- Buyers in Vietnam cautious amid high inventories

- Range-bound price trend to continue in near term

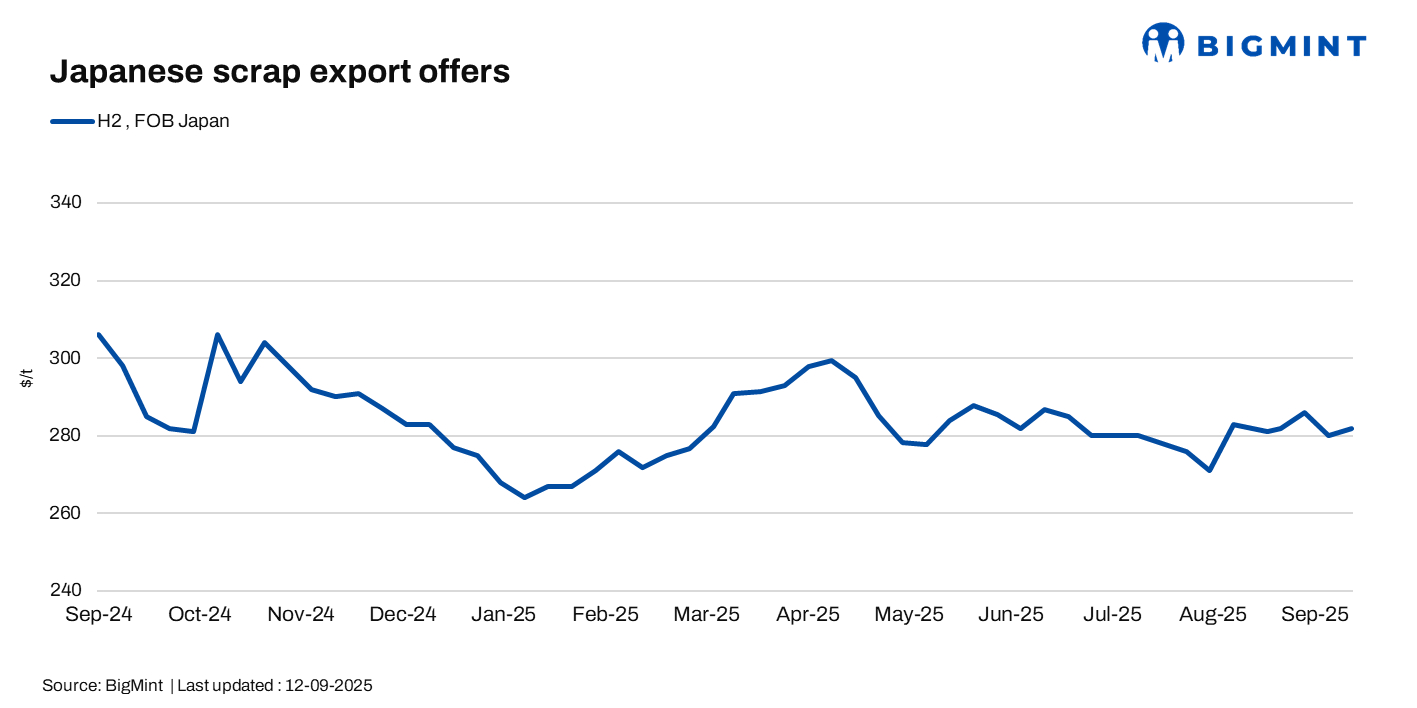

Japan’s H2 scrap export prices remained range-bound w-o-w, supported by a wider range of offers. Ahead of the September Kanto tender, most market participants remained cautious, and this trend continued in the days after, with the results unlikely to exert much influence on pricing.

BigMint assessed H2 at JPY 41,600/t ($282/t) FOB Tokyo Bay, down JPY 100/t ($1/t) w-o-w.

A Japanese trader noted that H2 scrap offers to Vietnam were in a broader range of $320-330/t CFR, with mainstream bids at around $320/t CFR.

Market activity was subdued ahead of the September Kanto tender, as some traders held back offers until results were announced. The tender saw a single successful bid of JPY 41,970/t ($285/t) for a 15,000‑t cargo to Bangladesh, up JPY 82/t m-o-m but unchanged in USD. This outcome is expected to have a limited near-term impact on Japanese scrap export prices.

Key market updates

Vietnam: Demand for H2 scrap remained cautious this week, with buyers reluctant to accept higher Kanto tender prices. Compared with August cargoes, current offers were considered challenging amid rising ocean freights.

US-origin deep-sea H2 scrap was range-bound at $350/t CFR Vietnam, with bids at around $340-345/t and tradable levels near $345/t. Reports of a potential $340/t CFR deal circulated but remained unverified, while mills largely stayed on the sidelines due to high scrap inventories.

Taiwan: H2 demand softened, with Feng Hsin Steel reducing local scrap procurement prices due to weak rebar trade, falling global tags, and subdued Chinese market conditions, which pressured overall buying activity.

Outlook

Looking ahead, Japanese export prices are expected to remain range-bound in the near term, while demand in Vietnam and Taiwan may stay cautious amid high inventories, weaker domestic steel demand, and logistical pressures.

Leave a Reply