- Inquiries remain limited amid cautious market sentiment

- Weak steel demand weighs on sponge prices

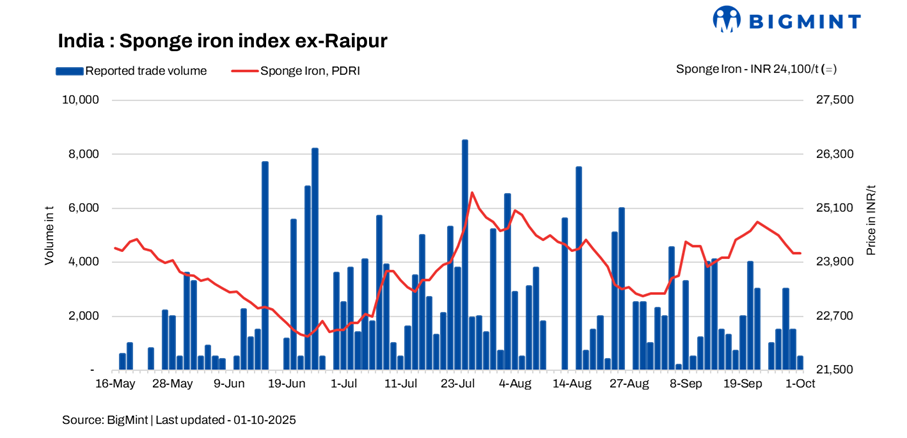

The Indian sponge iron market began October on a subdued note, with prices declining by INR 50-150/t across major markets. Sellers resisted further price cuts due to high input costs and festive season closures limiting availability.

Trade activity was muted, with limited buyer inquiries and cautious sentiment prevailing. Around 5,000 tonnes of deals were concluded across India, reflecting subdued demand. Overall, the market remained quiet with participants adopting a wait-and-watch approach.

Monthly recap- Sep’25

The Indian sponge iron market witnessed a positive price trend across regions in September, with increases ranging from INR 200-1,000/t. Despite limited buying activity, prices remained firm, driven primarily by rising raw material costs-particularly pellets and coal. Sellers refrained from price cuts to sustain margins, amid a mix of macroeconomic and regional factors.

Price movements

Central India: Prices increased by INR 800-900/t.

Eastern India: Prices rose by INR 300-700/t.

Southern India: Prices were up by INR 200-500/t

Key market drivers

- Subdued demand with selective restocking:

End-user demand remained soft, though some restocking was seen at lower price levels, offering mild support to the market. - Rising raw material costs:

Elevated pellet and coal prices exerted cost pressure on manufacturers, leading to firm offers despite weak downstream demand. - Inventory-driven selective selling:

High inventories prompted selective price adjustments in some regions, but not enough to reverse the broader upward trend. - Monsoon-related disruptions:

Unseasonal rains impacted logistics and industrial operations, limiting demand recovery and trading activity.

Outlook:

The sponge iron market is expected to remain range-bound with a slight upward bias, supported by firm raw material costs, limited supply adjustments, and cautious buying amid festive and post-monsoon recovery.

Rationale

Prices have been derived based on transactions, offers, bids, and indicative price data sets. Transactions are considered as T1 and given a weightage of 50%, whereas other data sets are considered as T2 and given a weightage of the balance 50%.

Click here for detailed methodology

Leave a Reply