- Buyers remain cautious regarding fresh deals, wait for clarity

- Sponge iron, semis prices decline by INR 300-500/t w-o-w

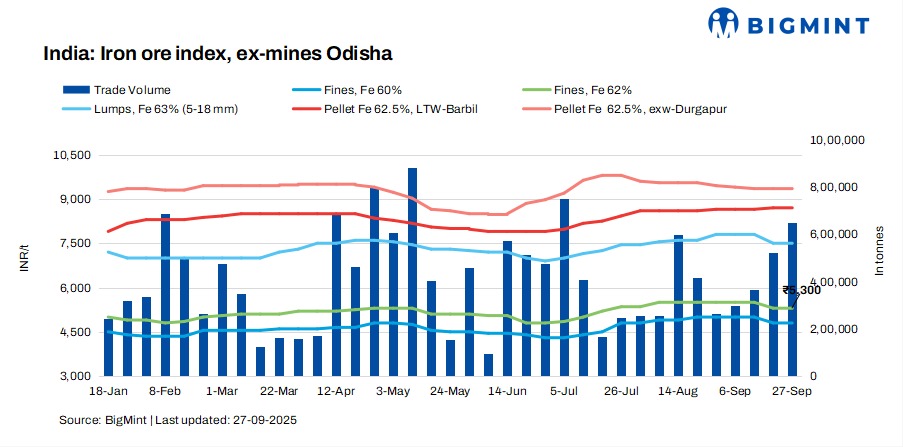

Iron ore prices in the Odisha region remained largely stable this week despite expectations of volatility following the September OMC auction. Market participants noted that a shortage of material, stemming from reduced production due to continuous rainfall and limited offers by miners, tightened supply in the spot market.

Price update

BigMint’s Odisha iron ore fines (Fe 62%) index remained stable w-o-w at INR 5,300/tonne (t) ($60/t) ex-mines on 27 September 2025. BigMint recorded deals for around 650,000 t in Odisha, concluded by direct sales. A few bulk deals for the October delivery were heard this week following the OMC auction.

In the SAIL Bolani mines auction, the entire 43,000 t of CLO (Fe 62.5%) were booked at the base price of INR 6,850/t on 26 September.

Market highlights

Only a handful of miners actively offered material, while many remained away from the market due to limited availability. A miner said, “Dispatches from earlier bookings are still pending, which is why we are not in a position to accept new orders at the moment.”

On the buyers’ side, mills adopted a wait-and-watch approach, as steel prices continued to decline. A buyer noted, “There is little interest in fresh procurement, as steel prices have softened, impacting margins for secondary producers.”

Meanwhile, despite bids in the September OMC auction falling sharply (INR 350/t in fines), miners held firm on their offers and resisted accepting lower bids. A trader informed BigMint, “The drop in auction bids does not impact other private miners’ prices. Miners are focusing on fulfilling prior commitments, not slashing prices.”

Export activity also played a role in shaping the domestic market. With exporters booking bulk shipments in recent weeks, higher export bids influenced the domestic segment. An exporter noted, “Exporters are willing to pay domestic suppliers more to fulfil their cargo commitments, which is indirectly supporting domestic offers.”

Overall, the market remains cautious, and participants expect pricing clarity in the coming week. Much will depend on policy announcements by the government, which traders believe could influence both domestic supply and export sentiment. Until then, volatility is likely to persist amid thin trade volumes and supply constraints.

Factors affecting iron ore prices

Pellet prices edge down w-o-w: Pellet (6-20 mm, Fe 62.5%) prices in Odisha’s Barbil inched down by INR 50/t ($0.5/t) w-o-w to INR 8,650/t ($98/t) loaded to wagon. Pellet (Fe 62.5%, 6-20 mm) prices in Durgapur fell by INR 50/t ($0.5/t) w-o-w to INR 9,300/t ($105/t) exw on 26 September.

Sponge iron prices fall w-o-w: According to BigMint’s assessment, sponge iron C-DRI (FeM 80%) prices in Rourkela decreased by INR 450/t ($5/t) w-o-w to INR 26,000/t ($293/t) on 27 September.

Billet prices drop w-o-w: Meanwhile, steel billet (100*100 mm) prices in Rourkela dropped by INR 300/t ($3.5/t) w-o-w to INR 36,000/t ($406/t) today.

Rationale

- T1- Two (2) deals for Fe62% fines were recorded in the publishing window, and were not considered for price computation. These were given 0% weightage for index calculation.

- T2 – BigMint received fifteen (15) offers and indicative prices under the T2 category (offers, indicative, and bids) in this publishing window. Ten (10) were taken into consideration and given 100% weightage. To check BigMint’s iron ore assessment, pricing methodology, and specification document, click here.

Outlook

BigMint’s analysis suggests that iron ore prices in Odisha are likely to remain volatile. Steelmakers are expected to gain clarity regarding tradable levels in the near term.

Leave a Reply