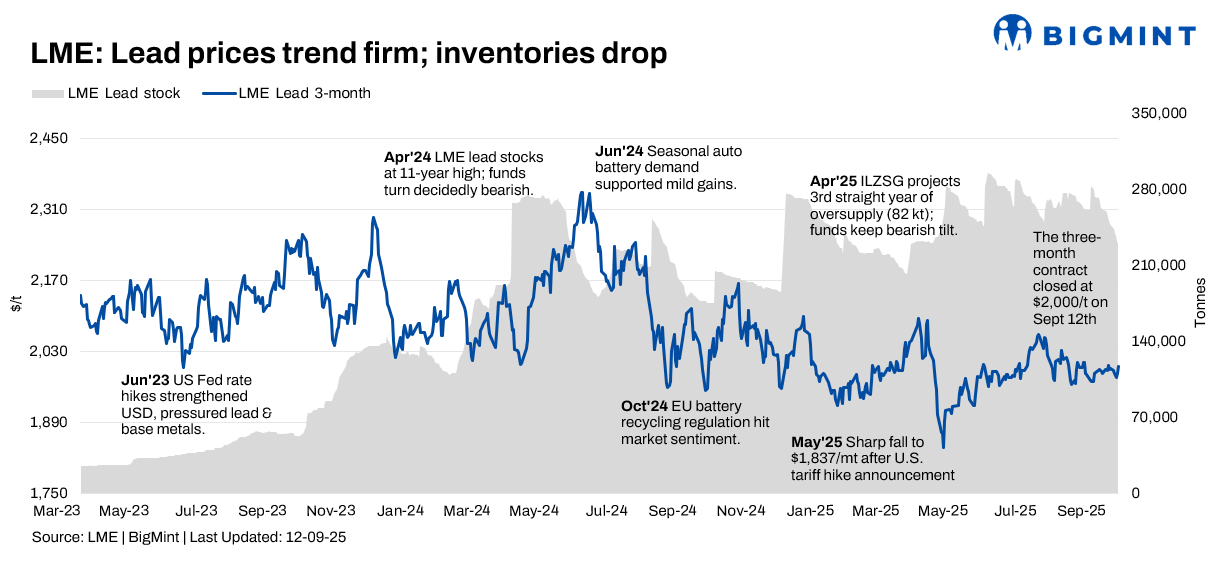

- LME lead inventories continue to decline

- Chinese and LME inventories to influence prices

The lead market, both globally and in India, experienced a week of fluctuations and limited trading during week 36 before closing higher on Friday. The market received conflicting signals, with a mid-week dip driven by US inflation data, followed by a strong rebound supported by regional supply tightness and positive late-week sentiment.

Price trends

LME lead cash-settlement prices fluctuated throughout the week. The market opened at $1,989.5/t on 8 September, consolidating around the $1,990/t level in the first half of the week. A mid-week dip, influenced by lower-than-expected US inflation data, saw prices fall to a low of $1,972/t. However, a strong rebound in the second half of the week, reaching a high of $2,004/t in late trading, led to a final closing price of $2,001/t on 12 September, up 0.65% for the week.

The three-month LME lead contract mirrored this pattern, also showing fluctuations before rebounding to close at $2,001/t on 12 September.

LME lead inventories continued to decline during the week, reaching 232,625 t by 11 September from 243,125 t on 8 September. This continued destocking contributed to a tightening global supply of readily available lead and helped support the late-week price rebound.

MCX lead trends (8-12 September)

MCX lead prices reflected volatile global sentiments, as well as the influence of domestic factors. The September contract closed at INR 182,050/t on 12 September, down 0.25% from the beginning of the week. Prices fluctuated throughout the week, influenced by global cues and domestic demand patterns. The Indian market was supported by factors such as the rupee’s performance, while tepid demand from battery manufacturers and weak global trends weighed on lead futures earlier in the week.

SHFE lead trend

SHFE lead prices also showed a fluctuating trend during the week, ultimately closing higher. The most-traded contract started at 16,915 yuan/t, experienced a mid-week low, and then rebounded to close at RMB 17,040/t on Friday, marking a 0.83% increase.

Market factors and influences

US inflation data, with August PPI down 0.1%, caused mid-week LME lead prices to dip from $1,989.5/t to $1,972/t. The Indian rupee’s fluctuations impacted MCX prices, which closed at INR 182,050/t. Supply tightness from Chinese smelter maintenance and mixed demand patterns influenced regional and global lead price movements.

PeakAmp raises INR 12 crore to boost battery recycling

PeakAmp has secured INR 12 crore in funding to expand its battery recycling operations in India. The investment will support the company’s sustainable initiatives, helping tackle growing battery waste. PeakAmp aims to enhance its technology, infrastructure, and partnerships to promote clean energy solutions and strengthen the circular economy, positioning itself as a key player in eco-friendly battery management.

Outlook

The near-term outlook for lead appears cautiously optimistic, particularly for the SHFE market due to regional supply tightness. However, global prices will likely remain sensitive to broader economic changes and the balance of global supply and demand. Market participants will be closely watching demand and inventory levels in both the LME and Chinese markets for future price indications.

Leave a Reply