- Revised GST, weak demand delay cotton price recovery

- Exports impacted by price unviability in global markets

The rationalisation of GST on man-made fibres (MMF) is set to alter India’s fibre mix, but the spillover on cotton will not be immediate. Cotton demand is expected to soften gradually as spinners gain flexibility to blend cheaper MMF, but the sector enters this transition with an unprecedented supply overhang.

The Cotton Association of India (CAI) estimates closing stocks at 60-65 lakh bales by 30 September 2025 – the highest since the Covid year, when spinning mills were shut for six months. This time, however, the surplus stems from two different forces: a surge in imports and weakening domestic consumption.

Imports, on the other hand, are expected to touch 41 lakh bales by end-September, breaking a 100-year record. At the same time, consumption has trailed due to tariffs, labour challenges and lower mill offtake.

MSP cushion for farmers, but CCI faces storage, liquidity strain

While farmers remain protected at present with an MSP of INR 8,100/candy (around 356 kg), pressure is likely to mount when procurement begins. The Cotton Corporation of India (CCI) bought one crore bales last year – nearly a third of the crop. With production this year projected at 325-340 lakh bales, questions loom over CCI’s capacity to absorb a similar volume.

The problem is structural as much as financial. CCI godowns already hold 35-40 lakh bales, of which 13-15 lakh remain unsold with the rest sold but physically yet to be lifted. Space constraints and funding requirements could limit MSP operations, triggering farmer anxiety in key cotton belts.

Early sowing, new seeds lift crop prospects

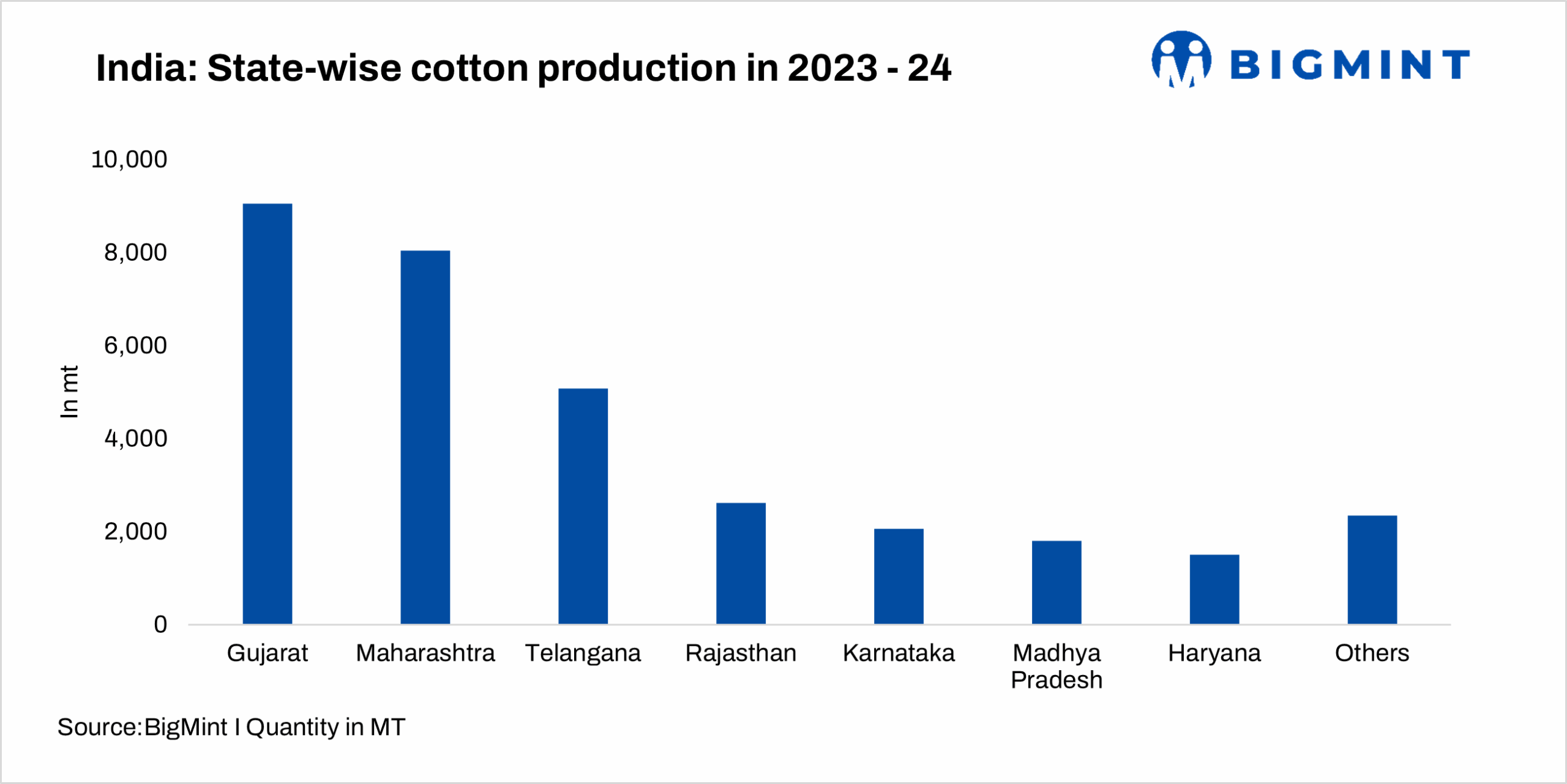

Rains in the first half of June helped advance sowing and bring early arrivals — currently at around 30,000 bales per day. Fresh hybrid seeds marketed as 4G and 5G in Gujarat by 15-20 companies have pushed yields up to 700 kg per hectare in select pockets.

If adoption of such seeds extends to 50% of growers across Gujarat, Maharashtra and southern states, output could hold at 325-340 lakh bales or higher. Arrivals may climb to 50,000 bales per day by early October. Yet, a clearer crop estimate will only emerge around mid-October or November.

Imports surge despite surplus: mills tap cheaper global cotton

India’s cotton paradox is stark. Despite ample domestic supply and rising carryover stocks, mills are importing at record levels. Last year, India imported just 15 lakh bales. This year, the figure has jumped to 41 lakh. Two issues are driving this shift.

First, cotton procured by CCI from October to April-May remains locked in godowns until price lists are released in March-April. Large mills consuming 5,000–8,000 bales a day cannot afford to wait — forcing them to tap cheaper foreign cotton.

Secondly, MSP-linked pricing has made Indian cotton 10-15% costlier than global rates for much of the past year. Intercontinental Exchange (ICE) futures at around INR 46,000/candy but CCI is quoting INR 55,000/candy. Thus, mills find imports more viable despite the foreign exchange drain. If policies remain unchanged, stocks could hit 100 lakh bales by September 2025, creating a China-style surplus build-up.

Exports collapse as price gap widens

India has swung from a cotton exporter to an importer within a year. Once capable of shipping one crore bales annually, exports shrank to 30 lakh bales last year and are likely to reach only 18 lakh bales this year. The price gap is the spoiler.

With Indian cotton at a 10-15% premium over world prices and yarn exports tied to ICE-linked benchmarks, mills face shrinking margins and reduced competitiveness. Global buyers in Bangladesh, China and Vietnam are increasingly sourcing from Brazil, where production has surged to 240 lakh bales with only 30 lakh consumed domestically. Brazilian cotton now sells at around INR 51,000/candy equivalent versus India’s INR 55,000/candy.

China, meanwhile, is heading for a 12-year high crop of 7.5 million tonnes — equivalent to 460 lakh Indian bales — up by 100 lakh bales over last year. With both Brazil and China adding to the global surplus, India faces limited headroom to export either cotton or yarn.

Structural weakness: yields lag global benchmarks

India holds one-third of the world’s cotton acreage but produces far below potential. Yields hover at 420-450 kg per hectare, among the lowest globally. The global average is 750 kg, while Brazil and Australia exceed 2,000 kg. The lower production can be attributed to some factors. One, about 70% of India’s acreage is rain-fed, and secondly, seed technology has stagnated since the introduction of Bt cotton in 2003-04. For the past five years, production has fluctuated between 300 and 340 lakh bales without a structural uplift. Mr Atul Ganatra, President of the Cotton Association of India, while speaking at a BigMint webinar on “India’s textile industry: GST impact and harvest season outlook,” indicated that with better seeds, cotton output could jump from 330 lakh to 500 lakh bales rapidly.

Policy reset essential for growth, exports

Ms. Chandrima Chatterjee, Secretary General, Confederation of Indian Textile Industry (CITI), also speaking at the webinar, points to the contradiction in current policies. While farmers deserve support, volatility driven by MSP and supply distortions have eroded price stability across the value chain. The industry aims to double output and market size by 2030, but that hinges on fibre availability, competitive pricing and predictable policy.

For now, cotton enters the new season high on existing stocks, slipping demand, import distortions and export losses – a cocktail that demands urgent recalibration before the GST-led fibre shift reshapes the industry even further.

Leave a Reply