- Mills may cut production further, impacting scrap demand

- Ongoing GST inspections continue to foster uncertainty

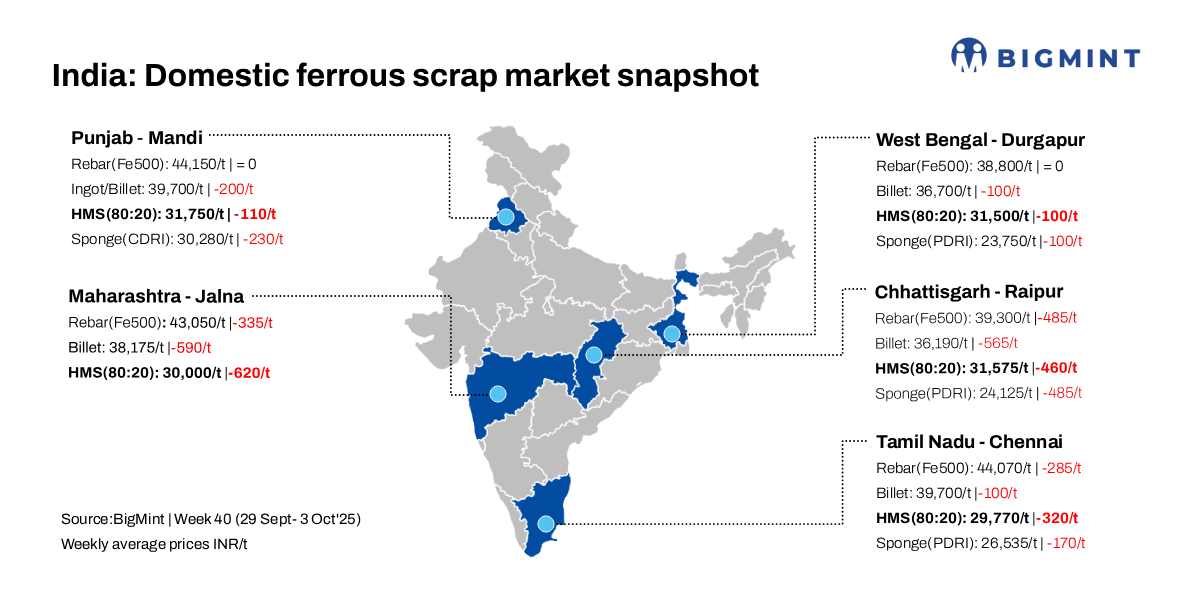

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, remained stable d-o-d at INR 34,500/t DAP on 3 October 2025. However, on a w-o-w basis, scrap prices declined by INR 100/t, pressured by weak demand.

Mandi Gobindgarh, one of India’s key steel manufacturing hubs, has been witnessing growing caution among steelmakers, as sluggish demand for finished steel weighs on overall market sentiment. With inventories currently at comfortable levels, several medium-sized mills — which are already operating on reduced shifts, limited to just 12 hours a day — are now contemplating further production cuts.

The high conversion cost associated with steelmaking, coupled with weak demand and falling prices, has prompted mills to scale back their procurement activities. As a result, scrap buying was largely need-based this week, with steelmakers avoiding large-volume purchases. In response, local scrap suppliers reduced their offers, reflecting the bearish sentiment across the region.

Despite steady availability and no immediate shortage of domestic scrap in Mandi, the ongoing GST inspections continue to cast a shadow of uncertainty over both scrap buyers and suppliers, impacting transactional confidence in the market.

Imported scrap market

The inflow of imported scrap remained minimal this week, as local mills shifted focus to domestic sources. Imported bookings nearly stalled, with a notable $10-15/t bid-offer gap making negotiations difficult. This pricing disparity further reinforced the preference for domestic scrap, which currently offers better viability amid the market’s cautious undertone. HMS 1 scrap from origins such as Bahrain, Kuwait, and South Africa delivered to the West Coast of India was in the range of $340-$342/t CFR. Additionally, South American HMS (hand-loaded) was available at $325/t in Mandi.

As Mandi Gobindgarh navigates this phase of muted activity, all eyes are now on how demand trends evolve in the coming weeks, especially with the festive season approaching — a period that could offer some support to the struggling market.

Raw material

Sponge iron (CDRI) prices in Mandi remained unchanged d-o-d at INR 30,300/t ex-works. On a weekly basis, sponge iron prices dropped by INR 230/t.

Steel grade pig iron prices in Ludhiana declined by INR 200/t to INR 35,000/t ex-works.

Steel market trends

Semi-finished steel (ingot) prices in Mandi Gobindgarh remained stable d-o-d at INR 39,700/t DAP, pressured by sluggish demand and tightening conversion margins. Across key production hubs, ingot prices softened further, by INR 100-300/t d-o-d. Ingot prices declined by INR 200/t on a weekly basis in the region.

Rebar (Fe500) prices in Mandi also remained steady d-o-d at INR 44,100/t ex-works. Finished steel prices remained steady on a w-o-w basis.

Overview of Alang scrap market

On 3 October 2025, melting scrap prices in Alang’s ship-breaking sector remained steady, with HMS (80:20) assessed at INR 30,500/t, as per BigMint data. Trade volumes in both semi-finished and finished steel products were average. Stable demand from Bhavnagar’s IF units played a key role in preventing price fluctuations.

Upcoming scrap auctions

Price highlights

End-cutting to billet spread: In Mandi, the spread between end-cutting scrap and billets stood in the range of INR 4,900-5,200/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were assessed at $325-330/t, approximately INR 31,300/t (inclusive of freight). HMS (80:20) prices in Mumbai remained stable at INR 30,700/t DAP today. Indicative prices of shredded from Europe stood at $355-358/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 12,050/t.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply