By Rhishita Das

- Domestic demand to grow at 7% CAGR, mirroring GDP rate

- CRGO supply hinges on imports, with domestic production falling short

- CRNGO supply adequate, but Chinese dumping risks remain

Morning Brief: India’s growing electrical steel segment has generated immense buzz, given the accelerating transformation of the power sector, both to increase capacity and to raise renewable energy adoption. While capacity additions in the electrical sector are ongoing to meet rising demand, market participants cite that India still suffers from heightened dependence on imports and an acute supply shortage.

Overview

A type of specialty steel, electrical steel is so called because of its suitability for electromagnetic applications. Silicon is the primary alloying element, as against carbon, which is kept at a minimum to avoid brittleness and energy loss. Given that the percentage of silicon in the alloy is comparatively high, traditionally around 3% but reaching up to 6.5%, electrical steel is also known as silicon steel.

The addition of silicon increases the alloy’s electrical resistivity and enables higher permeability of electrical currents, resulting in a reduction in core losses and improved energy efficiency.

Ferro silicon is the key feedstock for electrical steel.

Grade-wise classification & applications

Primarily, there are two grades of electrical steel: cold-rolled grain oriented (abbreviated as CRGO or GOES) and cold-rolled non-grain-oriented (CRNGO, CRNO, or NOES).

The key difference between the two is that CRGO is processed to have its grains aligned in a specific direction, while the grain orientation of CRNGO is more randomised, leading to uniform magnetisation in all directions. CRGO is also more expensive to produce and is limited in supply. It is ideal for use in static applications such as transformer cores in the power and distribution segment and inductors. Meanwhile, CRNGO is considered to be more suitable for rotating equipment, including motors and generators.

Demand-supply scenario

According to a source from a leading mill, global demand for CRGO stands at 3.2-3.5 mnt, while production is approximately 4 mnt. Production capacity is estimated to be within 5-7 mnt, with the lion’s share in the hands of only 10-12 companies, who fiercely guard their technology. India sources its CRGO mostly through imports, with self-reliance still a remote possibility. China is the largest consumer of this grade, followed by the US and India.

India’s CRGO demand is estimated at around 300,000 t per annum (tpa), but production capacity is around 50,000 t. In a 2024 report, GTRI pointed to domestic production meeting only 10-12% of demand. However, another senior executive from a major electrical steel producer suggested that Indian capacities are able to meet a higher 33-35% share of consumption.

As for CRNGO, global production capacity is pegged at 8-10 mnt, with both output and demand coming to around 5-6 mnt. Indian production capacity is considered to be at 750,000 t, with annual demand at 700,000 t.

India seems to have adequate CRNGO production, while domestic CRGO supply fails to meet demand. Additionally, the 0.23-mm and 0.27-mm sizes of CRGO are largely used in transformers. For CRNGO, the 0.35-mm and 0.50-mm sizes fetch the most demand.

Sectoral demand perspective

The energy sector has been the primary driver of the expanding electrical steel landscape in India. Infrastructure growth, rising electrification, increased renewable energy use, strong consumer demand, the emergence of artificial intelligence and need for data centres, shift to automation, EVs, and green steel adoption are all leading to robust investments in India’s power sector.

However, again, imports of finished products threaten India’s electrical steel demand. For example, in the transformer sector, cheap motor imports persist, while the home appliances segment is also reliant on foreign product inflows.

The same dynamics are reflected in the automotive industry, which is expected to be a major consumer of electrical steel in the days ahead. However, in India, electrical steel use in the automotive industry is still in its early stages, due to large-scale imports of finished components and equipment — 40 crore motors were imported last year.

As such, MSMEs have an excellent growth opportunity to capitalise on, with these businesses being tailor-made for MSMEs, asserted the above source.

Capacity expansions

JSW Steel, the leading electrical steel maker in India, has been steadily increasing production in collaboration with Japanese partner JFE Steel Corporation. In August, they announced an INR 5,845 crore expansion of their CRGO manufacturing capacity to 350,000 t.

The company had earlier also acquired thyssenkrupp Electrical Steel India, previously the only large-scale CRGO manufacturer in the country.

Additionally, SAIL and John Cockerill India have joined hands to set up an INR 6,000 crore plant for CRGO and CRNGO, with production of 1.5 mnt per annum.

The Indian government has also improved ease of doing business for potential CRGO producers as per the second round of the PLI scheme for speciality steels. Stating that the technology to make CRGO is unavailable with Indian steelmakers, the Ministry of Steel has reduced the investment and capacity creation thresholds to INR 3,000 crore and 50,000 t, respectively, to incentivise production growth.

Domestic consumption growth

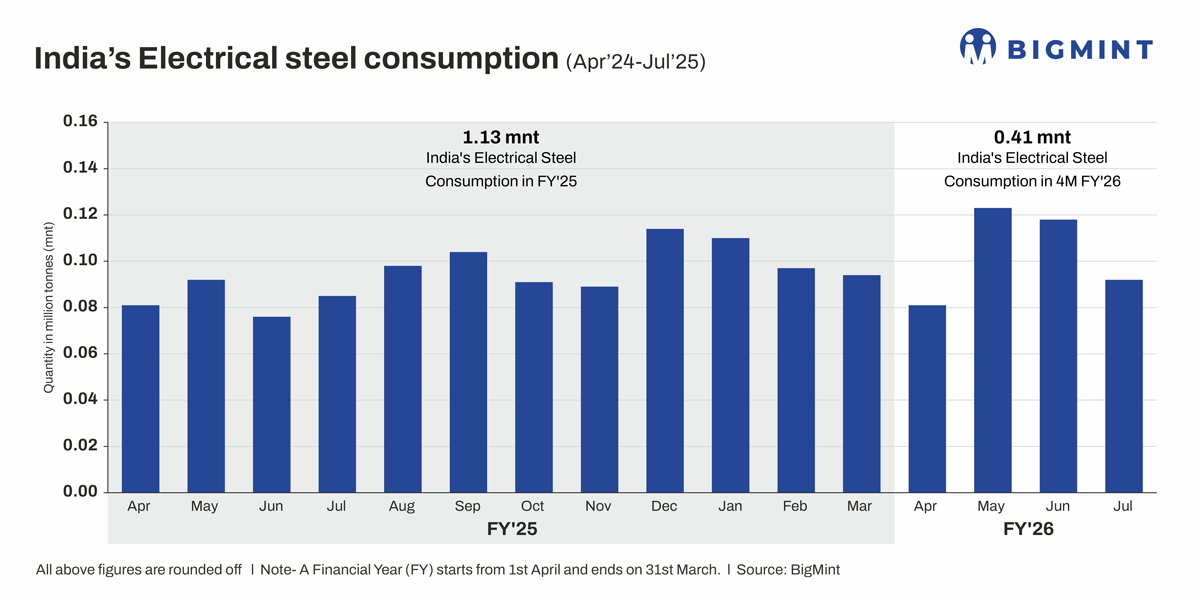

India’s electrical steel consumption has been steadily increasing in recent years, with FY’25 volumes at 1.13 mnt, up by a robust 24% y-o-y. Even FY’24 recorded a 21% y-o-y increase at 0.91 mnt. Meanwhile, consumption in the first four months of this fiscal year (4MFY’26) has reached 0.41 mnt already, showing a 24% rise y-o-y.

Import scenario, dumping threat

In the past five years, annual electrical steel import volumes have consistently remained above 1 mnt, with strong y-o-y growth in most years. In FY’25, imports jumped by 40% y-o-y to 1.97 mnt, though arrivals had fallen by 13% y-o-y in the preceding year. FY’22 and FY’23 witnessed y-o-y spikes of 10% and 19%, respectively.

Imports are sourced primarily from China, South Korea, Japan, Taiwan, and Russia. On average, South Korea has been the leading supplier to India, consistently shipping over 0.55 mnt every year. However, last fiscal year, China superseded South Korea (0.57 mnt) by exporting over 0.67 mnt to India, a rise of 123% y-o-y. This has given rise to concerns of dumping.

Mounting imports have caused irreparable damage to the domestic industry, a senior executive observed, while refuting claims of supply shortage. With reference to fully processed CRNO, he stated, “From a consumption point of view, India has got today nearly 50,000 t per year of extra capacity.” Due to predatory pricing of imports from China, Japan, and Vietnam, some of this capacity is idle.

The CRGO sector has also been suffering equally. Indian production manages to meet only around 35% of demand, but that is because domestic output has few takers amid surplus supply of cheap overseas material. Indian producers’ financial losses have swelled, even keeping capacity expansions in check.

In October 2024, India initiated an anti-dumping investigation into Chinese CRNO imports based on complaints from domestic subsidiaries of South Korean and Taiwanese producers, including POSCO Maharashtra Steel and CSCI China Steel Corporation India. However, both CRGO and CRNGO have been kept outside the purview of the three-year safeguard duty on flat steel imports.

Demand outlook to 2030

India’s electrical steel demand is only going to rise as energy transition and power generation accelerate. One source suggests 7% growth rate, aligning with GDP levels, while GTRI projects a 10-12% increase annually for CRGO in particular. An expanding power sector, the government’s push to integrate 500 GW of renewable energy by 2030, and the Bureau of Energy Efficiency’s mandate for a star-label upgrade for transformers, effective January 2025, are expected to boost demand for this specialty steel.

The other major contributor is EVs and green energy. EVs use high-performance CRGNO in motors, while renewable energy systems (like wind turbines and solar inverters) use both variants. The auto sector would, however, benefit from the development of high-grade CRNGO with lower energy loss and better magnetic properties.

The government’s tightening of energy efficiency standards for appliances, motors, and transformers is also expected to boost demand, as well as setting up of smart grids and digital transformers. This may push manufacturers to shift to premium-grade electrical steel with ultra-low core loss, despite higher costs incurred.

However, risks remain from elevated imports and the dominance of a few suppliers in the world.

Leave a Reply