- Buyer pushback drags silico manganese lower

- Weekly imported manganese ore cargo arrivals increase

Imported manganese ore prices remained largely stable across grades amid an uncertain market outlook. However, South African ore inched up on limited portside availability and a few bulk bookings at higher rates for Mn 37% grade, lending some support to prices. On the other hand, manganese alloys prices edged lower, with the gains in ore having limited impact due to subdued demand from the alloy steel sector.

- Australian high-grade ore (46% Mn): Prices remained unchanged at $4.72/dmtu w-o-w.

- Gabonese high-grade ore (44% Mn): Stable at $4.41/dmtu w-o-w.

- South African lumps (37% Mn): Increased by $0.04/dmtu w-o-w to $4.20/dmtu.

Manganese alloys market softens: Indian manganese alloys prices showed mixed trends this week. Silico manganese (60-14) slipped by INR 200/t ($2/t) w-o-w to INR 69,000–69,200/t ($783–786/t) across Durgapur, Raipur, and Vizag, as buyers resisted elevated offers amid stable demand and sufficient supply. Export prices of 65-16 grade also eased by $2/t w-o-w to $910/t FOB Vizag/Haldia.

In contrast, high-carbon ferro manganese (HC 70%) prices held steady with a marginal uptick of INR 100/t ($1/t) w-o-w at INR 70,400–70,500/t ($799–800/t) in Durgapur and Raipur. Export prices of HC 75% grade also edged up slightly by $1/t w-o-w to $886/t FOB Vizag/Haldia, reflecting largely stable demand and limited supply fluctuations.

Imported manganese ore prices are likely to remain stable in the near term, as the market outlook appears uncertain. Limited demand from the alloy sector and cautious buying amid price fluctuations are expected to keep ore prices range-bound, unless supply disruptions or sudden demand shifts occur.

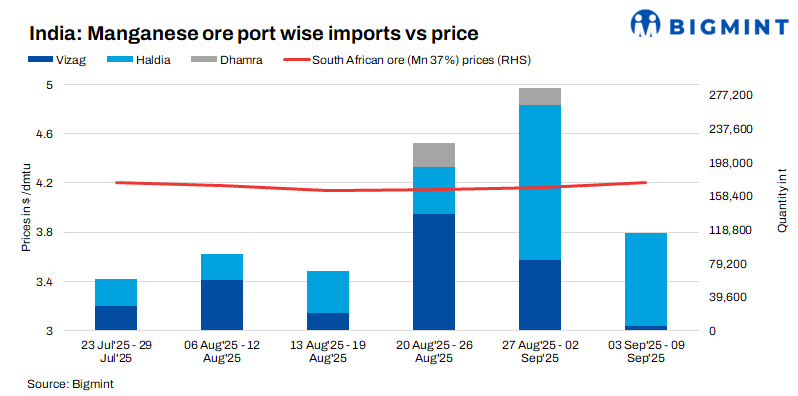

Imported cargo arrivals fall w-o-w: Weekly manganese ore cargo arrivals to India increased by 29% (Mn37%, Mn44%, and Mn46%) to 114,999 t over 3 -9 September against 285,683 t in the previous week.

Leave a Reply