- LME zinc inventory falls to 50,000 t, lowest since Jun’23

- Hindustan Zinc joins ICMM to promote sustainable mining

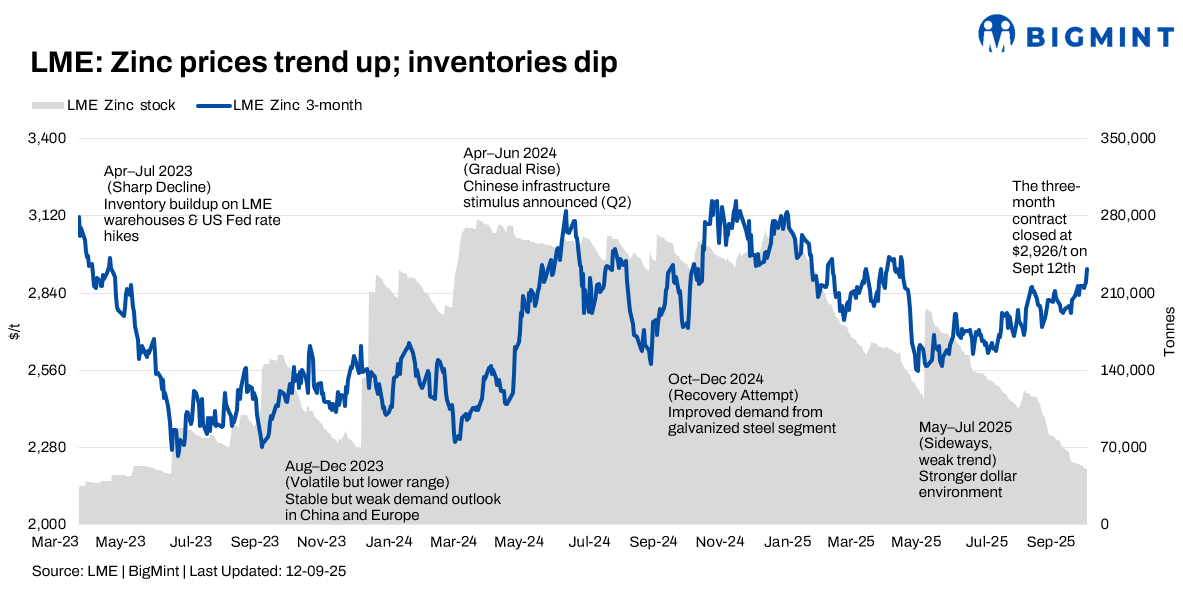

The London Metal Exchange (LME) zinc contract experienced a fluctuating and sideways trend during week 36 (8-12 September, 2025). Prices initially dipped due to profit-taking and lingering concerns over the US economic outlook, but were supported by continued inventory declines and growing expectations for a US Fed interest rate cut. Market volatility remained, with prices witnessing conflicting signals amid tightening supply from overseas and rising Chinese stockpiles.

Price trends

LME zinc cash-settlement prices trended downward in the first half of the week, opening at $2,884.50/t on 8 September. Prices dropped to $2,877.00/t on 9 September and eased further, closing at $2,908.00/t on 11 September.

The three-month LME Zinc contract mirrored this pattern, starting at $2,865.00/t on 8 September and closing at $2,879.50/t on 11 September. While prices did see some fluctuations and intraday profit-taking, the overall trend remained positive towards the end of the week, supported by the continued decline in LME inventories and expectations for a US Fed rate cut.

LME zinc inventories continued their declining trend during the week, falling from 53,075 t on 8 September to 50,525 t by 12 September. As of 10 September, LME zinc inventory dropped to around 50,000 t, hitting a low since June 2023. This continuous destocking indicates a tightening global supply of readily available zinc and provided a strong impetus for late-week price support.

MCX zinc trends (8-12 September)

MCX Zinc prices experienced fluctuations during the week. Prices initially declined on 8 September, settling at INR 273,300/t due to weak demand signals from China. However, prices showed signs of recovery towards the end of the week, with the contract trading around INR 280,000/t on 12 September. This was supported by a softer US dollar and continued tightening LME inventories.

SHFE zinc trend

SHFE zinc prices maintained a fluctuating trend during Week 36. The most-traded SHFE zinc 2510 contract saw price movements influenced by both the strong LME performance and weak domestic demand with rising inventories. While SHFE zinc initially showed some strength, it faced profit-taking later in the week.

The SHFE/LME zinc price ratio pulled back to fluctuate near 7.6, with the import window for zinc ingots into China remaining closed.

Hindustan Zinc joins ICMM, pledges commitment to sustainable mining

Hindustan Zinc Limited, the world’s largest integrated zinc producer, has become the first Indian company to join the International Council on Mining and Metals (ICMM). Following an independent assessment, the membership highlights the company’s dedication to sustainable mining practices, adhering to 40 performance expectations covering environmental, social, and governance standards, validated across all its assets.

Outlook

The near-term outlook for zinc remains uncertain, as the market is grappling with conflicting signals. While declining LME inventories indicate tightening supply, the continued build-up in Chinese inventories due to weak demand is a significant bearish factor. Global macroeconomic uncertainty, particularly US Fed policy, and ongoing trade tensions will likely dictate short-term price direction. The rising trend in imported zinc concentrate TCs suggests a tight raw material market, which could affect future refined zinc supply. The market will be closely watching for signals of a genuine pick-up in Chinese demand.

Leave a Reply