- Australian exports fall by 5% on reduced vessel activity

- GST reforms, higher landed costs cap Indian imports

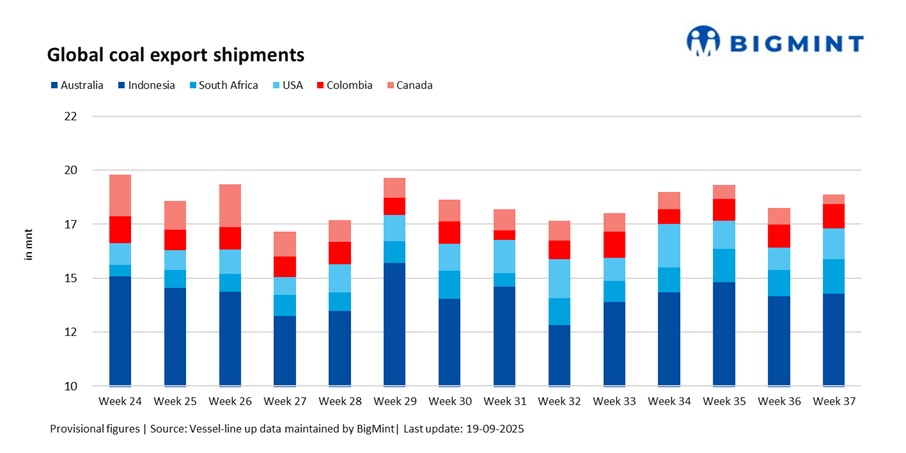

Global seaborne coal exports rose 3.3% w-o-w to 18.51 million tonnes (mnt) in Week 37 (6-12 September 2025) from 17.93 mnt in Week 36, according to BigMint’s vessel line-up data. The rebound was underpinned by higher shipments from Indonesia, South Africa, the US, and Colombia, which collectively offset declines from Australia and Canada.

The uptick reflected a combination of improved vessel availability in South Africa, steady Indonesian loadings, and opportunistic fixtures from the US and Colombia. However, muted Indian demand continued to cap momentum, as higher landed costs from freight softness and the impending GST reforms weighed on fresh import bookings.

Country-wise trends

Indonesia: Coal exports rose 7% w-o-w to 7.7 mnt in Week 37 from 7.2 mnt in Week 36, supported by a combination of stable weather conditions and steady cargo flows. Loadings were led by Taboneo (1.66 mnt), followed by Samarinda (1.07 mnt) and Bunati (0.81 mnt), while smaller ports contributed the balance. Market sources noted that improved vessel availability and consistent port activity underpinned the week’s increase, offsetting earlier monsoon-related slowdowns.

On the demand side, India (1.86 mnt) and China (1.49 mnt) remained the two largest buyers, reflecting their continued dependence on Indonesian thermal coal. The Philippines (1.10 mnt) and South Korea (0.94 mnt) also featured prominently. However, despite the broader stability, traders cautioned that softer Indian procurement amid higher landed costs limited upside potential.

Australia: Coal shipments fell 5.7% w-o-w to 6.40 mnt in Week 37 from 6.79 mnt in Week 36, extending the downward trend after a strong August. Loadings were dominated by Newcastle (3.09 mnt), followed by Gladstone (1.43 mnt) and DBCT (0.68 mnt), while other terminals handled smaller parcels. The slowdown was attributed to reduced vessel activity and longer turnaround times, which constrained port throughput during the week.

On the demand side, Japan (2.02 mnt) and China (1.07 mnt) remained the principal buyers. However, shipments to India were notably weaker, as elevated landed costs following softer freight dynamics and GST-related reforms curbed procurement. Market participants also pointed to selective buying strategies by Indian utilities, which, combined with logistical constraints, weighed on overall exports.

South Africa: Exports surged 31.9% w-o-w to 1.54 mnt from 1.16 mnt, with all shipments routed through Richards Bay Coal Terminal (RBCT) at 1.54 mnt.

Improved railings supported the rebound, though logistical fragility remains a key risk. India, with 0.82 mnt, featured among the main buyers, with opportunistic demand providing support. The market, however, remained cautious on sustainability given recurring rail bottlenecks.

US: Coal exports climbed 33.6% w-o-w to 1.36 mnt in Week 37 from 1.02 mnt in Week 36, marking a notable recovery after the prior week’s weakness. Loadings were concentrated at Norfolk (0.48 mnt), followed by Baltimore (0.36 mnt) and Mobile (0.31 mnt), with smaller volumes handled at other terminals.

India (0.31 mnt) emerged as the largest buyer of US coal, lifting smaller parcels mainly for the steel and cement sectors. Additional volumes were directed towards European markets, though uptake there remained selective amid elevated freight levels and cautious industrial demand.

Colombia: Coal exports increased 9.2% w-o-w to 1.10 mnt in Week 37 from 1.01 mnt in Week 36, continuing the steady recovery in shipments. Loadings were dominated by Puerto Nuevo (0.64 mnt) and Puerto Bolivar (0.25 mnt), supported by stable production levels. By shipper, Prodeco (0.66 mnt) and Cerrejon (0.25 mnt) remained the key contributors, underscoring their dominant role in sustaining Colombian export flows.

On the demand side, Brazil (0.23 mnt) and the Netherlands (0.18 mnt) featured as the largest buyers, while smaller parcels were absorbed by other European utilities.

Canada: Coal exports slumped 45.3% w-o-w to 0.41 mnt in Week 37 from 0.74 mnt in Week 36, marking the steepest weekly decline among major exporters. Loadings were concentrated at Vancouver (0.23 mnt) and Roberts Bank (0.09 mnt), both of which witnessed reduced activity compared with the previous week. The sharp fall reflected weaker vessel availability and ongoing supply-side challenges that curtailed shipments.

Japan (0.25 mnt) remained the primary buyer. Market sources suggested that without sustained improvements in supply chain reliability, Canadian shipments are likely to fluctuate sharply in the weeks ahead.

Freight trends: Dry bulk coal freights softened w-o-w, with muted fixture activity and higher landed costs curbing trade flows. While time charter sentiment improved slightly and easing bunker prices provided some cost relief, voyage earnings remained under pressure amid subdued Indian buying and GST-related cost escalations.

Activity on Indonesia-India and South Africa-India routes was especially sluggish, discouraging fresh bookings and tempering the export rebound.

Outlook

Global coal exports are expected to remain range-bound in the near term. Indonesian flows are likely to hold steady, while Australian volumes may stay under pressure amid softer Indian buying. South Africa’s exports hinge on consistent railings, whereas US and Canadian shipments remain volatile. With freight sentiment weak and India’s landed costs set to rise under GST reforms, traders are expected to remain cautious on fresh bookings, limiting near-term upside in seaborne trade.

Leave a Reply