- China bucks trend, but high inventories cap upside

- Iranian billets slip despite increase in rebar prices

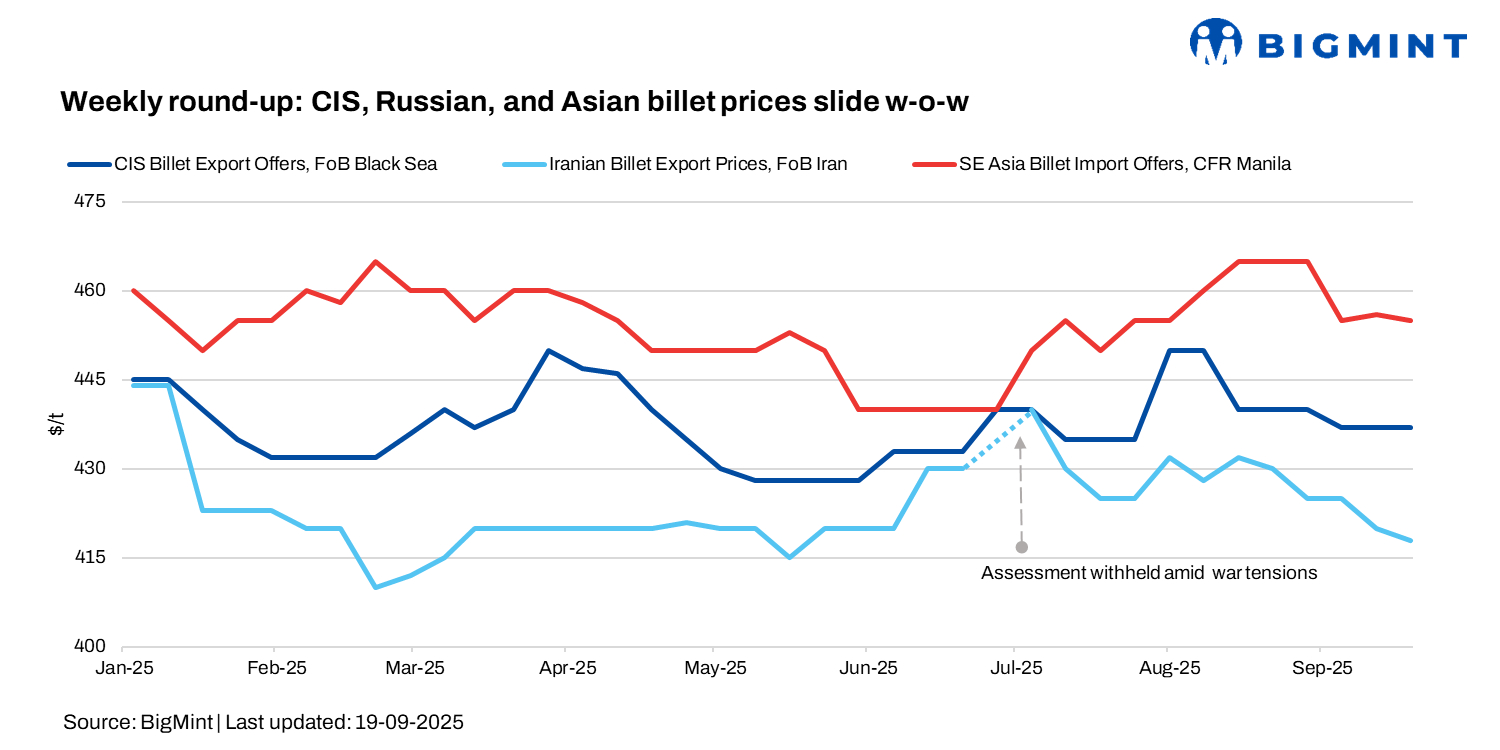

In the 38th week of 2025, global billet prices saw modest declines across most Asian markets, while the CIS region and Russia also witnessed softer offers, with weak scrap values and policy uncertainty pressuring tags. With production costs close to transaction levels, mills considered output cuts. Although Chinese domestic billet prices increased modestly, they remained competitive in the export market, with producers making aggressive efforts to capture market share amid ongoing uncertainty.

In Turkiye, deep-sea scrap softened, with US-origin HMS 80:20 at $334-338/t CFR and EU-origin material at $326-332/t CFR. Weak demand and cautious mill activity led to $5-7/t w-o-w declines. Rising freight, higher collection costs, and currency pressures kept the market largely stagnant.

Market highlights

Iran: Iran’s steel market showed mixed trends this week. Rebar rose by 5,000 rial/kg w-o-w to 380,000 rial/kg from 375,000 rial/kg by 17 September, supported by steady demand. Billets, however, softened by 3,500 rial/kg to 340,500 rial/kg from 344,000 rial/kg due to weak buying amid holidays and slow domestic activity.

Overall sentiment remained cautious, affected by political developments, exchange rate fluctuations, and potential electricity supply constraints. While rebar demand was stable, billets face pressure unless consumption picks up in the coming week. Export reference prices were largely unchanged, with billet at $420/t FOB and slabs at $410/t FOB.

In Iran, finished steel consumption fell 5% y-o-y to 7.9 million tonnes (mnt), with flats down 16% but longs up 11%, driven by rebar demand. Semis usage slipped 3%, while billet, bloom, and slab consumption also declined. Raw material consumption was mixed, with metallised products up 1%, pellets down 4%, and concentrate slightly higher.

CIS, Black Sea: Billet exporters in the CIS region struggled to maintain prices last week, with Russian offers for November shipment dropping to $440-445/t FOB from $445-450/t due to weak demand, a falling rouble, declining scrap prices, and policy changes in Egypt and Turkiye. Turkish buyers continued to seek lower prices at $450-455/t CFR, as stricter inward processing rules may limit imports. In Egypt, Russian billet activity stalled, with Chinese semis offered at $480-485/t CFR, though safeguard duties raised costs.

In Turkiye, domestic billets from major steel hubs were largely unchanged at around $500-510/t exw, but limited demand constrained semis sales. Imported CIS billets remained at $455-460/t CFR, while Chinese and Malaysian semis were offered at $470s/t and $480-490/t CFR, respectively.

China: Billet prices in Tangshan rose RMB 20/t ($6/t) w-o-w to RMB 3,050/t ($427/t), while SHFE January 2026 rebar contracts ended the week at RMB 3,172/t ($446/t), up RMB 20/t ($6/t) w-o-w but down RMB 21/t ($3/t) from mid-week highs.

Early week, gains were driven by policy support expectations, firm iron ore and coke prices, and domestic rebar demand exceeding 100,000 t/day. Mid-week, prices stabilised at around RMB 3,060-3,040/t ($430-428/t) due to high inventories and soft HRC and plate demand, while the 0.25% Fed cut triggered mild reactions. Towards the weekend, rising raw material costs and strong BF margins lifted billets slightly to RMB 3,050/t ($427/t). Export demand remained firm but was constrained by logistical issues.

The market was balanced but cautious, with limited upside amid elevated inventories.

Leave a Reply