- Brazil extends recovery, Australia remains largely stable

- South African exports rise on improved freight availability

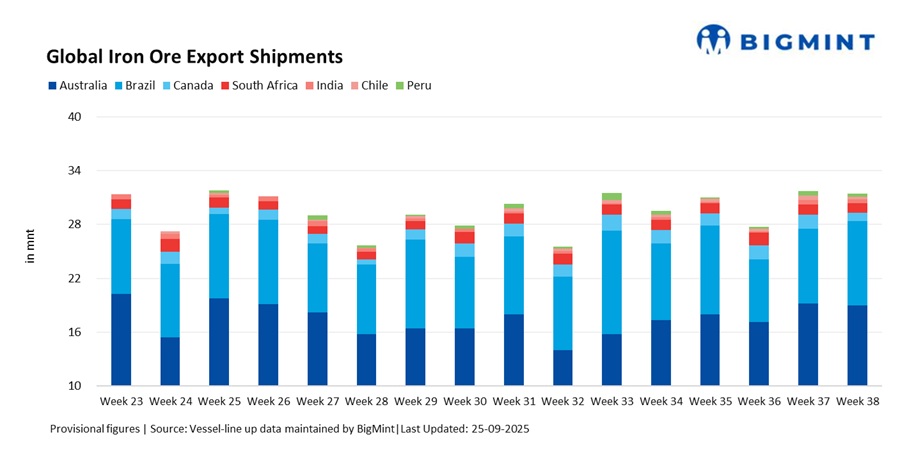

Global iron ore exports edged down by 0.7% w-o-w to 31.52 million tonnes (mnt) in Week 38 (13-19 September 2025) from 31.73 mnt in Week 37. The minor decline reflected weaker flows from Canada, India, Peru, and Chile, which offset gains from Brazil and a marginal improvement in South Africa. Market participants noted that while Australian volumes held largely steady, the dip in smaller exporters weighed on overall shipments.

Country-wise trends

Australia’s iron ore exports eased slightly by 1% w-o-w to 19.02 mnt in Week 38 from 19.22 mnt in Week 37, though overall volumes remained broadly stable. Loadings from Pilbara ports held firm, with Port Hedland dispatching 11.81 mnt, Walcott 3.94 mnt, and Dampier 3.05 mnt. Port Hedland shipments dipped slightly due to maintenance and softer demand, while Dampier recorded higher volumes thanks to more efficient operations and a favourable mix of cargoes.

Among major shippers, Rio Tinto led, with 6.99 mnt, followed by BHP at 5.73 mnt and FMG at 4.41 mnt, maintaining a strong pace despite subdued bids in the Pacific towards the week’s end. China remained the largest buyer at 15.67 mnt, with South Korea (1.43 mnt) and Japan (0.78 mnt) taking moderate volumes. Market sources highlighted that the slight dip in late-week fixtures reflected softer buying interest from some Chinese mills amid weaker steel margins, even as miner schedules stayed steady.

Brazil’s iron ore exports extended their recovery, rising 12.9% w-o-w to 9.36 mnt in Week 38 from 8.29 mnt in Week 37. The rebound was driven by increased activity at key terminals, including Ponta da Madeira at 4.26 mnt, Tubarao at 1.93 mnt, and Itaguai at 1.81 mnt. Vale dominated shipments, contributing 5.17 mnt, as the miner adjusted its scheduling to clear delayed parcels from earlier weeks.

China remained the primary destination, lifting 4.66 mnt, as improved Atlantic vessel availability and firmer fixture sentiment supported higher flows despite subdued steel demand. Market sources noted that while Brazilian exports remain sensitive to logistical bottlenecks and weather interruptions, the recent uptick reflected both catch-up operations and opportunistic scheduling in response to favourable freight dynamics.

Canada’s iron ore exports slumped 43% w-o-w to 0.91 mnt in Week 38 from 1.60 mnt in Week 37, as adverse weather and vessel scheduling delays disrupted flows. Sept-Iles handled 0.45 mnt, followed by Milne Inlet at 0.25 mnt and Port Cartier at 0.22 mnt. IOC was the leading shipper, dispatching 0.27 mnt.

On the demand side, Europe continued to dominate lifting, although limited cargo availability capped volumes. The Philippines emerged as a notable buyer at 0.18 mnt, while Belgium and Algeria lifted 0.15 mnt each. Market sources noted that the sharp decline was largely temporary, reflecting seasonal disruptions rather than structural weakness, but cautioned that weather-related risks could continue to impact Canadian exports.

South Africa’s iron ore exports posted a modest 2.6% rise w-o-w to 1.13 mnt in Week 38 from 1.10 mnt, with nearly all volumes handled through Saldanha Bay. The slight increase was supported by improved freight availability and steady demand, although rail and port constraints continued to limit further growth.

China remained the dominant buyer, lifting 0.82 mnt, as consistent restocking sentiment offset the impact from weak margins at domestic mills. However, Atlantic routes to China could face pressure in the near term due to muted fixture activity and limited cargo availability, leaving exports exposed to short-term volatility despite underlying demand strength.

India’s iron ore exports fell 18% w-o-w to 0.45 mnt in Week 38 from 0.55 mnt in Week 37, with Paradip handling the bulk at 0.29 mnt. The decline followed a sharp increase in Week 37, when exporters rushed cargoes amid speculation of a possible 30% export duty on low-grade iron ore from October. However, a source informed BigMint, “There is no government plan to impose export duty on low-grade materials; it was just a rumour,” highlighting the speculative nature of the earlier spike.

Heavy rains continued to disrupt mining operations in Odisha and Chhattisgarh, constraining production and adding volatility to exports. Market sources expect Indian exports to remain opportunistic in the short term, with volumes likely to normalise once seasonal mining conditions stabilise.

Chile’s iron ore exports slipped 23% w-o-w to 0.35 mnt in Week 38 from 0.45 mnt in Week 37, as activity slowed at Totoralillo (0.18 mnt) and Huasco (0.17 mnt). China remained the leading buyer at 0.18 mnt, while Egypt lifted 0.17 mnt. Market sources noted that the decline followed an operational catch-up in the previous week, with scheduling delays limiting fresh volumes. While Chile’s shipments remain small in the global context, steady offtake from key buyers helps provide a floor to exports despite weekly swings.

Peru’s exports nearly halved, plunging 43% w-o-w to 0.29 mnt in Week 38 from 0.51 mnt in Week 37. San Nicolas contributed 0.17 mnt and Matarani 0.12 mnt, with all cargoes directed exclusively to China. The sharp drop reflected operational volatility and the limited scale of Peru’s export infrastructure, which makes flows highly sensitive to port scheduling and weather disruptions. Although Chinese procurement of Peruvian magnetite concentrate was steady with 0.29 mnt, the country’s structural constraints continued to cap its export potential.

Freight market trends

Dry bulk iron ore freights showed mixed movements in Week 38, with Pacific basin routes strengthening on firm demand due to Australian and Indian cargoes, while Atlantic basin rates weakened amid muted fixture activity and limited orders.

The firmness in Pacific freights allowed Australian miners to sustain elevated shipment levels, but softer Atlantic sentiment weighed on Brazilian and South African exports, limiting upside despite improving port activity. Overall, divergent freight dynamics reinforced regional imbalances in iron ore trade flows.

Outlook

Global iron ore exports are expected to stay range-bound in the near term. Australian shipments should remain steady on firm Pacific freight, while Brazil’s recovery depends on Atlantic fixture activity. South Africa may face constraints from rail and port bottlenecks, and India’s volumes are likely to normalise post-monsoon.

Canada and Peru could see continued volatility, whereas Chilean shipments remain small but stable. Overall, mixed regional dynamics and freight trends are expected to keep Pacific routes relatively firm and Atlantic routes under pressure.

Leave a Reply