- Weak demand, supply overhang weigh on market

- Monsoon disruptions, festive holidays curb trades

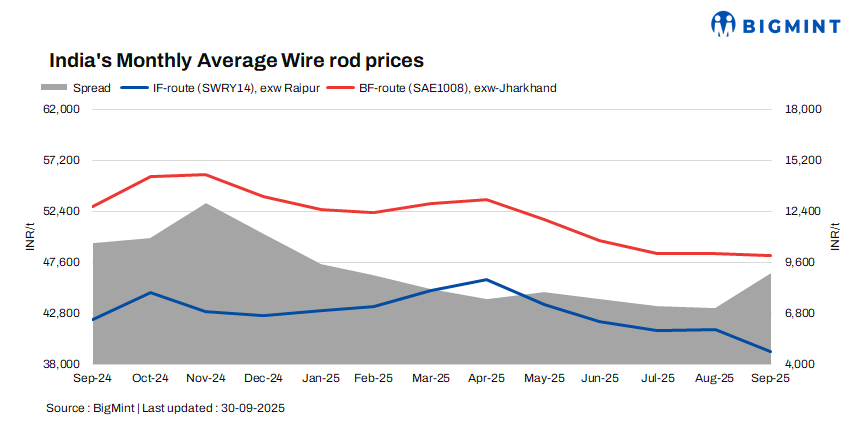

Indian steel wire rod prices plunged in September 2025. In the induction furnace (IF)-route segment, wire rod prices witnessed a monthly average decrease of INR 1,200/t ($14/t) to INR 39,200/t ($442/t) exw-Durgapur and fell by INR 900/t ($10/t) to INR 40,300/t ($454/t) exw-Raipur as compared to August levels. The spot trade reference price stood at INR 39,500/t ($445/t) exw-Raipur and INR 39,000/t ($439/t) exw-Durgapur as on 3 October.

Cumulative wire rod production via the IF and BF routes in January-August was assessed at 5.4 million tonnes (mnt), an increase of 10% compared to 4.9 mnt during the same period in 2024. Notably, for IF-route wire rods, Raipur (central India) and Durgapur (eastern India) are the major supply centres catering to various markets across the country. The daily wire rod production capacity in these two markets is around 20,000 t, as per BigMint data.

Wire rod prices (5.5-6mm, SAE1008) were assessed at INR 48,000/t ($541/t) exw-Jharkhand as on 26 September.

Market scenario

Raw material price trends: Steel billets and sponge iron are the key raw materials used in IF-route production. The semi‑finished steel market remained subdued, with prices under pressure due to weak downstream demand from the secondary mills. Festive season closures in some regions further slowed trade, and overall market activity remained limited to need-based buying. Considering the Raipur market as a benchmark, billet prices decreased by INR 600/t ($7/t) to INR 36,800/t ($415/t) exw, while sponge iron (PDRI FeM 80% +/- 1) saw no major changes, assessed at NR 24,100/t ($272/t) exw (monthly average prices).

Buying remains dull: Buying enquires were sluggish. End-users of wire rods, like binding and GI wire manufacturers, cautious about bulk procurement due to uncertainty in market direction, festivities and heavy rains in several regions. Manufacturers reported huge inventories at mills and slow lifting of previously booked material which drag offers down. Sellers offered discounts depending upon prior bookings and payment terms to liquidate material. This factor also balanced the bid-offer disparity in the spot market.

Primary mills see weak demand: In the BF-segment, wire rod prices (5.5-6mm, SAE1008) edged lower m-o-m by INR 200/t ($2/t) to average of INR 48,200/t ($543/t) exw-Jharkhand in September. Wire rod demand remained subdued in September, weighed down by monsoon disruptions, festive season slowdown, and restrained offtake from downstream sectors. Construction activity was impacted by rains, while infrastructure projects saw slower execution. Automotive and engineering industries also displayed cautious buying behaviour amid inventory adjustments.

Outlook:

The outlook for October is cautiously optimistic. A post-monsoon recovery in construction and infrastructure may support domestic demand.

Leave a Reply