- Muted demand keeps Indian scrap buyers cautious

- Festive season may see revival of aluminium scrap demand

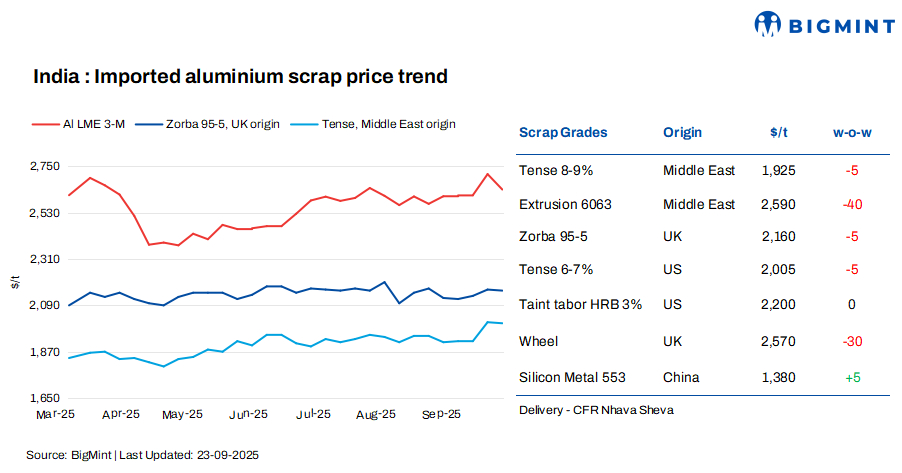

India’s imported aluminium scrap prices saw a negative trend w-o-w, following a downtrend in the London Metal Exchange (LME) prices. BigMint assessed US-origin Tense scrap at $2,005/t, down by $5/t w-o-w, while US Taint Tabor HRB (2-3%) held steady at $2,200/t.

Prices for UK-origin Zorba 95/5 and Middle East-origin Tense scrap both edged lower by $5/t. Meanwhile, Extrusion 6063 slipped $40/t w-o-w, and UK-origin wheel dropped $30/t.

LME prices decline w-o-w amid inventory inflows

At the time of reporting, LME aluminium prices stood at $2,664/t, down by around $50/t as compared to $2,614/t last week.

Meanwhile, aluminium inventories at registered warehouses posted a notable gain of 28,625 t to 485,275 t from 513,900t in the previous week.

Market insights

Indian aluminium scrap buyers stayed largely inactive this week, adopting a cautious stance amid weak market sentiment. With previously booked shipments still arriving and domestic prices under pressure, most buyers refrained from placing fresh orders. Trading was confined to small, need-based deals, as uncertainty over price trends and demand outlook prevailed.

The slowdown was further amplified by the Shradh period, during which industrial activity typically softens due to cultural observances. Locally, excess material availability and sluggish demand kept sales minimal. Many participants expect a downward correction ahead, especially with the rupee weakening against the USD, raising import costs.

Despite muted demand for aluminium semis, the auto sector offered a glimmer of hope. On the first day of Navratri and GST 2.0 rollout, Maruti Suzuki delivered nearly 30,000 units and Hyundai 11,000, a 5-6 times jump over daily averages. The festive boost, coupled with lower GST rates, has lifted industry growth forecasts to 5-7% for the fiscal year, from the earlier 1-4%. This recovery in passenger vehicle sales is expected to support aluminium alloy demand, indirectly aiding scrap demand in the coming weeks.

Domestic Tense scrap prices slipped by INR 2,000/t w-o-w to INR 194,000/t ex-Delhi, while ex-Chennai prices fell INR 1,500/t to INR 196,500/t as local demand remained subdued. With few offers in the market and buyers hesitant, near-term recovery hinges on festive-led demand and downstream sector support. Wire rod and cable plants are also preparing for BIS inspections, adding to the cautious approach in buying.

India’s aluminium ADC12 alloy ingot prices saw a slight m-o-m decline in October 2025, across both northern and southern regions, according to BigMint’s benchmark assessments.

A major Indian automaker has slightly reduced its ADC12 settlement price by INR 700/t m-o-m to INR 228,900/t for October. The marginal dip is attributed to easing raw material costs and anticipated improvement in ADC12 import availability.

Silicon price trends

According to BigMint’s assessment, silicon 553 prices from China gained by $5/t w-o-w to $1,380/t CFR Mundra.

Outlook

Prices are likely to remain range-bound in the near term. However, sentiment in the trade market is cautiously optimistic. With the festive season approaching — particularly Dussehra and Diwali — many expect buying activity to gain momentum in October, injecting renewed energy into the market.

Leave a Reply