- Market stays muted amid cautious sentiment ahead of 22 Sep

- Traders and buyers hold back, awaiting post-GST price direction

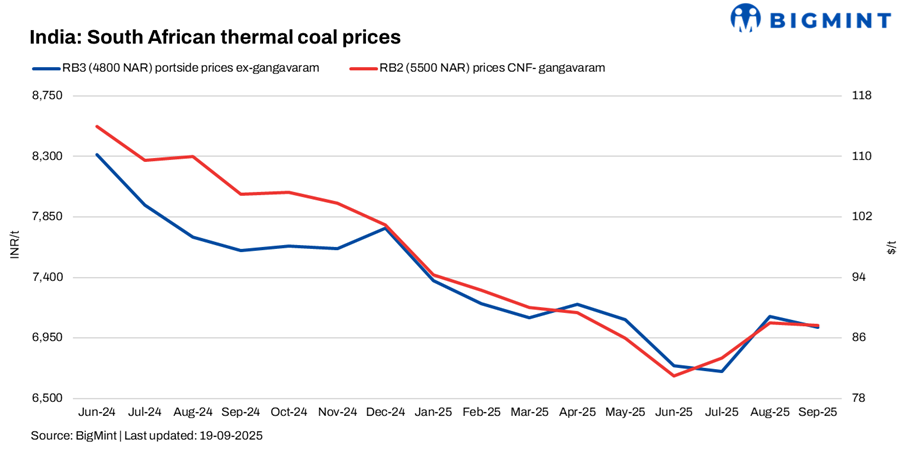

South African portside coal prices in India showed limited movement this week. At Vizag, RB2 held at INR 7,750/t w-o-w, while RB3 was steady at INR 6,800/t. At Gangavaram, RB2 stayed flat at INR 7,900/t, while RB3 edged down by INR 100/t to INR 6,800/t. Despite stability, deals remained muted as both sellers and buyers adopted a wait-and-watch approach before the 22 September cess removal deadline.

No active trades were reported, though a trading house was heard offering RB2 (5,500 NAR) at INR 8,200/t for post-deadline deliveries, while another trader quoted INR 8,400/t citing better quality. Current ex-Mangalore RB2 offers with cess stand at INR 8,250/t. South African RB1 was last indicated at around INR 9,600/t, with delivery orders likely only after the deadline.

Export offers from Richards Bay stayed unchanged, with RB2 assessed at $71/t FOB and RB3 at $60/t FOB, reflecting muted Indian buying.

Domestic coal prices held steady, with 5,000 GCV at INR 5,750/t ex-Bilaspur and 4,500 GCV at INR 4,900/t. FSA-linked prices are expected to ease after cess removal, but for now, stability continues.

In the sponge iron market, BigMint’s C-DRI index (ex-Rourkela) rose INR 250/t w-o-w to INR 26,450/t. Prices across India posted sharp gains of INR 100–600/t, with Ramgarh recording the steepest rise of INR 600/t. The rally was driven by stronger cues from semi-finished and finished steel, alongside improved trade activity. However, buyers stayed cautious, limiting participation as uncertainty persisted on the sustainability of the uptrend.

Outlook

Prices are expected to stay range-bound until clarity emerges post-22 September.

Leave a Reply