- Latest reduction follows 6 months of price stability

- China’s Baosteel keeps Oct’25 HRC prices unchanged

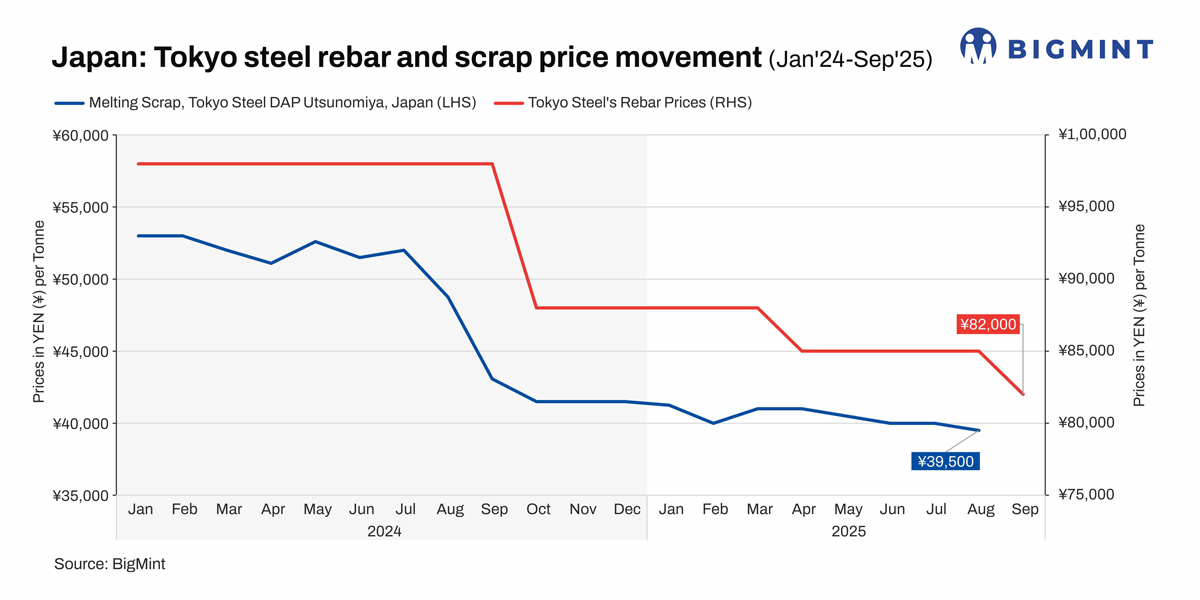

Tokyo Steel, Japan’s leading electric arc furnace (EAF) steel producer, has cut hot-rolled coil (1.722 mm) prices by JPY 3,000/tonne (t) ($20/t) for October 2025 sales. The company reduced prices after keeping them stable for six months in a row. Moreover, rebar prices were reduced by JPY 3,000/t ($20/t) and H-beam tags were slashed by JPY 12,000/t ($82/t) for October 2025 sales.

Revised prices are as follows:

HRCs (1.7-22 mm): JPY 86,000/t ($585/t)

Rebars (D13~25): JPY 82,000/t ($558/t)

H-beams (100-300 mm): JPY 100,000/t ($680/t)

(Note: Conversion rate as of 16 October 2025 – JPY 1 = $0.006802025; $1 = JPY 147.015)

Factors influencing Tokyo Steel’s pricing

1. Domestic market remains weak: Japan’s steel market is currently experiencing sluggish demand due to weak market conditions, which is reflected in the lacklustre nationwide shipments. The construction sector presents a mixed picture; while some electrical firms are busy, many prime contractors are delaying new projects. However, there is some optimism with rising inquiries for year-end projects.

Meanwhile, the manufacturing sector remains cautious, hindered by uncertainty regarding US negotiations and labour shortages, which have also impacted the outlook for imported steel. Despite these challenges and the pressure of high production costs on profitability, there are some positive signs, such as an increase in machine tool orders and growing investments in digital transformation, which could help improve the demand for steel in the future.

2. Key global mills’ pricing trends: The world’s top steel manufacturer, Baosteel, rolled over HRC prices for October 2025 sales after having raised them by RMB 200/t ($28/t) m-o-m for September sales.

However, Vietnamese steel giant Formosa Ha Tinh (FHS) raised its hot-rolled coil (HRC) prices by approximately $10/t m-o-m for October 2025 sales. Post revision, prices of HRCs (SAE1006, skin-passed) ranged within $519-528/t CIF Ho Chi Minh City (HCMC), depending on the quantity booked, as compared to $507-517/t CIF HCMC a month ago.

3. H2 export offers remain range-bound in Sep: Japan’s September Kanto scrap export tender closed with a marginal rise of JPY 82/t ($1/t), as 15,000 t of H2 were booked by a Chattogram mill at JPY 41,970/t ($285/t) FAS. The deal translates to around $295/t FOB Japan and $345-350/t CFR Chattogram, factoring in freight. BigMint’s weekly H2 assessment stood at JPY 41,600/t ($282/t) FOB Tokyo Bay, slipping JPY 100/t ($1/t) w-o-w in a range-bound market despite the tender outcome.

Outlook:

In the short term, Japan’s domestic steel market is expected to fluctuate in a narrow band. Some industry participants are optimistic about a pick-up in demand from the construction and the automobile industry, being the major consumers of steel products. Furthermore, the US tariffs on automobiles have now been settled, which hints towards improvement in the supply-demand balance as demand increases toward the second half of the year. On broader terms, market sentiment remains cautious around the ongoing global tariff talks and the pressure exerted by persistent steel imports from other countries.

Leave a Reply