- Cultivation acreage rises 2% y-o-y

- Excess rains may play spoilsport

What lies in store for India’s rice sector for the crop season 2025-26? Adequate production and procurement trends augur well from the country’s food security perspective. India is a major rice exporter globally, and hence large harvests will have a cascading impact on domestic food security, inflation, prices, and global rice supplies.

Rice is one of India’s most important crops. The Kharif (monsoon) season, which spans roughly from June through September, sees most of India’s paddy (rice) getting sown, with harvesting setting in, in many regions, beginning from mid-September. The season’s success heavily depends on the monsoon — its timing, strength, distribution, and intensity. Government policies (procurement, minimum support prices, export rules), and global demand also play big roles.

Production set to rise on acreage increase

The latest agricultural data available with BigMint reveals a promising outlook for India’s rice production, with a significant increase in planted area for the 2025-26 season. According to a recent report, rice acreage has climbed to 438.51 lakh hectares, marking a notable expansion from the previous year’s 430.06 lakh hectares. This growth represents a y-o-y increase of 8.45 lakh hectares — a 2% rise over the 2024-25 season. Furthermore, the figures indicate that the current rice acreage is 9% higher than the normal 403.09 lakh hectares, signalling a sustained trend of expansion in rice cultivation.

The consistent growth in planted area is a positive sign for food security and the agricultural sector’s resilience. The government and farmers have been working on initiatives to encourage crop diversification and enhancing yield, and these figures suggest that such efforts are yielding positive results. These are initial acreage figures but, nonetheless, these lay a strong foundation for a robust harvest in the coming months, which could help stabilise food prices and ensure a healthy supply of this staple.

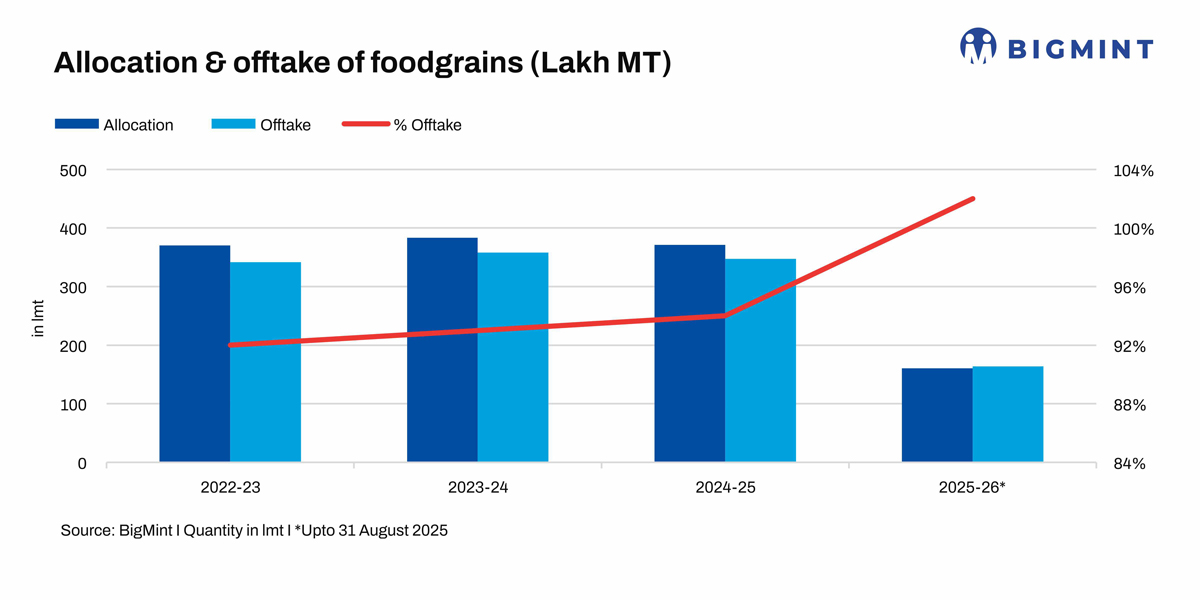

Procurement surpasses estimate

Procurement data indicates a strong and efficient purchasing process. Progressive paddy procurement has touched 912.73 lakh tonnes (LT), exceeding the initial estimate of 872.52 LT. This success in paddy procurement has translated into significant rice procurement, with 611.53 LT of rice progressively procured. Of this, 473.20 LT of custom milled rice has already been received, with a remaining 138.33 LT yet to be collected.

It may be mentioned that of the total 160.38 LT of rice allocated for the 2025-26 crop season (till August 2025), a healthy 164 LT have been procured, which is a hefty 102% of the allocation. So far, data available from 2022-23 till 2024-25 reveals procurement has remained under 95% for the full crop years. In 2022-23, procurement was at 92% (342 LT) of the 370 LT allocated. In 2023-24, it was at 93% or 358 LT of the allocated 383 LT while 2024-25 saw 347 LT or 94% being procured out of the 371 LT allocated.

The high procurement figures demonstrate that the government’s system for purchasing and storing rice grains is functioning effectively, as per a source. A strong buffer stock is essential for effectively managing food prices, providing relief during crises, and ensuring a stable supply through the Public Distribution System (PDS), which provides subsidised food to millions of underprivileged people. In essence, the data points to a well-managed and productive rice sector which augurs well for India’s food security in the current crop season.

Monsoon dampener

The only shadow casting on India’s rice segment is the excessive rainfall seen this monsoon season, which has led to flooding and crop damage in certain regions. As of early September, the country has received about 6% above-normal rainfall for the period from June 1st to August 31st.

But, India could indeed record another bumper rice crop, possibly around 150-151 million tonnes for the 2025-26 crop season against around 149 mnt seen in 2024-25.

As a result, domestic prices are likely to remain soft, especially for non-premium rice grades, unless supply chain constraints or quality issues emerge.

Leave a Reply