- Global supply tightens due to Guinea Alumina license loss

- LME aluminium stocks decline, showing constrained availability

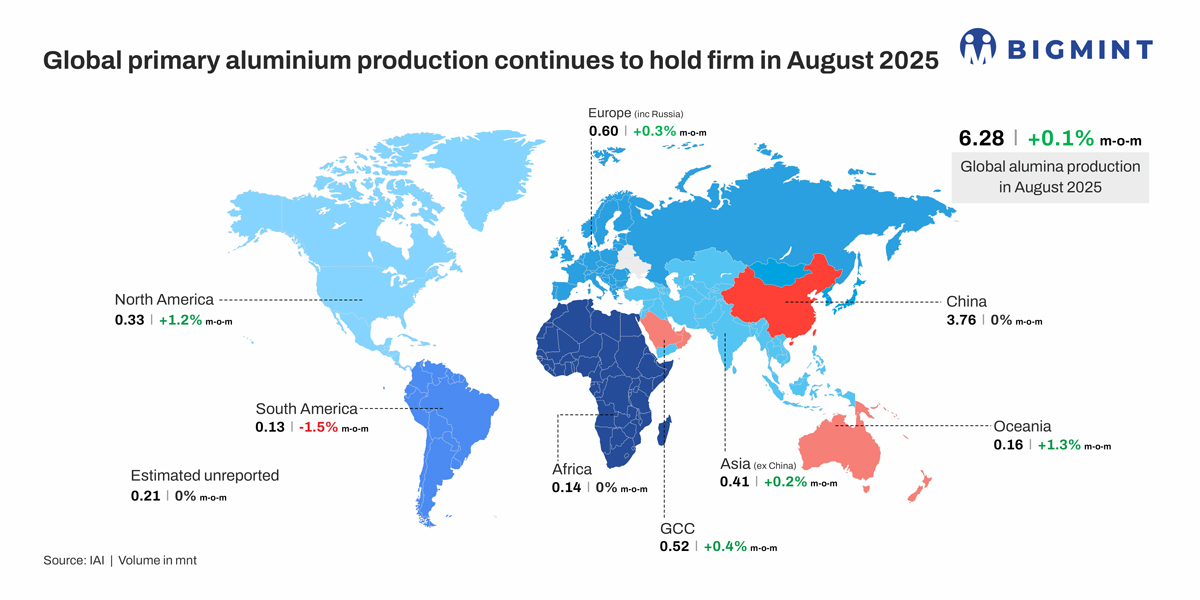

Global primary aluminium production in August 2025 stood at 6.28 million tonnes (mnt), slightly up from 6.27 mnt in July, marking a marginal 0.1% month-on-month (m-o-m) rise and 0.88% year-on-year (y-o-y) growth. The data indicates broadly stable global output across regions, with minor adjustments reflecting ongoing production balance. Meanwhile, global aluminium output in 8MCY’25 reached 49.037 mnt, up from 48.399 mnt in 8MCY’24, marking a 1.32% y-o-y increase.

Country-wise breakdown

China remained the largest producer at 3.76 mnt, largely stable m-o-m, continuing to account for more than half of global supply. Africa also held steady at 0.14 mnt. South America recorded a slight decline of 1.5% m-o-m to 0.13 mnt, while North America increased to 0.33 mnt, up 1.2% m-o-m. Asia (excluding China) edged up 0.2% to 0.41 mnt, Europe (including Russia) rose 0.3% to 0.60 mnt, Oceania climbed 1.3% to 0.16 mnt, and GCC output expanded 0.4% to 0.52 mnt. Estimated unreported production remained steady at 0.21 mnt.

Overall, the August data reflects a largely rangebound global aluminium production, with minor gains in North America, Oceania, and GCC offsetting small declines in South America.

China’s production limits and global supply tightening

China’s domestic aluminium production in August rose modestly, while exports of unwrought aluminium and semi-finished products jumped to 542,000 t in July from 489,000 t in June. Imports also increased by 12.9% y-o-y to 320,000 t, with total imports in the first eight months of 2025 reaching 2.65 mnt, up 2.7% from last year. These numbers reflect China’s continued role as the dominant driver of global aluminium supply and demand.

At the same time, global supply is under pressure. Guinea Alumina lost all mining licenses, potentially disrupting ore supply to Emirates Global Aluminium, while LME aluminium inventories fell nearly 100,000 t in early September, highlighting tightening availability. Japan, in contrast, saw a 6.3% m-o-m rise in aluminium stocks, but Q4 premiums fell to $98-$103/t, signaling weak regional demand and uneven supply conditions.

In the meantime, aluminium producers in the southwestern part of Yunnan province have been keeping their output firm, due to plentiful hydropower resources available in the area.

Historically, the aluminium market has been defined by surplus, supported by Chinese production growth and large LME inventories. However, China is now approaching its government-mandated production cap of 45 mnt, while sanctions on Russian aluminium and shifts in trade flows have further reduced exchange stocks to just above 700,000 t — down from over 3 mnt four years ago. These factors together explain the current tightening of global supply and broadly stable, yet constrained output observed in August.

Outlook

Global aluminium supply is expected to remain tight in the coming months amid constrained Chinese output, Guinea’s bauxite disruptions, and falling LME inventories. While global production remains rangebound, China nearing its 45 mnt cap and declining exchange stocks point to a structurally tighter market. Prices may stay firm or edge higher, supported by supply-side risks and steady demand.

Leave a Reply