- Sponge-grade coal shows selective demand strength

- Imported coking coal prices into India stable w-o-w

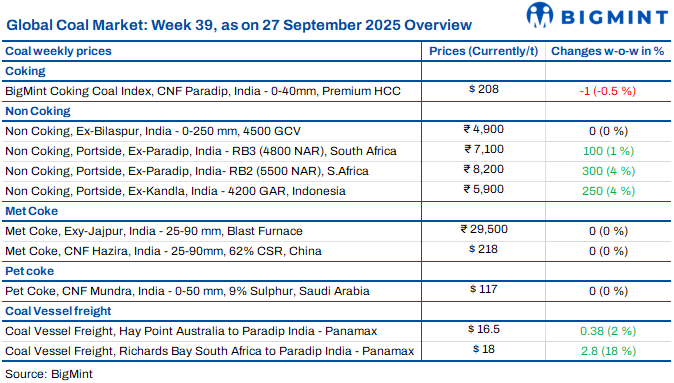

The coal market stayed cautious this week as participants adjusted to GST-linked changes. Sellers lifted offers on older inventories to recover cess, while buyers preferred to wait for clarity before committing to fresh bookings. Domestic auctions reflected selective demand, with sponge-grade material fetching premiums. Meanwhile, muted activity in sponge iron and steel segments capped aggressive restocking. The market is expected to remain range-bound until demand revival post-monsoon.

Portside Indonesian coal prices firm post-GST

Indian portside Indonesian thermal coal offers firmed during the week ending 26 September 2025 as traders adjusted for cess-loaded older inventories following GST reforms. BigMint assessed 5000 GAR at INR 7,100/t in Kandla and INR 7,000/t in Vizag, while 4200 GAR rose to INR 5,900/t and INR 5,800/t respectively. Navlakhi’s 3400 GAR grade climbed to INR 4,500/t. Coal inventories at Indian power plants slipped further, sufficient for only 16 days of consumption, leaving 18 plants under critical stock status. International prices recorded mild gains, with 5800 GAR at $76.48/t, 4200 GAR at $43.87/t, and 3400 GAR at $30.63/t. Portside prices are expected to stay firm near term, though new cess-free arrivals and easing global freights may cap sharp gains.

South African portside coal offers rise

South African portside coal prices in India edged higher this week following GST changes, but trades remained thin. At Vizag, RB2 increased INR 450/t to INR 8,200/t and RB3 rose INR 300/t to INR 7,100/t. At Gangavaram, RB2 climbed INR 300/t to INR 8,200/t, while RB3 also gained INR 300/t to INR 7,100/t. Despite these higher offers, active deals were scarce, with limited RB2 trades reported at INR 8,150-8,200/t. Seaborne dynamics shaped sentiment as an RB3 Panamax cargo was fixed at $57/t FOB Richards Bay for mid-October, while an RB2 Panamax shipment was booked at $86/t CNF India for November. Export offers softened $2/t w-o-w, with RB2 at $69/t FOB and RB3 at $58/t FOB. Outlook remains cautious, with prices expected to stay range-bound until post-monsoon demand improves.

Domestic coal prices stable

Coal prices in India held steady this week, with 5,000 GCV assessed at INR 5,750/t ex-Bilaspur and 4,500 GCV at INR 4,900/t. In SECL’s 24 September auction, sponge-grade coal fetched notable premiums, highlighting firm demand in select segments. However, overall sentiment remains cautious, with traders and buyers awaiting delivery-linked price impacts before committing to larger volumes.

Coking coal index steady as buyers wait for fresh deals

BigMint’s premium hard coking coal (PHCC) index held steady at $208/t CNF Paradip on 27 September, edging only $1 lower from last week. No fresh Indian bookings were reported, though inquiries are expected to rise as steel demand recovers in Q3FY’26. Globally, Australian coking coal gained to $190/t FOB, driven by Chinese demand and supply issues in Queensland. Indian post-monsoon restocking may support trade, though momentum remains uncertain.

Met coke market steady as buyers weigh supply risks

India’s met coke market stayed firm this week with BF-grade assessed at INR 29,500/t ex-Jajpur and INR 30,000/t ex-Gandhidham, while foundry-grade held INR 35,600/t ex-Rajkot. Trading momentum came from bulk bookings, though imports fell sharply, pushing dependence on domestic supply. Australian PHCC up by $1/t w-o-w to $190/t FOB. Pig iron weakness limited met coke demand, keeping overall sentiment cautious. Prices are expected to stay range-bound until clarity emerges on quantitative restrictions.

Imported pet coke market steady; buyers eye imports

Imported pet coke offers in India stayed unchanged w-o-w, with BigMint assessing US-origin at $118-120/t CFR and Saudi-origin at $117-119/t CFR. Domestic supply constraints from reduced Nayara output and shutdowns at Kochi and CPCL have steered demand toward imports, with cement makers already booking US cargoes for October. However, the removal of cess on coal from 22 Sep could weigh on pet coke prices in the longer term.

Coal freights show mixed movement across trade lanes

Dry bulk coal freights moved unevenly this week. On the Australia (Hay Point)-India (Paradip) Panamax route, rates edged down by $0.38/dmt to $16.50/dmt. South Africa (Richards Bay)-India (Paradip) Panamax freights rose sharply by $2.8/dmt to $18/dmt, supported by tight vessel supply. In contrast, Indonesia (East Kalimantan)-India (Navlakhi) Supramax freights fell by $1.24/dmt to $14.47/dmt on muted export demand. The Baltic dry index increased by about 60 points to 2,240, though Panamax fell 99 points to 1,824 and Supramax dipped 9 points to 1,483. Near term, South Africa and Australia routes may stay firm, while Indonesia remains under pressure.

Leave a Reply