- BF-origin rebar prices drop by INR 200/t w-o-w

- Flat steel affected by liquidity crunch, GST ambiguity

- Market expects marginal price improvement before Diwali

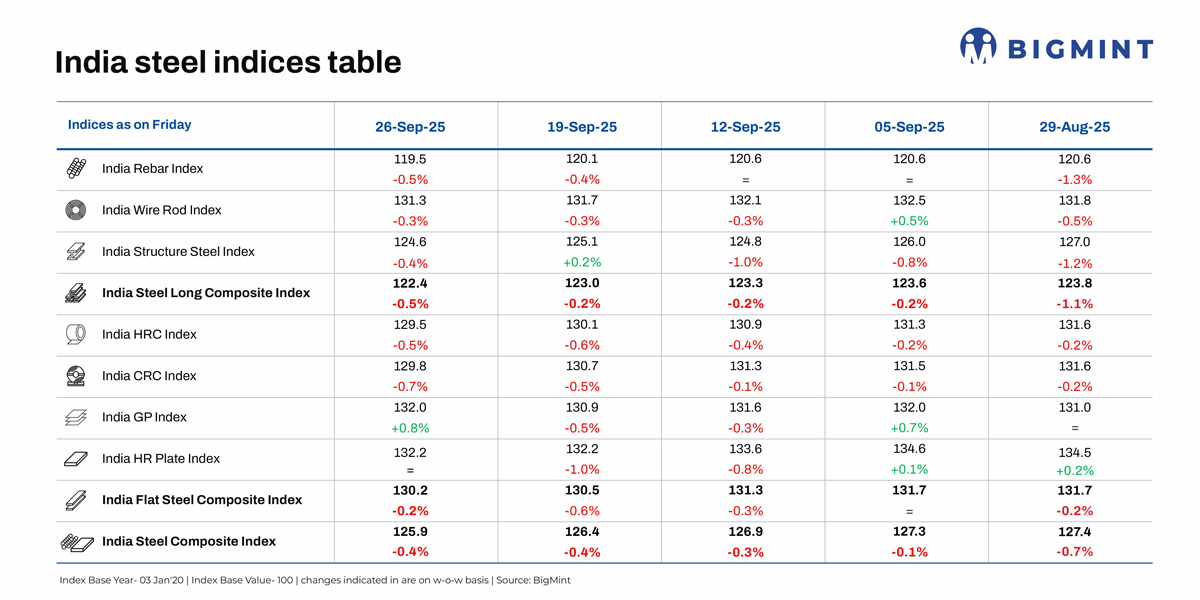

Morning Brief: BigMint’s India steel composite index, a barometer of the domestic steel market, continued to hover at multi-year lows in end-September 2025 due to several factors, but mainly an extended monsoon and its impact on economic activities, particularly construction and infrastructure, and weak global sentiments.

The composite index edged down by 0.4% w-o-w. The flats composite index declined 0.2% w-o-w compared with the 0.5% drop in the longs index. That this is despite the decline in steel imports in August and September goes to show that internal demand-supply pressure is weighing on domestic flat steel prices. The index is hovering at nearly 5-year lows.

Highlights of price movements

Rebar prices trend lower: Trade-level BF rebar prices edged down by INR 200/tonne (t) ($2/t) w-o-w to INR 46,800/t ($528/t) exy-Mumbai, as per BigMint’s assessment on 26 September. Prices are exclusive of GST at 18%. The primary mills either increased their discounts or reduced list prices due to subdued market sentiments. Demand was impacted due to heavy monsoon downpour in different regions and the descent of a festive season lull on key markets across regions.

The projects segment witnessed low activity as buyers were on the sidelines amid monsoons and logistics challenges. Rebar inventories at mills remained at high levels. A major PSU steel mill is expected to take a shutdown next month, market sources informed.

IF-rebar trade prices declined, too, amid subdued activities owing to festive season and heavy rainfall in some regions, especially central and eastern India. Inventory levels were high at 12-15 days across regions. Prices dropped INR 700/t ($8/t) w-o-w to INR 43,700/t ($493/t) exw-Mumbai on 26 September.

Flat steel prices under pressure: BigMint’s benchmark assessment (bi-weekly) for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) decreased marginally by INR 100/t ($1/t) w-o-w to INR 49,100/t ($553/t) on 23 September against INR 49,200/t ($554/t) on 16 September. Trade-level HRC prices, however, stayed firm w-o-w at INR 48,000-50,200/t ($541-566/t). Cold-rolled coil (CRC) prices showed a slight downtrend w-o-w, with prices ranging between INR 54,000-58,300/t ($609-657/t).

The HRC market remained weak, with buyers limiting purchases to immediate needs. GST cuts and festive holidays added uncertainty. The expected recovery in demand now seems unlikely in the near term, sources informed. Adding to the uncertainty, recent GST cuts introduced on 22 September have left the market in a state of flux as traders are watching closely to gauge how these changes might affect pricing and demand.

Additionally, the festive season of Durga Puja, which is currently underway, has slowed down trade, particularly in eastern India.

Outlook

With the safeguard duty in place, AD duty on imports from key countries and now a proposal for imposition of further duties on certain steel grades for specialised applications, trade remedial measures have offered support to domestic producers amid market slowdown. Landed cost of imports from key countries are higher than domestic prices.

Domestic steel prices will most likely remain rangebound in the near term, with a slight rebound likely ahead of Diwali. Flat steel export offers may stay under pressure in the short term, driven by cautious market sentiment and the approaching CBAM. This will be a drag on domestic prices too. Liquidity constraints and uncertain market conditions may limit demand.

Longs prices, on the other hand, have been weighed down by need-based buying amid monsoon disruption. But market participants are hopeful of a turnaround in October.

Leave a Reply