- Rising charterer interest leads to active fixtures in Pacific basin

- Brazil–China corridor records improvement in exchanged rates

Dry bulk iron ore freight rates continued to reflect mixed trends this week, firming on the Australia-China and India-China routes, while edging lower on Atlantic basin routes such as Brazil-China and South Africa-China, highlighting divergent demand-supply dynamics across regions.

“Time charter (TC) sentiment is up, reflecting owners’ optimism and improved vessel demand outlook. With bunker costs easing, voyage expenses are lower; however, net freight earnings have edged down slightly, as spot market activity and cargo demand remain relatively soft“, said a source.

Capesize freight rates extended gains this week, supported by robust activity and a flurry of fixtures, particularly on the Australia-China route, BigMint noted.

Market confidence strengthened further as the Pacific witnessed vibrant exchanges, underpinned by a healthy flow of fresh orders and charterers moving with greater urgency to secure tonnage.

At the same time, period interest remained firm, with several fresh fixtures reported concluded. Tonnage demand held relatively firm, with key Western Australia mining majors – BHP, FMG, and Rio Tinto – actively seeking vessels.

Activity in the Atlantic started off fairly thin this week, with only limited participants attempting to conclude trades. Later, however, BigMint observed rate levels on the Brazil–China route edging higher, supported by positive momentum in the Pacific. Rates on the route also reflected a forward premium, with later loading dates (future shipments) quoted or fixed at higher freight levels than near-term loadings, particularly for late September to October windows.

Route-wise updates

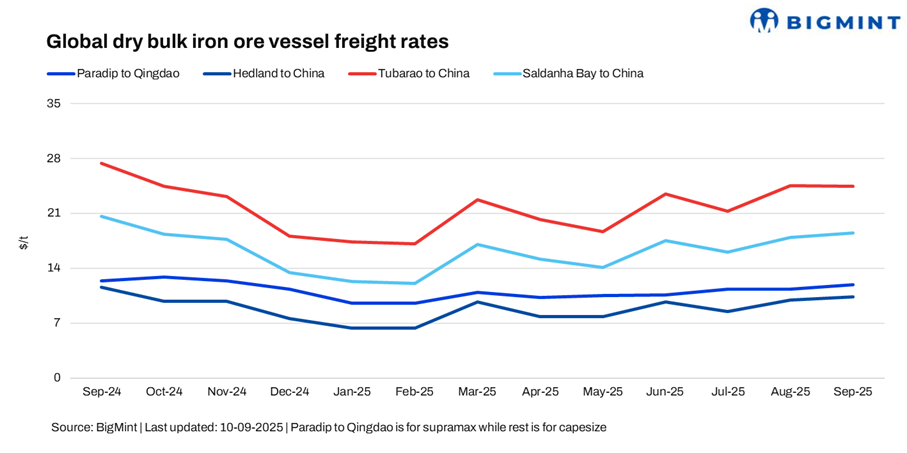

- India (Paradip)-China (Qingdao), Supramax: Freights for Supramax vessels from the Indian Ocean to China remained stable w-o-w at $11.94/dmt. “The market is firming as iron ore traders rush to sell and export cargoes following news of a potential 30% export duty on low-grade iron ore from early October”, a Mumbai-based shipbroker told BigMint.

- Australia (Port Hedland)-China (Qingdao), Capesize: Capesize freights for iron ore shipments from Western Australia to China increased by $0.29/dmt w-o-w to $10.49/dmt. On the Australia-China route, initial Capesize offers were heard around $9.9/dmt, before firming to approximately $10.5/dmt, according to fixtures data compiled by BigMint.

- Brazil (Tubarao)-China (Qingdao), Capesize: Capesize freights for Brazil to China shipments, on contrary, witnessed a drop of $0.08/dmt w-o-w, settling at $24.42/dmt. On the Tubarao-Qingdao route, three fixtures were reported this week at around $23.6-24.5/dmt. The modest decline contrasts with firmer rates on Pacific basin routes, highlighting the impact of varied demand–supply dynamics across the two regions. Traders remained cautious amid ongoing uncertainty, while some charterers continued to secure vessels for near-term requirements.

- South Africa (Saldanha Bay)-China (Qingdao), Capesize: Capesize freights from Saldanha Bay to Qingdao followed the suit and edged lower by $0.04/dmt w-o-w, settling at $18.46/dmt. Freight levels on the South Africa-China route moderated this week, with activity relatively subdued with no fixtures reported.

Market highlights

- Baltic index hits over 1-month high: The Baltic Exchange’s main dry bulk sea freight index rose significantly w-o-w on 10 September driven by higher rates across all vessel segments. The overall index increased around 93 points w-o-w to 2,079, with the Capesize index rising sharply by around 142 points to 3,016. Additionally, the Supramax segment also increased by 7 points w-o-w to 1,473.

- DCE iron ore futures head north on supply concerns: Iron ore futures on the Dalian Commodity Exchange (DCE) for the January 2026 contract rose by around RMB 28/t ($4/t) at RMB 805/t ($113/t) on 10 September. Iron ore futures climbed driven by mounting concerns over supply prospects from the giant Simandou project in Guinea, coupled with expectations of improving demand in top consumer China.

Outlook

Near-term dry bulk iron ore freight rates to China show mixed trends. Australia-China and Brazil-China routes are supported by steady exports and active Capesize demand, though softening Chinese steel demand and potential oversupply keep the outlook cautious.

In contrast, India–China freight remains under pressure as monsoon-related quality concerns and preference for high-grade ore limit bookings. Overall, while some routes benefit from steady flows, challenges persist for India-origin cargoes.

Leave a Reply