- HRC prices remain steady amid need-based buying

- IF rebar tags show mixed trends amid slow offtake

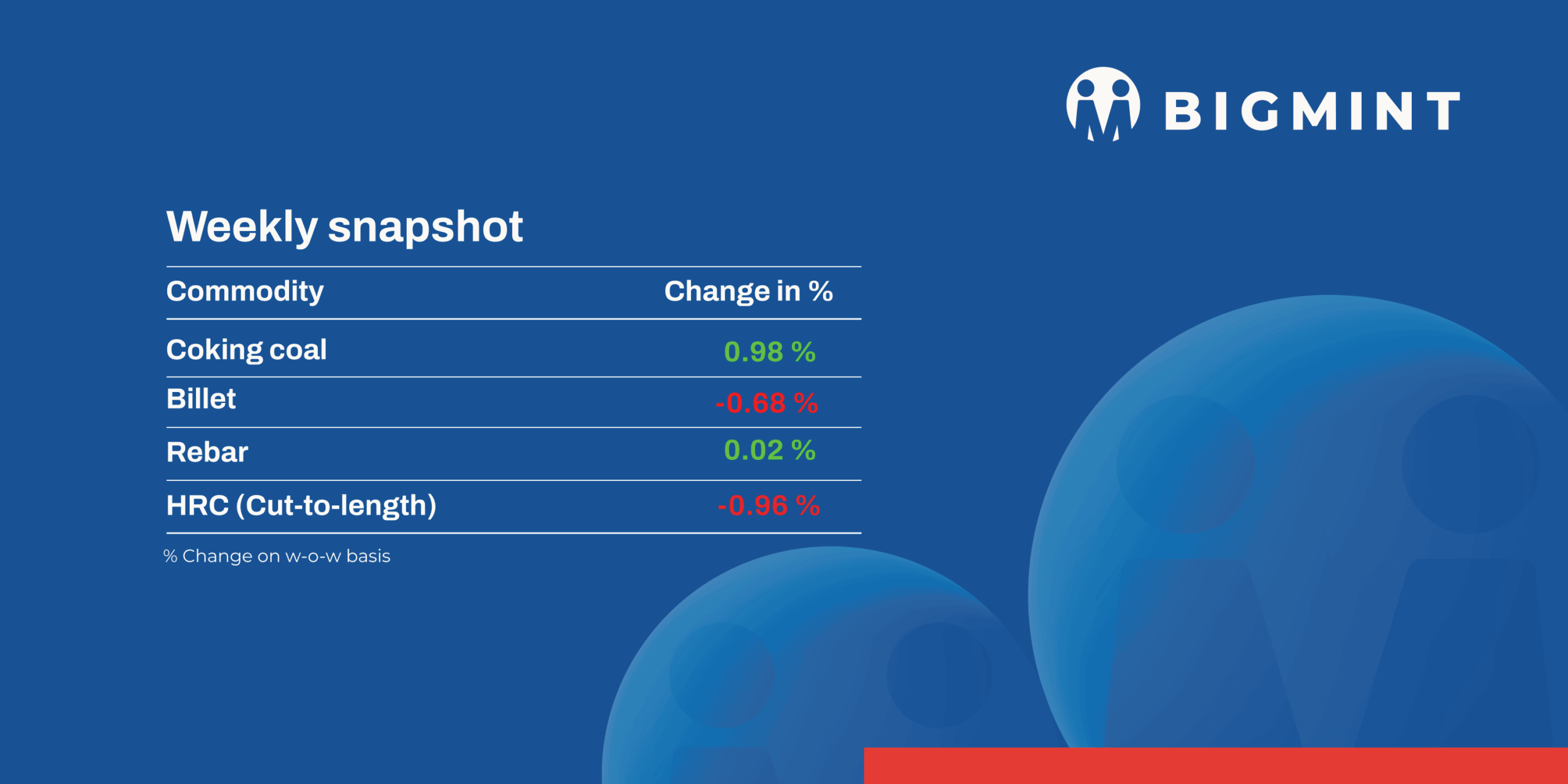

The domestic steel market witnessed a downtrend during Week 39 (22-27 September 2025). Semi-finished steel prices registered a decline in the range of INR 50-800 /tonne (t) across major trading regions. Overall, a recovery in the market is expected following the festive season.

Iron ore, pellet

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index rose by $1/t w-o-w to $68.5/t FOB east coast on 25 September. BigMint recorded export deals for nearly 460,000 t of fines during the recent trading sessions. Cargoes for Fe 56-57% fines were finalised in the range of $78-81/t CFR China. Discounts for Indian-origin Fe 57% fines were stable, at around 18-18.5% in the overseas market, and deals were largely concluded in the same range.

- NMDC Karnataka auctioned 188,000-t iron ore from its Kumaraswamy mines, Karnataka, on 24 September. The entire quantity was booked, with lumps fetching premiums of INR 1,000-1,070/t (20.4%) and fines up to INR 650/t (14.8%). 64,000-t lumps (10-40 mm, Fe 61.45-62.59%) were booked at INR 5,909-6,309/t against base prices of INR 4,909-5,239/t, with 124,000-t fines (Fe 58.86-62.49%) sold at INR 3,530-5,029/t against INR 3,520-4,379/t.

- At NMDC CG’s auction for 61,900 t of iron ore from its Bacheli mines on 25 September, 12,900 t of DR CLO (Fe 67%) fetched 19% premium (base INR 6,910/t), while out of 6,000 t offered, 4,000 t of ROM (Fe 65.5%) were booked at base price of INR 6,050/t. However, 43,000 t of fines (Fe 64%) remained unsold at the base price of INR 5,290/t. Prices were FOR basis plus royalty, DMF, and NMEDT.

Coal

- India’s met coke market stayed firm this week, with BF-grade assessed at INR 29,500/t ex-Jajpur and INR 30,000/t ex-Gandhidham, while the foundry grade held at INR 35,600/t ex-Rajkot. Trading momentum came from bulk bookings, though imports fell sharply, pushing dependence on domestic supply. Australian PHCC was up by $1/t w-o-w to $190/t FOB. Prices are expected to stay range-bound until clarity emerges on quantitative restrictions.

- South African portside coal prices in India edged higher this week following GST changes, but trades remained thin. At Vizag, RB2 increased INR 450/t to INR 8,200/t and RB3 rose INR 300/t to INR 7,100/t. At Gangavaram, RB2 climbed up by INR 300/t to INR 8,200/t, while RB3 also gained INR 300/t to INR 7,100/t. Despite these higher offers, active deals were scarce, with limited RB2 trades reported at INR 8,150-8,200/t.

- Coal prices in India held steady this week, with 5,000 GCV assessed at INR 5,750/t ex-Bilaspur and 4,500 GCV at INR 4,900/t. In SECL’s 24 September auction, sponge-grade coal fetched notable premiums, highlighting firm demand in select segments. However, overall sentiment remains cautious, with traders and buyers awaiting delivery-linked price impacts.

Ferrous scrap

- India’s imported scrap market stayed weak through the week, pressured by subdued steel demand, sufficient domestic supply, and cheaper alternatives. Buyers avoided raising bids, leaving trade activity limited. Shredded offers held at $360-365/t CFR against bids at $355-360/t, while HMS hovered at $330-335/t depending on origin. Despite varied offers, muted demand and currency pressure capped buying interest.

- Towards week’s end, Chennai saw fewer arrivals as Australian cargoes diverted to Indonesia, while UK turnings gained traction in western India.

- Around 10,000-11,000 t of imported scrap were booked, including 5,000-6,000 t of HMS 80:20 at $330-340/t, with the balance comprising bundle scrap, turnings, busheling, and hand-loaded HMS.

Ferro alloys

- Silico manganese: Indian silico manganese prices (60-14) rose by INR 500/t ($7/t) w-o-w to INR 69,400-69,800/t ($783-787/t) in the key regions of Durgapur, Raipur, and Vizag. amid tightening supply conditions. Transportation challenges caused by monsoon-related disruptions in key regions further constrained supply, creating a supply-demand gap.

- Additionally, on 25 September 2025, SMIORE auctioned 31,248 t of manganese ore (20%-34% Mn, -10 to 100 mm). Moderate participation led to 11,088 t sold (35%), with 20,160 t unsold.

- Ferro manganese: Indian ferro manganese (HC 70%) prices continued to fall, by INR 200/t ($2/t) w-o-w to INR 70,200/t ($792/t) exw in Durgapur. Meanwhile, prices, exw-Raipur, also inched down by INR 200/t($2/t) to INR 70,300/t ($793/t) w-o-w. Prices dipped as subdued demand persisted, while steady supply kept the market under pressure.

- Ferro silicon: Indian ferro silicon prices were largely steady with a slight dip of INR 400/t ($5/t) w-o-w to INR 88,300/t ($996/t) exw-Guwahati. Meanwhile, Bhutanese offers also declined by INR 400/t ($5/t) to INR 88,000 ($992/t). Trading was largely quiet, as the most sellers were out of the market.

- Ferro chrome: Additionally, at the ferro chrome auction on 22 September, 1,650 t of the 3,300 t offered were sold, all from the larger lot (Cr: 60-64%, 10-100 mm) at the base price of INR 117,500/t ($1,325/t) exw.

Semi-finished

- Indian semi-finished steel prices trended down, as per BigMint’s assessment. Domestic billet prices in all key locations decreased by INR 50-800/t ($1-9/t) due to need-based buying. Weak finished steel demand kept sentiment subdued, pushing semi-finished sellers to cut offers to spur trades. However, a small number of regions witnessed a hike of INR 100-600/t ($1-7/t).

Sponge iron

- Sponge iron prices dropped in all regions, by INR 100-450/t ($1-5/t) as muted downstream demand forced sellers to cut offers to spur buying. However, cautious buyers limited purchases to immediate needs, keeping inquiries sparse amid uncertain price trends.

- Indian direct reduced iron (DRI) export offers increased by $6/t to $335/t CPT Raxaul, while CPT Benapole offers increased by $9/t to $346/t.

Finished long steel

- IF-rebar: India’s induction furnace (IF) route rebar prices saw mixed trends amid slow demand, with buyers only fulfilling immediate needs. Trading activity was subdued across regions, mainly hampered by ongoing festivals and heavy rainfall. This cautious sentiment led buyers to avoid bulk purchases. Market participants highlighted that the slow lifting caused stocks to pile up, with inventory holding periods at around 12-15 days, although this varied location wise. Market participants expect prices to remain range-bound in the near term.

- On a w-o-w basis, rebar prices varied in the range of INR 100-900/t, as per BigMint’s assessment.

- Trade reference prices of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size were assessed at INR 39,500-39,900/t exw Raipur and INR 42,800-43,400/t exw Jalna.

- Trade reference prices of heavy structural steel for base size 150mm channel stood at INR 41,700-42,200/t exw Raipur.

- Trade reference prices of wire rod hovered at INR 40,000-40,500/t ex-Raipur.

- BF-rebar: India’s trade-level blast furnace (BF) rebar prices dropped w-o-w across major markets. Major primary mills either increased their discounts or reduced list prices due to subdued market sentiments. Buying activities were impacted by heavy rains and the festive season across major Indian markets.

- Trade-level BF rebar prices edged down by INR 200/t ($2/t) w-o-w to INR 46,800/t ($528/t) exy-Mumbai, as per BigMint’s assessment on 26 September 2025. Prices are exclusive of GST at 18%.

- In the projects segment, prices hovered between INR 45,500-46,500/t ($513-524/t) FOR Mumbai. The project segment witnessed low activity as buyers were on the sidelines amid the monsoon and logistics challenges.

Flat steel

- Trade-level prices of hot-rolled coils (HRCs) in India stayed firm w-o-w at INR 48,000-50,200/t ($541-566/t). However, cold-rolled coil (CRC) prices showed a slight downtrend w-o-w, with prices ranging between INR 54,000-58,300/t ($609-657/t)

- The Indian HRC market remained weak, with buyers limiting purchases to immediate needs. GST cuts and festive holidays added uncertainty, while the anticipated demand recovery remained uncertain, keeping sentiment cautious.

India’s bulk imports of HRCs touched 359,874 t as of 20 September, based on vessel line-up data. Around 214,104 t of additional cargoes are expected by mid-October. - India’s bulk exports of HRCs touched 101,523 t as of 20 September, and around 85,850 t of additional cargo are being shipped.

BigMint’s India hot-rolled coil (HRC, S275 for Europe) export index remained stable w-o-w at $545/t (FOB main port) amid weak domestic demand. The European HRC market stayed subdued due to weak demand from end-users and ongoing uncertainty surrounding forthcoming regulatory changes, keeping market activity quiet. - Indian HRC (SAE1006) export index for the Middle East remained unchanged w-o-w at $500/t FOB main port. With a slow market and the year-end approaching, customers are holding back on building up inventory, sources informed.

Leave a Reply