- No new fixtures reported on Australia-India coal route

- Indonesia-India rates inch higher despite no reported fixtures

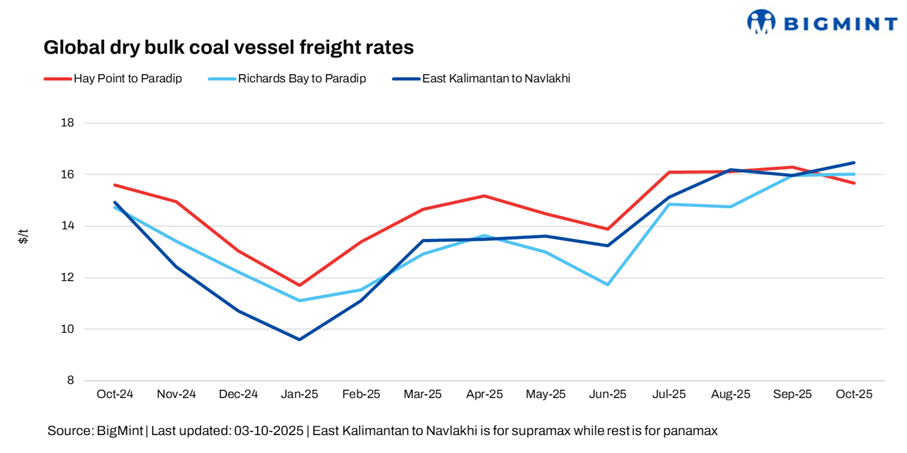

Dry bulk coal freights maintained a mixed trend this week. Indonesia-India rates rebounded, whereas Panamax freights on the South Africa-India and Australia-India routes declined. Trading was largely inactive, with no fixtures reported across any of the routes amid ongoing holidays in India.

A source noted, “Asia-Pacific Panamax freight rates eased as sentiment softened amid sluggish Pacific basin trading. Freight derivatives declined during Asian hours, reinforcing the negative mood, while bunker prices edged slightly higher. No new fixtures were reported on the Australia-India coal route.”

Another source told BigMint, “Trading activity from South Africa remained thin during Asian hours, with limited fixtures and minimal market movement, reflecting subdued demand and cautious sentiment among charterers in the Atlantic-Asia routes.”

“Indonesia-India dry bulk coal freight rates inched higher despite no reported fixtures, largely on the back of tighter vessel availability, with owners holding a bullish stance and pushing for higher levels, even in the absence of fresh spot demand”, a charterer shared observations, shedding light on the dynamics of the route.

India’s port-side thermal coal stocks edged down slightly to 11.86 million tonnes (mnt) in week 39 from 11.93 mnt in week 38, according to provisional BigMint data. Market sentiment remained cautious, influenced by volatile ocean freights and recent GST reforms, with participants adopting a wait-and-watch approach before committing to fresh restocking.

Route-wise updates

- Australia (Hay Point)-India (Paradip), Panamax: Freights from Australia to India edged down by around 0.84/dry metric tonne (dmt) to $15.66/dmt.

- South Africa (Richards Bay)-India (Paradip), Panamax: Panamax freights on the South Africa to India route fell sharply by $1.98/dmt w-o-w to $16.02/dmt.

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: Supramax coal freights on the Indonesia to India route stood at $16.47/dmt, a significant w-o-w increase of $2/dmt.

Market highlights

- Baltic index drops to 1-month low: The Baltic Exchange’s main dry bulk index dropped sharply to around one-month low by 331 points w-o-w to 1,909 on 02 October 2025 due to falling rates across all vessel segments. The Panamax segment slipped by 139 points w-o-w to 1,685, while the Supramax segment edged down 27 points w-o-w to around 1,456, reflecting uncertainty among market participants.

- Brent crude oil futures fall w-o-w: Brent crude oil futures fell significantly by around $3.57/barrel (bbl) w-o-w to $64.04/bbl due to a combination of factors such as easing global demand concerns, rising supply expectations, which collectively weighed on market sentiment and pressured prices downward.

Outlook

The near-term outlook for dry bulk coal freights appears mixed across key routes. Indonesia-India rates are likely to remain supported by tight vessel availability and steady demand, while Australia-India and South Africa-India routes may face softer momentum due to muted cargo flow and cautious charterer activity.

Overall market sentiment is expected to stay cautious, influenced by limited fixtures, seasonal demand fluctuations, and volatility in bunker prices. Charterers may continue a selective approach, keeping freight levels under pressure on routes with ample tonnage, while tighter lanes could see occasional spikes.

Leave a Reply