- India rushes exports before possible duty on iron ore from Oct

- Chile, Peru see recovery, South African exports weak

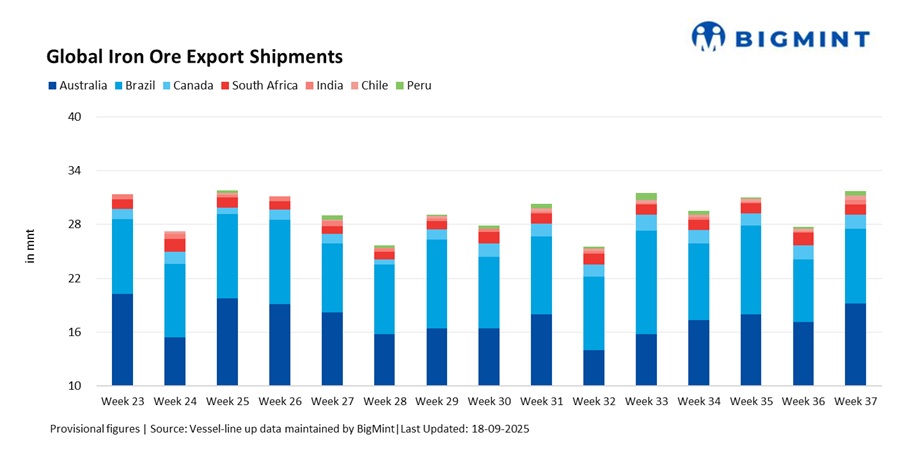

Global iron ore exports rose 14.3% w-o-w to 31.73 million tonnes (mnt) in week 37 (6-12 September) of 2025, up from 27.76 mnt in week 36. The rebound was mainly supported by higher shipments from Australia and Brazil, with India, Chile, and Peru also recording strong recoveries from recent lows.

Market participants noted that Australian exports regained momentum after a softer week 36, with miners pushing more cargoes into the Pacific basin amid firmer freight sentiment and improved vessel demand. Brazil also staged a partial recovery following a steep slump in the prior week, supported by higher activity at key ports.

At the same time, India saw a sudden surge as exporters rushed shipments amid apprehensions that a 30% export duty may be imposed on iron ore from October.

Smaller exporters such as Chile and Peru also contributed to the weekly rebound, recording sharp operational catch-ups. However, South Africa’s flows declined as rail and port constraints continued to weigh on performance, limiting the country’s ability to sustain exports despite firm Asian demand.

Country-wise exports

Australia’s iron ore exports rose 12.1% w-o-w to 19.22 mnt from 17.14 mnt in week 36, the highest weekly volume since mid-August. Loadings from Pilbara ports remained strong, with Port Hedland handling an estimated 11.86 mnt, Walcott around 4.09 mnt, and Dampier close to 2.8 mnt. Among the majors, Rio Tinto shipped 6.92 mnt, BHP 5.65 mnt, and FMG 5.38 mnt, with activity supported by firm Capesize demand in the Pacific.

China continued to dominate liftings at over 16.62 mnt despite weak steel margins, followed by Japan at 1.40 mnt and South Korea at 0.59 mnt. Market sources noted that Pacific freight strength provided additional support, allowing Australian miners to sustain elevated shipment levels even as Chinese mills tread cautiously.

Brazil’s iron ore exports rebounded 18.6% w-o-w to 8.29 mnt from 6.99 mnt in week 36, recovering from the prior week’s sharp decline. Ponta da Madeira led shipments with nearly 2.8 mnt, followed by Itaguai at 2.02 mnt and Tubarao at 1.9 mnt, while smaller ports made up the remainder.

Vale dominated flows, dispatching around 3.43 mnt, with China absorbing over 4.06 mnt of the total. The recovery was underpinned by a modest pickup in fixture activity, as improving sentiment in the Pacific basin spilled over into Atlantic markets, helping Brazilian exports regain momentum. Market sources also noted that Vale’s recently restarted Capanema mine is gradually ramping up, but immediate impact on volumes is limited.

Canada’s iron ore exports edged up 3.5% w-o-w to 1.60 mnt in week 37 from 1.55 mnt in week 36. Sept-Iles led shipments with 0.86 mnt, followed by Milne Inlet at 0.53 mnt and Port Cartier at 0.22 mnt. The uptick was aided by improved weather conditions and stable vessel availability, helping flows normalize after recent disruptions.

On the demand side, Europe remained the key destination, with The Netherlands lifting 0.27 mnt, Spain 0.20 mnt, and Germany and Bahrain at 0.17 mnt each. Canada’s high-grade concentrate continues to attract European mills seeking efficiency gains, though seasonal logistical constraints and ice-navigation risks toward year-end could cap momentum.

South Africa’s iron ore exports dropped 23.1% w-o-w to 1.10 mnt in week 37 from 1.43 mnt in week 36. Saldanha Bay handled the bulk at 0.93 mnt, with Richards Bay contributing 0.17 mnt.

China remained the top buyer at 0.34 mnt, followed by The Netherlands with 0.18 mnt. However, shipments were weighed down by logistical bottlenecks and relatively higher freight costs. Meanwhile, buyers stayed cautious, and bid-offer gaps limited fixture activity despite steady underlying demand.

India’s iron ore exports surged nearly fivefold to 0.55 mnt from 0.12 mnt in week 36, marking the highest weekly tally since early monsoon season. Shipments were primarily handled through Paradip (0.25 mnt) and Dhamra ports (0.17 mnt).

Chinese traders were the largest buyers at 0.17 mnt, securing most of the available parcels, while smaller volumes went to Southeast Asia. Despite heavy rains still affecting mining operations in Odisha and Chhattisgarh, the urgency to clear inventories for export provided a temporary boost. Market sources expect this surge to be short-lived, with volumes likely to normalize once the duty is implemented.

Chile’s iron ore exports surged 60% w-o-w to 0.45 mnt in week 37 from 0.28 mnt in week 36. Totoralillo and Huasco contributed 0.17 mnt each, while Guayacan added 0.08 mnt.

China and Bahrain emerged as the main buyers at 0.17 mnt each, continuing to absorb Chile’s niche high-grade magnetite supply. The rebound was largely operational, as improved port scheduling allowed larger parcels to be cleared after the prior week’s slowdown. Though Chile’s volumes remain small in the global context, steady Chinese offtake provides a reliable floor for exports, cushioning weekly swings.

Peru’s iron ore exports more than doubled, climbing 109% w-o-w to 0.51 mnt in week 37 from 0.25 mnt in week 36. San Nicolas dominated shipments, accounting for nearly the entire volume, which was directed almost exclusively to China.

The sharp rebound reflected both operational recovery and opportunistic scheduling. However, market participants noted that Peru’s relatively small-scale operations leave exports prone to volatility. Structural challenges such as infrastructure constraints and reliance on a limited number of ports continue to cap the country’s growth potential.

Dry bulk iron ore freights exhibit mixed trends

Dry bulk iron ore freights showed mixed trends in week 37. Pacific basin routes strengthened, supported by active demand on the Australia-China and India-China corridors, which encouraged miners to raise shipments. Rising charterer interest, firmer period fixtures, and easing bunker costs all underpinned sentiment.

In contrast, Atlantic basin freights from Brazil and South Africa to China saw marginal declines, with thin fixture activity and higher tonnage availability weighing on sentiment. The divergence meant that freight supported Australia’s elevated volumes but offered little relief for South African or Brazilian shipments, reinforcing regional imbalances.

Outlook

Global iron ore exports are expected to remain steady to slightly higher in the near term, supported by Australia’s consistent flows and a gradual recovery in Brazil. India’s shipments could remain firm in the short run as exporters rush cargoes ahead of the expected duty but may drop sharply once it is imposed.

South Africa’s rail and port challenges are likely to continue capping exports, while weather-related risks in Canada and Peru may add volatility. Freight sentiment is expected to stay more supportive in the Pacific than the Atlantic, keeping global trade flows regionally skewed.

Leave a Reply