive effect of festive holidays. Additionally, submerged project sites and the uncertainty stemming from the GST rate cut for cement contributed to the subdued pace of material procurement.

BF-route rebar prices drop m-o-m: Trade level BF-rebar prices dropped by INR 1,000/t m-o-m to an average of INR 47,100/t exy-Mumbai amid subdued domestic demand in September. Domestic steel demand remained weak last month due to monsoon-related disruptions, logistical challenges, and the festive season, which kept buyers cautious. Major mills either reduced prices or offered discounts amid weak market sentiment.

In the projects segment, prices declined by 1,300/t m-o-m to average price of INR 46,000-46,500/t FOR Mumbai.

Outlook

Domestic steel prices will most likely remain rangebound in the near term, with a potential rebound likely ahead of Diwali.

Leave a Reply