- Turkish semis tags drop w-o-w; import restrictions tighten

- Clear price direction expected in China post-Golden Week holidays

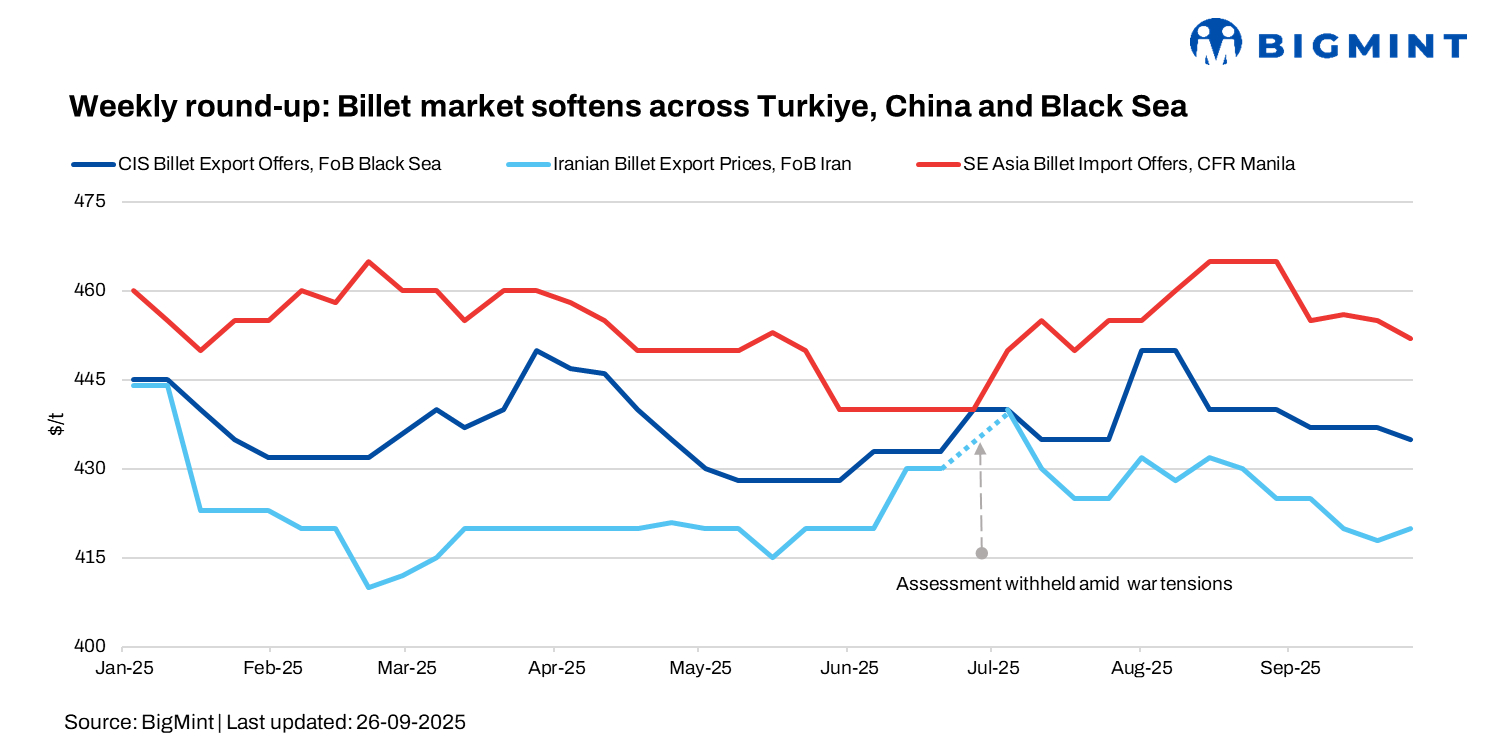

In week 39 of 2025, global billet prices eased across key regions, including Turkiye, Russia, and China. Chinese exporters are boosting overseas shipments amid strong regional competition, with Indonesia, Malaysia, Vietnam, Iran, and Russia actively seeking discounted semi-finished material.

In Turkiye, the imported deep-sea scrap market started subdued, with US/Baltic HMS 80:20 at $330-335/t CFR and EU-origin at $325-330/t CFR. Weak steel demand and soft prices limited buying interest, while sellers faced pressure from falling European collection rates. Prices gradually recovered on tighter supply, with US/Baltic HMS 80:20 reaching $342/t CFR and EU-origin at $332-335/t CFR–driven more by constrained availability than stronger mill demand.

Southeast Asia & China:

Over the past month, imported billet in Southeast Asia rose by $4-8/t to $460-465/t CFR, while Chinese exports of semis eased $2-3/t to $440-443/t FOB.

Weak domestic demand in China, driven by real estate struggles and a slowing economy, limits support for semi-finished steel prices. Finished steel inventories remain high despite reduced output, and the market expects no meaningful recovery in the coming months. Slight price gains may appear closer to winter if production is curtailed and new economic stimulus emerges.

Chinese exporters are boosting overseas shipments amid strong regional competition, with Indonesia, Malaysia, Vietnam, Iran, and Russia actively seeking discounted semi-finished material.

Tangshan billet prices fell RMB 60/t ($8/t) w-o-w to RMB 2,990/t ($425/t), while SHFE Jan’26 rebar futures dropped RMB 71/t ($10/t) to RMB 3,114/t ($443/t). Ahead of Golden Week, weak demand and completed restocking pushed markets to multi-week lows. A clearer price direction is expected post-holidays, with limited support from volume control policies.

Black Sea & Turkiye

In the Black Sea region, prices were largely stable as most mills nearly sold out October production. Russian semis for November were assessed at $440–445/t FOB, with CIS shipments to Turkiye at $460-465/t CFR ($440-445/t FOB). Notable deals included Russian lots at $460/t CFR ($440/t FOB) and $455-460/t CFR ($435/t FOB), with no major changes expected after recent Kardemir purchases.

In Turkiye, imported billets eased $3-5/t to $452-455/t CFR, and domestic semis declined $10/t to $490-500/t exw. Rising scrap prices and restocking may support costs, though new restrictions–shortened import certificate validity and 25% domestic sourcing–are likely to constrain imports. Domestic demand remains weak, mainly from government projects, while private consumption struggles with high material costs and limited orders.

Iran: Billet prices rose 10,500 rial/kg ($25/t) to 351,000 rial/kg ($835/t), and rebar gained 15,000 rial/kg ($36/t) to 395,000 rial/kg ($939/t), supported by strong exports and a rising exchange rate. Supply remains tight, with billets sold out at the Iran Mercantile Exchange. Snapback sanctions may fuel stagflation, raise forex and interest rates, and limit investment.

Iran’s billet export market remains subdued. Producers offer $415-420/t FOB, above current market levels of $410-415/t, while traders quote $390-395/t FOB, down from $395-400/t. Activity is limited by domestic regulations and political tensions, though selective trade continues.

UAE & other GCC

In September, UAE billet offers ranged $485-505/t CFR and exw depending on origin, with Chinese billets at $460-470/t CFR. Iranian billets eased to $415-420/t FOB. Asian suppliers show limited scope for price growth, as rising supply offsets post-rainy-season demand. Re-rollers in the UAE earn positive margins (nearly $30/t), Omani companies achieve better than $100/t exw, while Saudi re-rollers remain under pressure; a $10/t decline in offers could improve profitability.

Leave a Reply