- Pre-holiday restocking weaker than expected but prices trend up

- Post-holiday demand to support prices amid balanced fundamentals

Mysteel Global: China’s thermal coal market has exhibited distinct seasonal patterns ahead of this year’s National Day holiday week, which begins next Wednesday. This year, as the pre-holiday restocking fizzled out earlier than expected, insiders are questioning whether prices can regain strength once the week-long break ends.

Typically, coal prices increase after the holiday, as utilities always rush to restock when the market reopens. However, in recent years, stronger regulation and shifts in demand have reshaped the market, making it harder to take pre-holiday trends as reliable indicators of what will follow.

In 2021, the market experienced unprecedented turbulence around the National Day week, as Mysteel Global reported at the time. Before the break, soaring demand from power generators, coupled with tight domestic supply under strict carbon emission restrictions and mine safety inspections, pushed prices to record highs. Average benchmark 5,500 kcal/kg thermal coal prices at northern ports surged beyond RMB 1,400/tonne (t) ($196.3/t), FOB with VAT, before the holiday, Mysteel historical data show.

The government responded with a series of emergency measures — including accelerating coal output, enforcing long-term contract fulfilment, and capping spot prices — but the desired outcome of prices retreating did not occur as fast as Beijing had intended. Prices continued to soar in the first two weeks after the holiday and reached a record high of RMB 2,550/t on 18 October, before quickly plummeting to bottom out at just RMB 780/t on 31 December.

Following the 2021 price turmoil, the central government mandated higher coverage of long-term contracts at regulated prices (typically capped around RMB 700-770/t for 5,500 kcal NAR coal) to ensure stable supply to power utilities and to keep spot prices in check.

Around the National Day holidays in both 2022 and 2023, pre-holiday restocking by power plants provided mild support for prices, but ample domestic production and strict oversight prevented significant spikes. Post-holiday, prices typically softened as electricity demand entered a seasonal lull, yet volatility remained muted compared to 2021, reflecting improved market resilience under policy guidance.

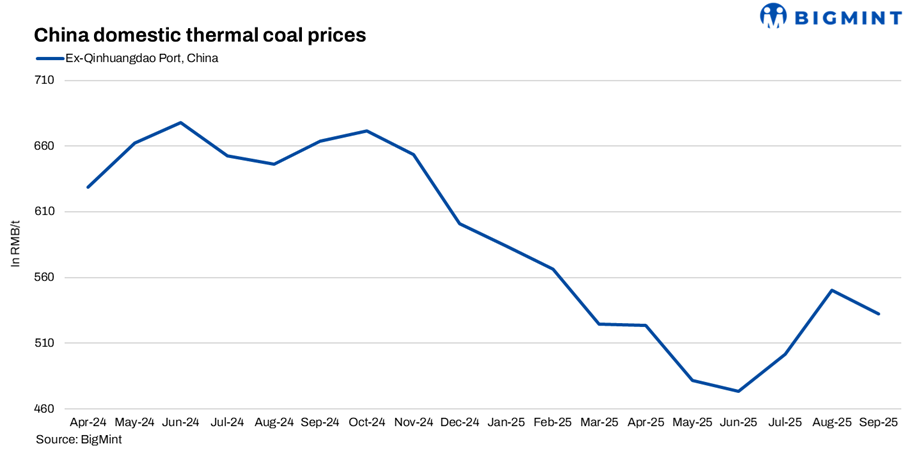

In September 2024, port prices lifted in anticipation of the traditional ‘golden’ season during September-October for non-power end-users (such as cement makers preparing for a spurt in autumn construction activity) and by routine utility restocking. The 5,500 kcal/kg NAR thermal coal price at northern ports rose from RMB 840/t to RMB 870/t throughout the month.

Despite the pre-holiday uptick, market sentiment turned cautious in the weeks following. Power plants in southern China showed limited appetite for high-priced domestic coal, preferring cheaper alternatives or delaying purchases. Non-power sectors, such as cement and chemicals, offered only marginal demand support. Consequently, benchmark prices declined to RMB 855/t and moved sideways on this level until further declines in November and December amid weaker-than-expected demand for winter heating.

This year’s dynamics look more complex. Prices have seesawed but retained an upward bias, supported by utility restocking and the government’s campaign against overproduction at coal mines and price wars in other resource sectors. Even so, fundamentals appear more balanced, with supply constraints offset by tempered consumption, suggesting narrower price swings than in past years.

Having said that, there are still some swing factors that could shape the market trend. For example, pre-holiday buying among utilities was lighter than expected, leaving room for catch-up procurement that could lend support once China reopens after the break.

Meanwhile, flexible purchasing by industrial users can also deliver sudden jolts to market sentiment, adding volatility.

Thirdly, after the holiday, ensuring sufficient energy supply in winter becomes a political priority, but as 2021 showed, peak-season demand does not always guarantee higher prices.

Taken together, analysts expect prices to largely hold steady or edge higher after the holiday, rather than break into sharp rallies or collapses. The picture, they say, is of a market that has matured, one shaped less by panic or speculation, and more by market discipline and seasonal nuance.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply