- Sellers focus on clearing stocks before GST reforms take effect

- Buyers resist bulk bookings, preferring a wait-and-watch stance

The coal market this week remained subdued, with participants largely holding back ahead of the GST and cess transition. Sellers attempted to liquidate old stocks, while buyers restricted activity to urgent needs. Uncertainty over post-22 September pricing kept sentiment cautious, leaving both portside and domestic trade quiet. Overall, the market tone is steady but watchful, awaiting clear price signals.

Indonesian portside coal market steady as buyers await GST clarity

The Indian portside market for Indonesian thermal coal stayed stable this week as participants delayed purchases ahead of the 22 September GST reform. Prices held at INR 6,950/t for 5000 GAR in Kandla and INR 6,850/t in Vizag, while 4200 GAR and 3400 GAR grades also remained unchanged. Trading activity was muted, with buyers expecting cheaper post-cess cargoes and some sellers cutting offers slightly to clear stocks. Freight rates on the Indonesia-India route softened amid vessel oversupply, while global Indonesian coal tags posted modest gains supported by selective regional demand recovery. Outlook remains cautious until post-GST clarity emerges.

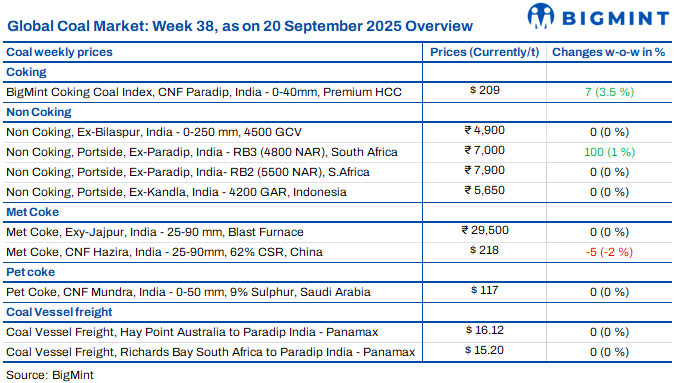

South African coal market stays cautious ahead of GST shift

South African coal prices at Vizag and Gangavaram remained mostly unchanged this week, with RB2 steady at INR 7,750-7,900/t and RB3 around INR 6,800/t. Activity stayed muted as both buyers and sellers waited for clarity post-22 September cess removal. No major trades surfaced, though some forward RB2 offers were heard near INR 8,200-8,400/t. Export offers held stable at $71/t for RB2 and $60/t for RB3, reflecting weak Indian demand. In sponge iron, prices rallied INR 100-600/t, led by Ramgarh, though cautious sentiment capped large-scale buying. Prices are expected to remain range-bound until the GST transition clears.

Domestic coal prices steady w-o-w; sentiment hinges on GST clarity

Domestic coal prices stayed flat this week, with 5,000 GCV at INR 5,750/t ex-Bilaspur and 4,500 GCV at INR 4,900/t. Buyers continued to adopt a cautious stance ahead of 22 September, when cess removal is expected to ease FSA-linked prices. For now, offers remain unchanged, with market direction likely to emerge only after GST adjustments take effect.

India’s coking coal index climbs as mills book fresh cargoes

BigMint’s premium hard coking coal (PHCC) index rose $7/t w-o-w to $209/t CNF Paradip on 20 September, supported by fresh bookings. An Indian mill secured a 25,000-30,000 t Australian PHCC cargo at $210–215/t CFR Vizag, while two more mills in east and south concluded deals.

Indian met coke market steady as weak pig iron curbs demand

The Indian met coke market stayed unchanged this week, with BF-grade assessed at INR 29,500/t ex-Jajpur and INR 30,000/t ex-Gandhidham, while foundry-grade held INR 35,600/t ex-Rajkot. Trading stayed limited around 20,000 t, as buyers preferred local supply. Pig iron weakness pressured demand, with prices in Durgapur slipping INR 400/t to INR 32,300/t. Imports were weighed down by muted buying, though Chinese restocking ahead of holidays lent regional cost support.

Imported pet coke prices steady w-o-w; demand response stays weak

Imported pet coke offers in India remained unchanged this week. While some trades reflected a marginal $1-2/t easing as sellers adjusted to weaker coal prices and resistance from buyers, BigMint’s assessment held steady. US-origin offers stayed at $118-120/t CFR, while Saudi-origin hovered at $117-119/t CFR. Market sentiment stayed muted, with limited acceptance of higher levels from end users.

Dry bulk coal freights show mixed trends

Dry bulk coal freights displayed a mixed trend this week as muted cargo demand and cautious sentiment weighed on activity. Australia-India Panamax rates held stable at $16.12/dmt, supported by SAIL fixtures, while South Africa-India freights also stayed unchanged at $15.20/dmt despite limited inquiries. In contrast, Indonesia-India Supramax freights declined by $0.25 w-o-w to $15.71/dmt, pressured by vessel oversupply and weaker export demand. Overall, charterers continued to resist elevated offers while shipowners held firm on rates. With freight derivatives inching up but spot fixtures subdued, the near-term outlook remains soft to range-bound.

Leave a Reply