- Export offers to Middle East fall by $5/t w-o-w

- Offers to EU hold firm despite sluggish demand

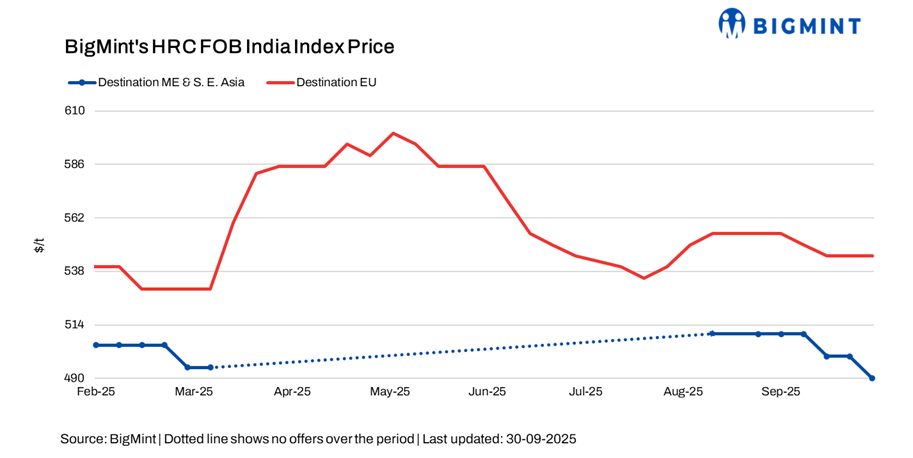

BigMint’s India hot-rolled coil (HRC, SAE 1006) export index for the Middle East and Vietnam fell by $10/tonne (t) w-o-w to $490/t as of $500/t last week. A deal was heard concluded for October sales to the Middle East, indicating improved demand in the region from the infrastructure sector. While some sectors may be experiencing a slowdown, significant government-backed construction initiatives are still driving demand for steel products in key areas of the region.

India’s HRC (S275) export index for Europe held steady w-o-w at $545/t FOB main port amid sluggish domestic demand, with the market quiet due to weak end-user demand and regulatory uncertainty.

1. Indian HRC export offers to Middle East drop w-o-w: Indian HRC export offers to the Middle East dropped by $5/t w-o-w to $520/t CFR UAE as compared to $525/t CFR UAE a week ago. A deal for around 25,000 t was heard concluded at $518/t for October sales.

China’s HRC export offers to the Middle East remained unchanged at $505-510/t CFR UAE. Moreover, a tube maker closed a deal for around 30,000 t at $500-510/t CFR UAE for early-November sales, though this information could not be confirmed.

HRC futures on the Shanghai Futures Exchange (SHFE) January 2026 contracts fell by RMB 75/t (10/t) w-o-w to RMB 3,274/t ($460/t) as compared to RMB 3,349/t ($470/t) a week ago. Moreover, on a d-o-d basis, contracts decreased by RMB 30/t ($4/t) against RMB 3,304/t (464/t).

2. Indian HRC export offers to EU remain stable w-o-w: Indian HRC export offers to the EU remained flat w-o-w at $595-600/t CFR Antwerp ($545-550/t FOB India), with muted trading activity due to adequate stock levels and uncertainty over new trade policies and the Carbon Border Adjustment Mechanism (CBAM). Buyers adopted a wait-and-watch approach, delaying purchases until CBAM regulations and steel safeguard measures became clearer.

3. Indian HRC offers to Vietnam decline w-o-w: Indian HRC export offers to Vietnam declined by $5/t w-o-w to $505-510/t CFR Ho Chi Minh City (HCMC) against $510/t CFR last week. Notably, a deal for approximately 30,000 t at $507/t HCMC for October sales was heard concluded.

Vietnam’s steel demand growth was supported by a recovering domestic market, driven by the real estate sector’s upturn and increased public investment in infrastructure projects, resulting in strong consumption of construction steel and HRC.

Outlook

Indian steel exports are expected to experience regional divergence in the short term, with the Middle East and Vietnam offering growth opportunities due to strong demand, while EU exports could remain sluggish amid regulatory ambiguity.

Leave a Reply