- Surging supplies from neighbouring Bhutan likely to pressure prices

- India’s reliance on Bhutan to rise despite import diversification

- Hike in power tariffs in the North East a critical challenge for industry

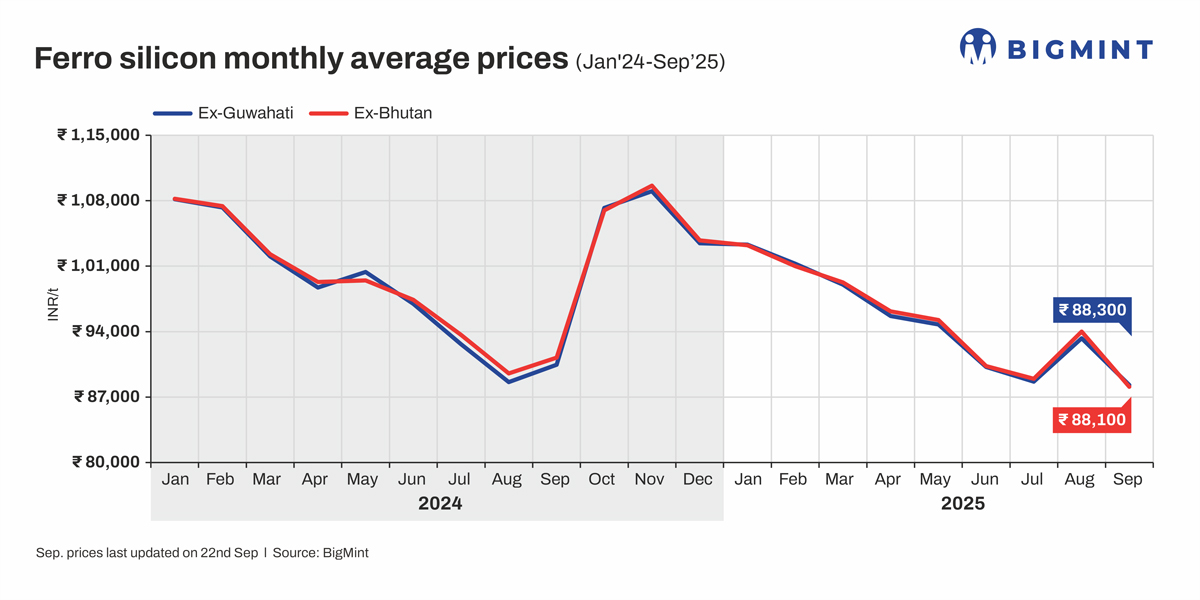

Morning Brief: Indian ferro silicon price trends remain heavily influenced by Bhutan’s prices. The neighbouring country is India’s largest supplier of ferro silicon and has an outsized influence in determining price dynamics. Amid fast growth in steel production, India’s dependence on Bhutan for ferro silicon, a key deoxidiser and alloying agent in steel and a critical ingredient in stainless steel production, is expected to increase.

For perspective, India produced much less ferro silicon last year than it actually consumed, importing around 200,000 t from different countries. Bhutan’s production of roughly 150,000-200,000 t of ferro silicon in CY’24 was majorly exported to India. Bhutan remained India’s largest ferro silicon supplier in H1CY’25, though its exports to India fell 20% y-o-y to 54,960 t, as per BigMint data.

In September, Bhutan opened prices at INR 86,000/t exw, a drop of INR 9,000/t m-o-m. Indian sellers also adopted the same price. But, as the month progressed, key Bhutan-based players reduced sales which created a supply deficit in the domestic market and led to a rise in prices.

Currently BigMint assesses ferro silicon (25-150 mm, FeSi 70%) at INR 88,000-89,000/t exw both in Bhutan and Guwahati – the key hubs.

Factors affecting Q4CY’24 price outlook

Surge in Bhutan’s capacity: Bhutan’s current monthly capacity production capacity of ferro silicon is around 15,000-16,000 t. Three new are expected to start production in the next quarter: ACE Himalayan Ferro Alloys (around 2,200 t monthly production), Samtse Ferro Alloys (2,400 t monthly) and BMML Ferro Alloys (around 2,400 t monthly). This will see total capacity addition of around 7,000 t per month.

According to reports from Bhutan, there are other companies with FDI partners from India, with stakes roughly between 50-75%. Data from Bhutan government sources show that as many as nine smelting units are coming up in Norbugang and a total of roughly 218,000 t of capacity is going to be added by the end of this year and next year.

With prices already low and higher production costs and CAPEX of the new units, the worry is that additional supply entering the market from the latter half of this year to next year could depress prices despite firm Indian demand.

India’s demand covered by imports: India’s monthly demand is estimated at around 30,000-35,000 t while production is around 15,000 t per month. Therefore, the reliance on imports is heavy and is also likely to increase, thanks to the phenomenal surge in steel production. India’s imports in January-August 2025 were assessed at over 155, 000 t, up nearly 20% y-o-y.

Although Bhutan remains the key supplier, supplies from Russia and Malaysia jumped by 220% y-o-y to 42,835 t in 8MCY’25 as against 13,378 t in the year-ago period. Diversification of import sources is apparent but a lot will depend on how Bhutan’s domestic supply scenario and pricing dynamics will evolve.

An additional worry is the upward revision in power tariffs in Bhutan as demanded by the BPC and the Druk Green Power Corporation (DGPC). Electricity accounts for around 30-35% of production costs.

North Eastern market scenario: Meghalaya is the primary hub of Indian ferro silicon production along with Guwahati and Arunachal Pradesh. However, domestic smelters are struggling with the rise in power tariffs. With the tariff at INR 7.10/unit in Meghalaya, a couple of plants have already stopped operations owing to the rise in power tariffs.

Domestic producers have to be competitive to match with Bhutanese prices and some buyers have a preference for Bhutanese material. The North Eastern market is largely influenced by Bhutan’s prices.

Silicon metal impact: Imported silicon metal has also been on the rise in recent months, particularly from China, as some end-users prefer it as an alternative to ferro silicon. However, with the INR depreciating recently against the USD and touching new lows recently, imports have gone down, as per sources.

This might lead to higher ferro silicon demand and offer support to prices, although the exact dynamics is as yet uncertain.

Outlook

The potential surge in supplies from Bhutan was the result of investments in fresh capacity, thanks to the boom time following the pandemic which saw prices and profits of ferro silicon soar. However, global steel dynamics has changed in 2025 and geopolitical and trade conflicts are weighing on the market and prices. Despite 8-9% growth in steel production in India, excess Bhutanese supplies may dent prices further. Price cutting among Bhutanese suppliers may also contribute to this trend.

However, as market chatter suggests, if Bhutanese suppliers resort to some sort of carbon pricing mechanism due to their far lower emissions intensity compared to India (thanks to hydropower), prices will increase for Indian buyers, although this is still a remote possibility.

India’s ferro silicon imports surged 20% in H1CY’25. Increased imports are likely to keep domestic prices under pressure but hike in production costs due to power tariffs will certainly not let prices drop beyond viable levels.

Leave a Reply