- Manufacturing activity contracts for 5th consecutive month

- Production curbs drag down coal, crude steel output m-o-m

- Auto continues to shine; sales, output top 20 mnt for 1st time

Morning Brief: China’s steel ecosystem continued to wrestle with macroeconomic headwinds in August, foremost among these being the protracted uncertainty surrounding the US tariffs, though the heightened volatility of the previous months was somewhat absent.

Steel and coal production continued to decline m-o-m, in keeping with the government’s aims to curb overproduction. In contrast, iron ore imports increased marginally m-o-m.

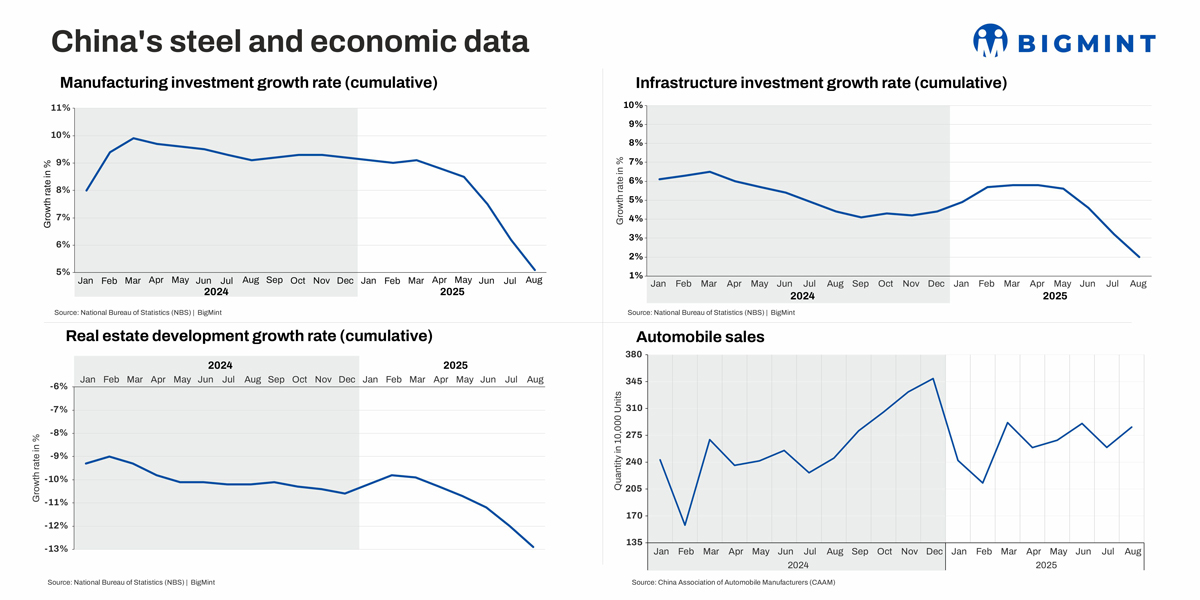

Except for the auto sector, which continued to shine, key steel-user segments contracted, recording waning investment growth. Overall, a grim mood prevailed, contributing to subdued steel demand trends.

Production curbs pull down crude steel output

China’s crude steel production edged down by 0.7% y-o-y and 2.9% m-o-m to 77.37 million tonne (mnt), the third consecutive month with a decline and the lowest volume since December.

Production restrictions ahead of the Victory Day military parade, held on 3 September in Beijing, led to lower volumes last month, and the impact continued.

As per Mysteel, mills in three of the top five crude steel-producing regions in China — Hebei, Shandong and Shanxi — were hit with these government-mandated sanctions, which aimed to ensure clean air during the parade.

Sluggish demand due to the summer off-season also prompted steelmakers to reduce production. Persistent losses also forced electric arc furnace (EAF) units to slash production.

Additionally, pig iron output stood at 69.79 mnt in August, a 1% increase y-o-y and 1.4% dip m-o-m.

Steel exports drop m-o-m as domestic prices rise

Steel exports declined by 3.3% m-o-m to 9.51 mnt, though volumes inched up by a marginal 0.1%.

As per Mysteel, August’s shipments were mainly for bookings made in June, during which heavy rains and muted construction activity had weighed on demand for steel. US tariff-driven uncertainties also dampened volumes. Moreover, a brief upturn in Chinese steel prices in July-August also prompted mills to focus on domestic bookings.

However, changes in export tax regulations, expected to take effect from 1 October, prompted some front-loading, and overall subdued domestic demand ensured volumes remained high.

Market optimism drives up iron ore imports m-o-m

Iron ore imports into China totalled 105.23 mnt in August, up by a minor 0.6% m-o-m while edging down by 1.6% y-o-y. Imports remained above 100 mnt for the fourth straight month.

Iron ore imports were buoyed by a supply surge from Australian miners, who pushed record output into the market. Additionally, optimism ahead of China’s peak steel consumption season from September made mills keen to build up their iron ore stocks. Lower prices in the second quarter (with monthly averages remaining below the $100/t mark) and a 5% y-o-y uptick in hot metal output also kept import appetite strong.

However, lower flat crude steel output, production restrictions on mills, and a sustained steel demand slump likely weighed on volumes.

Coal output falls y-o-y amid crackdown on overproduction

China’s coal production dipped by 3% y-o-y in August to 390.5 mnt, though volumes recovered from July’s one-year low of 380.99 mnt. Production curbs, aimed to address overcapacity problems amid an unexpected surge in output in H1CY’25 and continued depression in pricing, continued to reduce volumes. Safety inspections were also initiated in July ahead of the military parade on 3 September.

Coal imports continue rising m-o-m

China imported 42.74 mnt of coal and lignite in August, surging by 20% m-o-m but down 6.8% y-o-y. This marks the second straight month with an m-o-m increase and the highest volume in eight months.

Scorching temperatures due to the summer led to an increase in thermal power generation and, thus, pushed up coal demand. Given lower domestic output and higher prices of the same, imports turned more attractive.

Cement production falls, construction segment struggles

Cement production fell by 6.2% y-o-y to 148 mnt in August, though output inched up from July’s 146 mnt, a 16-year low. The continuing property market collapse, poor real estate investments, weak consumption trends, and weather-driven disruptions in construction activity have prompted cement manufacturers to scale back production.

Notably, the growth rate for real estate development in January-August was at a steep low of -12.9%, while the same for infrastructure stood at an equally poor 2%. Both were at multi-year lows.

Auto sales, output top 20 mnt for first time

Both production (21.051 million) and sales (21.097 million) in the automobile segment surpassed 20 million units in January-August, a first for China, fuelled by substantial government subsidies and favourable consumption-boosting policies. In August, the strong growth momentum continued, with production and sales volumes up by 8.7% and 10.1% m-o-m, respectively. Auto exports hit 4.3 million units in the first eight months, up 13.7% y-o-y.

The new energy vehicles (NEV) segment continued to drive growth, with January-August production at 9.6 million, rising by 37.3%. Sales volumes also surged parallelly.

However, reports suggest that despite strong sales on paper, China continues to grapple with a supply glut. Aggressive price undercutting kept auto producers margins under stress.

Manufacturing activity shrinks for 5th straight month

China’s official manufacturing purchasing managers’ index (PMI) stood at 49.4 points in August, indicating a contraction in activity. Notably, this is the fifth consecutive month with the PMI below the 50-point mark. US tariffs continued to foster caution about procuring from China, slowing export orders for the month. Subdued domestic demand also generated pessimism.

The production sub-index was at 50.8, however, increasing from 50.5 in July. This suggests that manufacturing production continued to expand, though overall activity shrank.

Additionally, manufacturing investment growth was at 5.1%, down a sharp 1.1 percentage points from July, indicating continued erosion of business confidence.

Outlook

Growth in China’s steel industry is expected to remain fragile, contingent on a sustained recovery in domestic demand and construction activity, as well as the strength of expected stimulus measures.

September generally heralds the peak steel consumption season, and optimism persists about a moderate market rebound. However, early data suggests that the recovery has been weaker than expected, with steel inventories remaining elevated.

Leave a Reply