- LME zinc climbs to a six-month high

- SHFE zinc drops to 18-month low

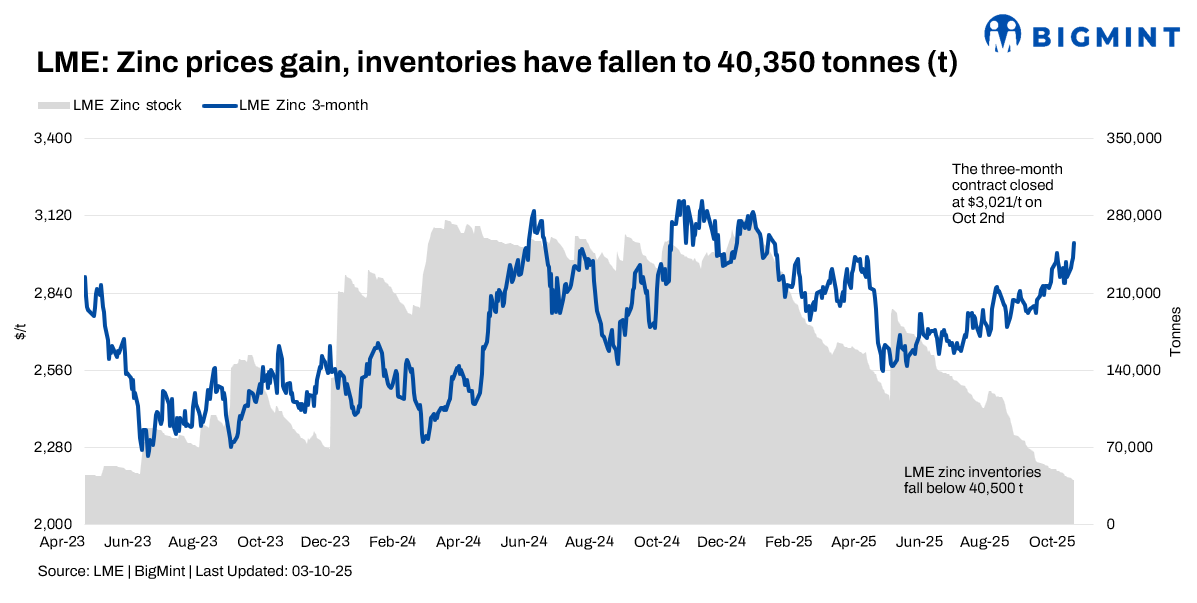

Western zinc markets are facing a deepening supply squeeze as LME inventories have fallen to 40,350 tonnes (t), with only 30,625 t deliverable—barely enough to supply global demand for a single day. Off-warrant stocks, totalling 12,087 t, further underline how depleted exchange-registered inventories have become.

In contrast, China’s SHFE zinc inventories have surged to 100,544 t, the highest since August 2024, reflecting stronger domestic output and a widening geographic imbalance in zinc availability.

Price movements mirror this divergence. LME zinc recently climbed to a six-month high, while SHFE zinc dropped to an 18-month low, expanding the London–Shanghai price differential to over USD 330/t. This spread indicates localized tightness in Western markets and potential arbitrage opportunities in the months ahead.

Globally, refined zinc output fell by 2.1% in the first half of 2025, despite a 6.3% rise in mined production. The shortfall was driven by smelter cutbacks in Brazil, Japan, and Kazakhstan, where energy costs, plant closures, and environmental constraints reduced refining capacity. In contrast, China’s refined zinc output rose nearly 7% year-on-year, supported by a 43% surge in concentrate imports and higher treatment charges (TCs) that boosted smelter margins and utilization rates.

The result is a market divided between short supply in the West and surplus metal in China. Analysts suggest that unless price spreads narrow or export flows increase, global supply pressure may persist through late 2025. The current arbitrage window could encourage Chinese exports, potentially easing LME tightness and restoring balance—if such flows materialize before the deficit deepens further.

This evolving dynamic between depleted Western warehouses and rising Chinese surpluses is expected to shape zinc market behavior through the remainder of 2025, with the focus firmly on whether a “Chinese booster” will replenish LME stocks and stabilize global supply.

Leave a Reply