- Subdued demand weighs on market

- Monsoon impacts IF rebar prices

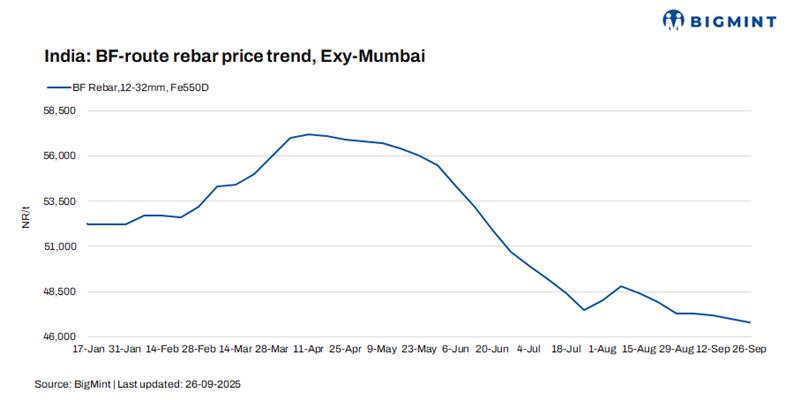

India’s trade-level blast furnace (BF) rebar prices dropped w-o-w across major markets. The major primary mills either increased their discounts or reduced list prices due to subdued market sentiments. Buying was impacted due to heavy monsoons and festive season lull seen across major domestic markets.

Trade-level BF rebar prices edged down by INR 200/tonne (t) ($2/t) w-o-w to INR 46,800/t ($528/t) exy-Mumbai, as per BigMint’s assessment on 26 September 2025. Prices are exclusive of GST at 18%.

In the projects segment, prices hovered between INR 45,500-46,500/t ($513-524/t) FOR Mumbai. The projects segment witnessed low activity as buyers were on the sidelines amid monsoons and logistics challenges.

Rebar inventories at mills remained at high levels amid weak market sentiments. A major PSU steel mill is expected to take a shutdown next month, market sources informed.

Update on projects

- L&T secures major order from NHSRCL for 156 km track works on Mumbai-Ahmedabad bullet train project using Shinkansen technology.

- L&T’s Heavy Civil Infrastructure secures key order from NPCIL for reactor, turbine, and systems installation at Kudankulam Units 5 & 6.

- L&T secures large STATCOM and SCADA orders in India, UAE, and Oman to enhance grid stability, resilience, and energy efficiency.

- L&T’s Construction & Industrial Products vertical secures significant orders across mining, tyre machinery, and valve segments in India and abroad.

- KEC International secures record EPC orders worth ₹3,243 crores for T&D projects in UAE and tower supplies in the Americas.

- Rail Vikas Nigam Limited (RVNL) emerges as the lowest bidder (L1) for a project from Southern Railway & West Central Railway, in the normal course of business.

Factors behind drop in prices

1. IF-rebar prices drop w-o-w: IF-rebar trade prices witnessed a drop w-o-w across markets. Trade prices dropped this week amid subdued activities owing to festive season and heavy rainfall in some regions, especially central and eastern India. Inventory levels were still high at 12-15 days across regions. IF rebar prices fell INR 700/t ($8/t) w-o-w to INR 43,700/t ($493/t) exw-Mumbai as of 26 September.

The BF-IF rebar price gap stood at around INR 3,000-3,500/t ($34-39/t) in Mumbai. IF rebars hold a dominant 65-70% market share in India.

2. Raw material prices drop w-o-w: BigMint’s Odisha iron ore fines (Fe 62%) index edged down by INR 200/t ($2/t) w-o-w to INR 5,300/t ($60/t) ex-mines on 20 September. Iron ore prices in Odisha declined following the conclusion of the Odisha Mining Corporation (OMC) auction. The price correction was driven by a sharp drop of nearly INR 350/t ($4/t) in auction bids, which influenced broader market sentiment.

Australian premium hard coking coal (PHCC) prices were stable w-o-w at $204/t CNF Paradip.

Outlook

Market participants are still cautious but feel that prices may have bottomed out and expect a recovery next month.

Leave a Reply