- SE Asian billet market weak; Philippine bids steady at $450/t

- Turkiye, Russia cut rates; Egypt imposes 16.2% safeguard duty

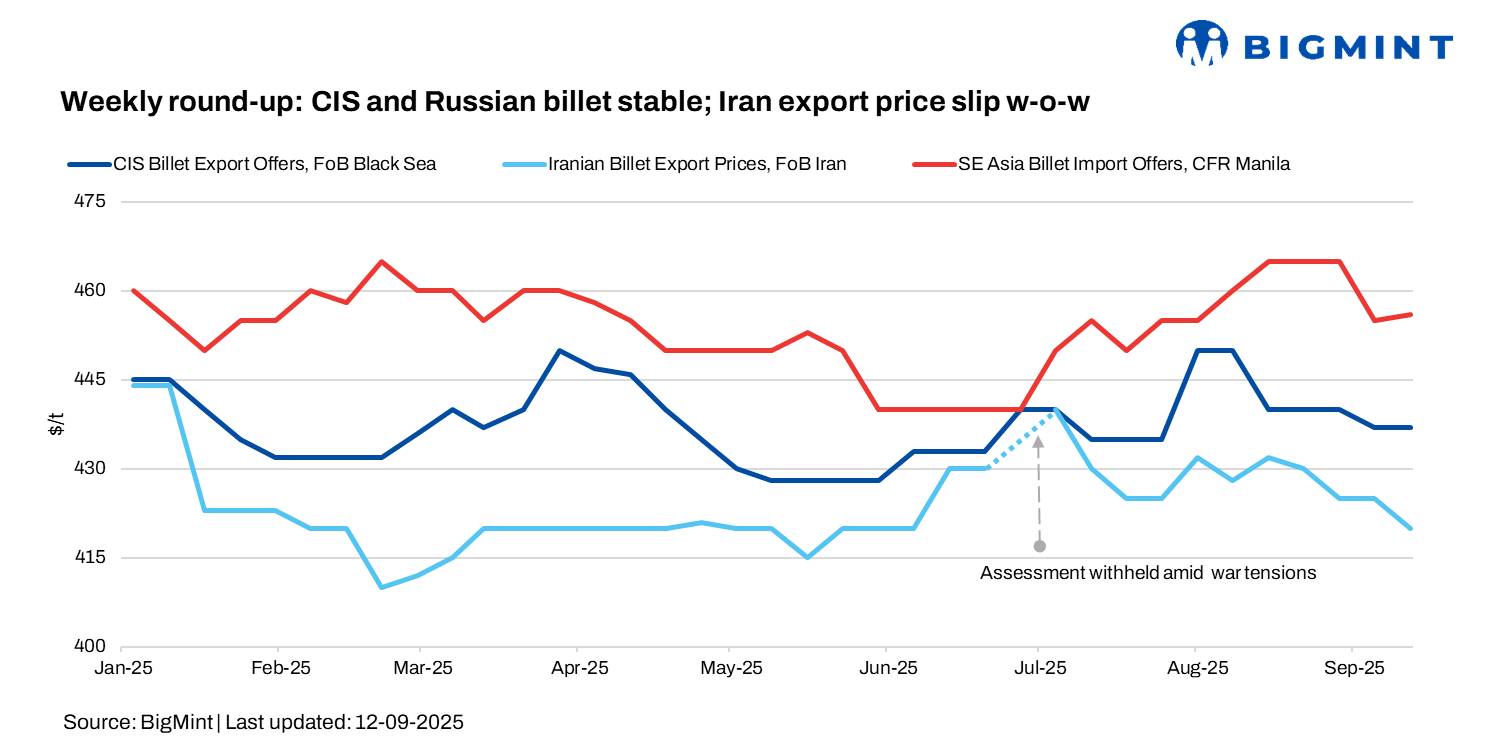

In the 37th week of 2025, global billet prices were range-bound. CIS exporters held offers steady, though price cuts are expected amid a weaker rouble and softer Turkish demand. In Asia, bids for Chinese billet in the Philippines were $450/t CFR, while rare CIS offers to Turkiye appeared at $460-465/t CFR ($440-445/t FOB).

Turkiye’s deep-sea scrap market stayed subdued, with US/Baltic HMS 80:20 at $338-342/t CFR and EU-origin at $326-333/t CFR, as weak demand, slow exports, high freight, and currency swings kept trading thin.

Market highlights

Iran: At the start of the week, Iranian billet was assessed at 343,500 rial/kg, falling to 342,000 rial/kg by 8 September, while rebar declined from 383,000 rial/kg to 378,000 rial/kg. The new currency swap mechanism supported exports, and stable exchange rates are expected to sustain trade activity. Domestic supply increased as power cuts eased, though higher volumes were largely absorbed by exports.

Non-standard-sized billets continued to find buyers in neighbouring markets. By weekend, billet slightly rebounded to 344,000 rial/kg, while rebar slipped further to 375,000 rial/kg. Export reference prices were largely unchanged, with billet at $415-420/t FOB, slabs at $405-410/t FOB.

Southeast Asia: Late this week, Chinese billet was offered at $445-450/t CFR Taiwan, down $5/t from last week, with buyers bidding $440-445/t CFR and no confirmed deals. The broader SE Asian import market also weakened amid muted demand. Chinese 3sp billet was offered at $445-450/t CFR, while in the Philippines, bids for Chinese 5sp stood at $450/t CFR and offers at $455-460/t CFR, with no contracts reported.

Outside SE Asia, a 30,000 t shipment of Chinese 3sp billet sold to Sri Lanka at $460/t CFR for November delivery. By comparison, 15,000 t billet shipped to Sri Lanka in October changed hands at $465/t CFR.

Egypt has imposed a provisional safeguard duty of 16.2% ad valorem, or minimum EGP 4,613/t ($95.7/t), on billet imports, effective 14 September for 200 days. Announced alongside flat steel measures, the move comes after billet imports surged over 1,900% between 2021-2024, including a 220% y-o-y rise in 2024. While integrated mills support the duty to protect local producers, re-rollers warn of potential supply disruptions and higher costs. The market has turned quiet, with concerns that previously booked tonnages may be cancelled to avoid additional charges. The government is promoting production chain integration and is ready to issue licenses for new billet capacities.

In Egypt, 10,000 t of Russian billet was sold for prompt shipment at $480-485/t CFR Damietta ($440-450/t FOB) considered more profitable than selling to Turkiye.

CIS billet exporters largely held offers steady over the week, though price cuts are anticipated amid a weaker rouble and softer Turkish demand despite recent North African deals. Russian semis for end-October-November shipment were offered at $445-450/t FOB Black Sea, with larger mills at the lower end, while rare CIS offers to Turkiye appeared at $460-465/t CFR ($440-445/t FOB), above buyers’ $450-455/t CFR ($430-435/t FOB) expectations.

In China, Tangshan billet closed the week at RMB 3,010/t ($423/t), up RMB 20/t ($4/t), while SHFE Jan’26 rebar fell to RMB 3,127/t ($439/t), down RMB 16/t ($1/t). Billet traded in a narrow RMB 2,990-3,010/t range, with rebar dipping midweek before Friday recovery. Iron ore remained near RMB 800/t ($112/t), coke softened, and EAF losses hit a 13-month high. Inventories rose for the seventh week, keeping demand sluggish, though late-week local billet sales offered some support, and exports stayed steady.

Interest rate updates

- At a 12 September meeting, the Central Bank of Russia cut the key interest rate from 18% to 17%, citing steady economic growth amid high inflation expectations; the next meeting is scheduled for 24 October.

- Meanwhile, Turkiye’s central bank cut its benchmark rate to 40.5% from 43% for a second consecutive meeting, continuing a series of reductions since late 2024 as inflation eased from over 75% to 33% in August. GDP growth exceeded expectations, rising 1.6% quarter-on-quarter in Q2.

Leave a Reply