- Finished steel prices dip 2-3% on weak demand, rising stocks

- Coking coal tags rise 5% on improved trading, supply concerns

- Market shows optimism regarding demand recovery in Oct’25

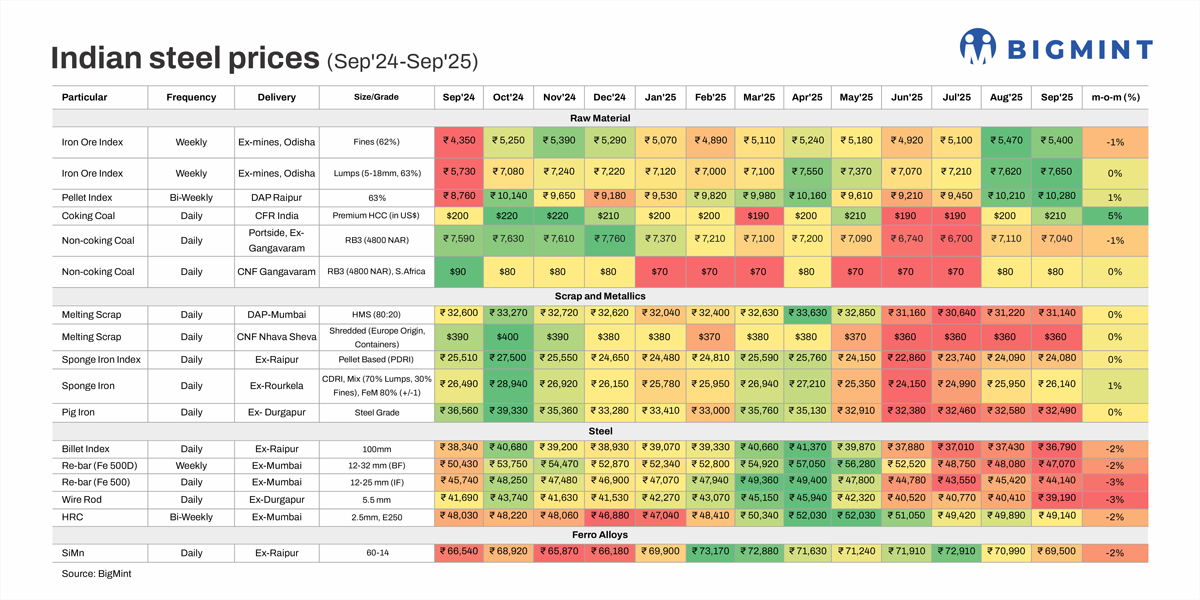

Morning Brief: India’s steel and raw material prices remained largely stagnant in September, with the demand slump due to the monsoon continuing. Some marginal declines were recorded, especially in the semi-finished and finished steel prices. Only coking coal was an exception, experiencing a decent 5% hike, amid supply concerns.

Overall, demand failed to rebound, as many had hoped, and the approach of the festive season was marked by subdued trading activity, with restocking impetus absent amid elevated finished steel inventories.

Additionally, the positive impact of the government’s GST reforms is expected to be felt in the medium term rather than immediately, so September faced limited fresh demand triggers.

Price movements in Sep’25

Iron ore

Iron ore: BigMint’s Odisha iron ore fines (Fe 62%) index dipped by 1% m-o-m to a monthly average of INR 5,400/tonne (t) ex-mines. The lumps (5-18 mm, Fe 63%) index remained stable at INR 7,650/t ex-mines.

Iron ore prices in Odisha remained firm m-o-m, supported by limited material availability due to monsoon-related production disruptions. However, prices remained flat, with steelmakers largely engaging in need-based buying and cautious market sentiment prevailing due to muted sponge iron and steel segments.

Meanwhile, lower-grade fines fetched active buying interest, driven by improved activity in the seaborne market due to rumours of a possible export duty.

The monthly iron ore auctions from the Odisha Mining Corporation witnessed bids falling by INR 350/t m-o-m for fines and INR 100/t for lumps. This also depressed sentiment.

Pellets: PELLEX, BigMint’s domestic pellet index, inched up by 1% m-o-m to INR 10,280/t DAP Raipur.

A soft steel market weighted on pellet prices in September, leading to cautious procurement. However, prices remained stable overall, as some pellet plants were under maintenance and suppliers intermittently kept sales closed, which kept supply tight. Stable iron ore prices also supported pellet tags, and sellers maintained firm offers.

Coal

Coking coal: Imported coking coal increased by 5% m-o-m to a monthly average of $210/t CFR India in September, driven by an improvement in trade activity in the middle of the month. Other factors that lent support were the stability in Australian coking coal prices, elevated domestic tags in China, supply concerns in Queensland, including BMA’s planned Saraji mine shutdown, and firm met coke prices in India.

Non-coking coal: South African portside RB3 thermal coal (4800 NAR) prices inched down by 1% m-o-m to INR 7,040/t, while CNF Gangavaram tags were stable at $80/t.

Prices witnessed limited movement due to a couple of reasons: First, the monsoon curbed demand, with poor steel demand from the construction sector pressuring the sponge iron market.

Secondly, the GST revisions led traders to aggressively cut prices to liquidate old stocks. Notably, the reforms included an increase in the rate on coal to 18% from 5% and the removal of INR 400/t cess. While the overall tax burden remained unchanged, the restructuring meant increased upfront working capital requirement due to the higher GST outflow.

However, the price cuts failed to spark buying enthusiasm, and trading activity remained muted due to uncertainty over the reforms’ impact.

Thirdly, high freights continued to keep offers firm.

Scrap & metallics

Domestic melting scrap: Domestic HMS 80:20 was stable m-o-m, averaging at INR 31,140/t in September, with steel demand patchy amid a prolonged monsoon. Sufficient supply amid moderate demand prevented price rises.

Imported melting scrap: Imported EU-origin containerised shredded prices were stable m-o-m at $360/t CNF Nhava Sheva, with tepid trading observed throughout the month. A strong dollar, weak finished steel sentiment, the availability of cheaper domestic substitutes, and monsoon rains limited buying appetite.

Sponge iron: Pellet-based sponge iron (PDRI) was flat m-o-m at INR 24,080/t ex-Raipur, while the CDRI variant was up by a minor 1% at INR 26,140/t. Prices held steady amid stable raw material costs and selective restocking activity. Sellers also limited price cuts to sustain margins, while some regions experienced tight supply.

Pig iron: Steel-grade pig iron prices were also steady m-o-m at INR 32,490/t. Limited availability in some pockets and stable raw material costs supported prices, while purchases took place on a need basis amid cautious sentiment and bearish downstream markets.

Ferro alloys

Silico manganese: Domestic silico manganese (60-14) dropped by 2% m-o-m to INR 69,500/t due to sluggish demand from steelmakers, which tried to maintain lean stock levels. Inventories accumulated in major producing hubs, and sellers were forced to trim offers to generate liquidity. The monsoon also hampered smooth material movement, delaying deliveries and discouraging fresh procurement.

Sellers attempted to lift prices marginally but faced substantial pushback. By the month-end, tightening supply due to monsoon-driven transportation challenges allowed some sellers to quote higher offers, which limited the price correction m-o-m.

Steel

Billets: BigMint’s billet index declined by 2% m-o-m to INR 36,790/t ex-Raipur, as lacklustre finished steel demand spurred price corrections. While GST 2.0 reforms and improved trade activity boosted prices in some regions in the first half of the month, demand softened towards the end of September, with sharper decreases in the final week.

BF rebar: Blast furnace (BF) rebar prices decreased 2% m-o-m to INR 47,070/t ex-Mumbai, as sluggish trade persisted due to heavy rains, the construction activity slowdown, and logistics disruptions.

At the beginning of the month, while some mills increased list prices by INR 1,000/t against levels in end-August, others rolled them over. However, these price hikes were not absorbed by the market.

Additionally, inventories at Tier-1 mills remained high, increasing by around 8% in mid-September compared with the beginning of the month.

The projects segment also saw muted activity, as buyers postponed purchases amid the monsoon and logistics challenges.

IF rebar: Induction furnace (IF) rebar prices were down by a slightly sharper 3% at INR 44,140/t ex-Mumbai due to limited inquiries and substantial inventories, with holding periods of around 12-15 days. This pushed manufacturers to reduce offers to liquidate inventories, but price drops were contained by a few factors.

First, the GST 2.0 framework, which reduced rates of key commodities in end-user segments such as construction and manufacturing, incentivised procurement. Second, sponge iron shortages in some markets offered cost support.

Similar factors caused wire rod prices to fall by the same percentage to INR 39,190/t ex-Durgapur.

HRCs: Trade-level hot-rolled coils (HRCs) were down by 2% m-o-m to a monthly average of INR 49,140/t. Dull trade activity weighed on sentiment, while uncertainty regarding future pricing and market direction prevented significant price movements.

Initially, leading steelmakers raised HRC and cold-rolled coil (CRC) list prices by INR 750-1,000/t against the net sales prices of end-August, but these failed to set off momentum in the trade channel.

Need-based buying continued, and ample supply meant a lack of restocking urgency. As the GST reforms took effect, traders turned guarded, unclear about how pricing would move, though there had been expectations of a demand boost earlier. Towards the month-end, festive holidays, such as Durga Puja, also reined in trade activity.

Outlook

Currently, market participants seem hopeful of a demand uptick in October, likely around Diwali. BF rebar prices increased by INR 400/t w-o-w in the latest exy-Mumbai assessment on 3 October, and it is heard that leading mills may increase their list prices in early October. However, in the flats segment, sentiment seems more cautious, with expectations of a roll-over by major mills, as demand did not improve in September.

Leave a Reply