- Bangladesh stays on sidelines after completing Sep bookings

- Turkiye expected to finalise major Sep bookings next week

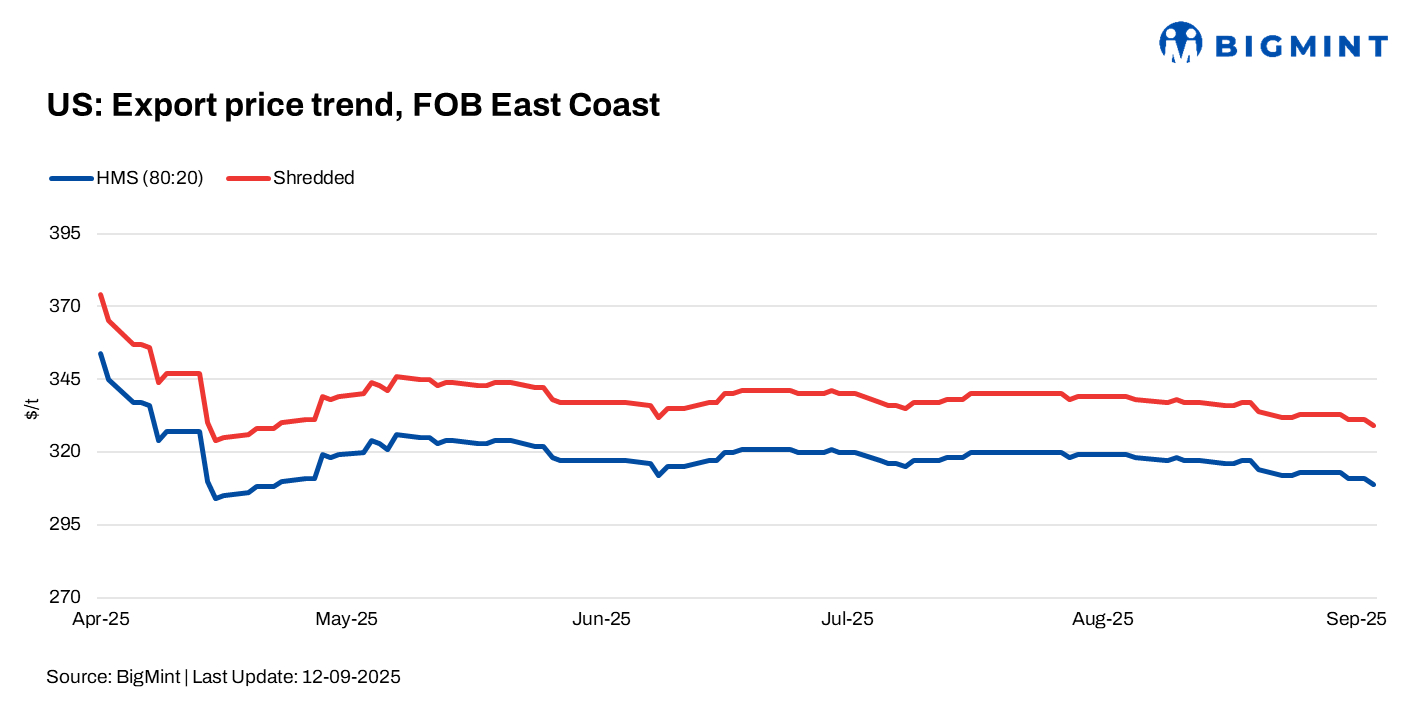

US ferrous scrap export prices eased slightly, by $4/tonne (t) w-o-w, amid a softening scrap market in Turkiye and Bangladesh, which contrasted with largely stable finished steel prices in key regions. In China, rebar continued its upward trend, while Asian billet markets faced pressure, as buyers remained cautious amid high inventories.

September export transactions indicate a $5-6/t decline from mid-August levels, reflecting weakness due to cautious buyer sentiment. Rising freights also fostered hesitancy among buyers. Freights to Turkiye stood at $42/t, up $7/t w-o-w amid vessel supply-demand imbalances.

Domestically, the US ferrous scrap market remained subdued, with limited negotiation activity. Both buyers and sellers stayed passive, resulting in slight declines in prime scrap prices.

FOB assessments (US East Coast, bulk)

- HMS 80:20 – $309/t, down by $4/t w-o-w.

- Shredded – $329/t, down by $4/t w-o-w.

Updates on key importers

Turkiye: Demand for US-origin ferrous scrap remained muted this week, with deep-sea import prices easing slightly. Cautious sentiment, amid soft domestic and export steel demand, kept fresh deals minimal.

Factors shaping Turkish scrap demand

- Turkish mills remained selective, with weak steel demand limiting import volumes.

- Major shipments for September are largely expected to be finalised by next week.

Despite the slight price dip, Turkish mills continued with a cautious purchasing approach, waiting for clearer signals on upcoming demand.

Bangladesh: Demand for US-origin scrap remained selective, with most large buyers on the sidelines after completing September bookings. Limited fresh deals occurred, as mills stayed cautious amid weak domestic steel demand and liquidity constraints, while European suppliers largely stayed absent. Containerised trades remained sluggish due to wide bid-offer gaps.

US-origin HMS 80:20, bulk – CFR assessments

- Turkiye – down by $3/t w-o-w at $340/t.

- Vietnam – down by $2/t w-o-w at $342/t.

- Bangladesh – up by $1/t w-o-w at $352/t.

Outlook

October is expected to remain mostly flat, with stronger pricing and better order books anticipated in November and December, according to market participants.

Leave a Reply