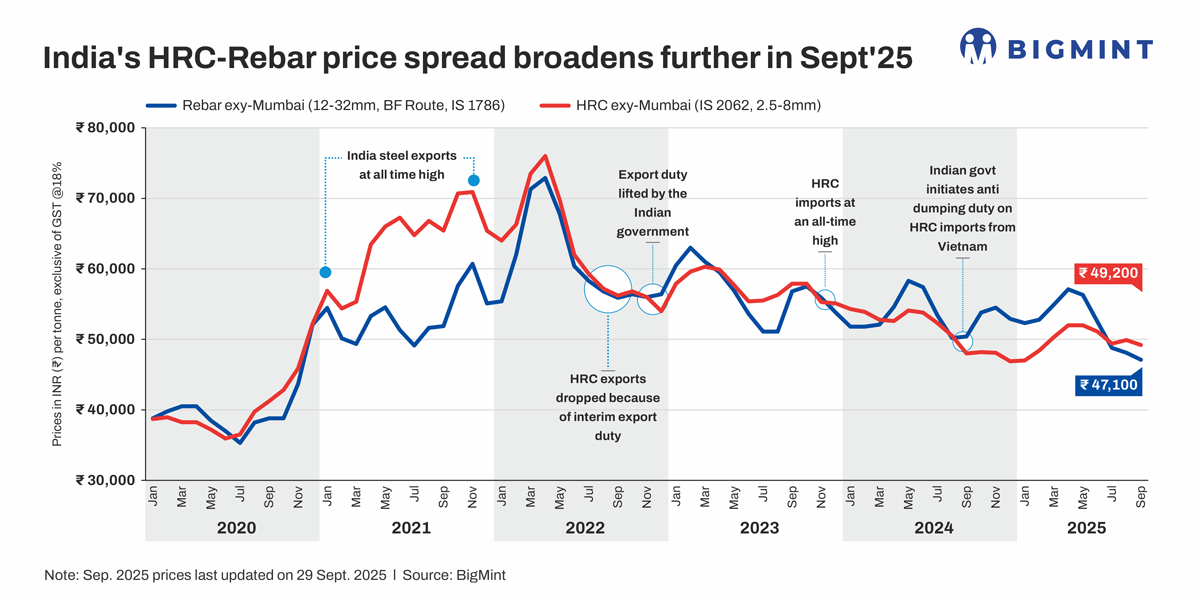

- Spread grows by just INR 300/t in Sep versus INR 1,800/t in Aug

- Weighted average BF-rebar prices drop INR 1,000/t m-o-m

- Steel prices to remain under pressure but slight uptick expected

Morning Brief: Indian steel prices were on a downward trajectory for much of September 2025 due to seasonal and festive slowdown affecting trade sentiment. The initial enthusiasm in the market in the beginning of September, with mills hiking prices across product categories, wore out after the first two weeks.

The spread, or gap, between domestic HRC (IS 2062, 2.5-8mm) and blast furnace-origin rebar (12-32mm, IS 1786) prices remained in positive zone for the third consecutive month in September. However, in contrast with the INR 1,800/t expansion in August, the spread grew by just INR 300/t in September. While weighted average HRC prices declined by INR 700/t m-o-m in September, rebar prices dropped a sharper INR 1,000/t.

Notably, after remaining in reverse territory for 10 consecutive months since September 2024, the HRC-rebar spread had finally turned positive in July this year. Under normal market conditions, HRC commands a premium of around INR 4,000-5,000/t over BF rebar. However, persistent weakness in global steel prices from end-2024 onwards eroded domestic flat steel prices and pushed the spread into reverse zone.

Factors affecting steel prices

HRC market movements: Leading Indian steel manufacturers officially raised prices of HRC and CRC by INR 750-1,000/t for September sales as compared to net sales prices in end-August. The surge in manufacturing activity in August, as evinced by the manufacturing PMI hitting a record high, supported this trend.

However, HRC market sentiment stayed muted as sluggish demand, oversupply and ample inventories pressured prices. Market participants informed that high stocks and thin margins kept trading slow while the expected pre-festive pickup in demand did not materialise. A demand uptick ahead of the festive season and positive impact of GST reforms in the steel-consuming downstream sectors was expected. But persistent rainfall and flood-like conditions in several regions have disrupted construction activity.

The HRC market remained weak, with buyers limiting purchases to immediate needs towards the end of the month. GST cuts and festive holidays added uncertainty. Adding to the uncertainty, GST reforms introduced on 22 September have left the market in a state of flux as traders are watching closely to gauge how tax changes might affect pricing and demand. Additionally, the festive season of Durga Puja has slowed down trade, particularly in eastern India.

Bulk HRC imports dropped 37% m-o-m in August and imports trended lower in September too. Staggered safeguard duty, AD duty on Vietnamese imports, proposals for safeguard investigation into imports from China, tightening of quality control parameters all contributed in some measure to curbing steel imports. The landed cost of HRC imports from China and Japan stayed above domestic prices.

BF-rebar market in September: Some of the leading primary mills increased prices by INR 1,000/t for early-September deliveries as against end-August. Rebar inventories with Tier-1 mills remained largely unchanged m-o-m in early September.

However, construction and infrastructure activities have slowed down due to heavy monsoons, labour shortages, and logistics disruptions. Demand remained limited as overall market sentiment stayed weak. Inventories at mills rose slightly by around 8% in mid-September compared with levels seen at the beginning of the month.

Towards month-end, the primary mills either increased their discounts or reduced list prices due to subdued market sentiments. Demand was impacted due to heavy downpour in different regions and the descent of a festive season lull on key markets across regions.

The projects segment witnessed low activity as buyers were on the sidelines amid monsoons and logistics challenges. Rebar inventories at mills remained at high levels. A major PSU steel mill is expected to take a shutdown next month, market sources informed.

Outlook

With the safeguard duty in place, trade remedial measures have offered support to domestic producers amid market slowdown. Landed cost of imports from key countries are higher than domestic prices.

Domestic steel prices will most likely remain rangebound in the near term, with a slight rebound likely ahead of Diwali. Flat steel export offers may stay under pressure in the short term, driven by cautious market sentiment and the approaching CBAM. This will be a drag on domestic prices too. Liquidity constraints and uncertain market conditions may limit demand.

Longs prices, on the other hand, have been weighed down by need-based buying amid monsoon disruption. But market participants are hopeful of a turnaround in October.

Leave a Reply