- Flats demand improves m-o-m but remains sluggish y-o-y

- Leading producer reportedly considering another price hike

India’s stainless steel finished flats market held mostly steady this week, with 304-series prices unchanged while 316-series tags gained on firm molybdenum costs.

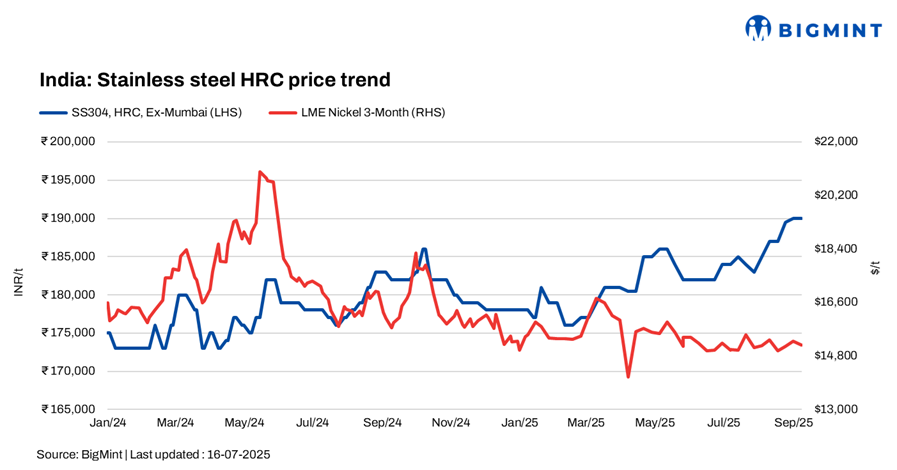

BigMint assessed 304-series hot-rolled coils (HRCs) at INR 190,000/t ex-Mumbai, flat w-o-w, while 304L black round bars (25-100 mm) remained at INR 158,000/t.

In contrast, 316-series HRCs rose INR 2,000/t w-o-w to INR 340,000/t, and cold-rolled coils (CRCs) gained INR 3,000/t to INR 343,000/t.

The flats market remained sluggish, with traders offering 3-4% discounts to liquidate stocks. Demand was heard to be decent but still subdued compared to last year’s peak season, though slightly stronger m-o-m. Sources suggested a leading stainless steel manufacturer was considering another price hike, backed by a strengthening dollar and firm raw material costs. Imports remained absent due to BIS restrictions, making it challenging for small- to medium-scale mills.

Longs demand stayed subdued as buyers held sufficient scrap inventories and remained active in billet bookings, including a recent 1,000-t deal for 304L billets from Indonesia at $1,525/t. Seasonal factors such as the monsoon and festive slowdown during Ganesh Chaturthi further curbed industrial activity, while liquidity pressures kept sentiment weak.

LME nickel tags dip

At the time of reporting, three-month nickel prices on the London Metal Exchange (LME) stood at $15,160/t, down 0.9% from last week’s $15,295/t. Nickel stocks at LME-registered warehouses stood at 218,070 t, up 3.7% compared to 210,234 t in the previous week.

Chinese stainless steel, NPI prices remain stable

In China, prices of domestic stainless steel 304-grade CRCs stood at RMB 12,800-12,900/t ($1,798-1,812/t) exw, stable w-o-w, while FOB tags of 304-grade CRCs were firm at $1,920/t.

Chinese portside prices of nickel pig iron (NPI) (8-12%) remained firm w-o-w at RMB 953/t ($134/t). Meanwhile, Indonesian FOB prices of NPI (12-14%) stood at $117/t.

Raw materials scenario

Ferro molybdenum: Indian ferro molybdenum prices surged by INR 66,000/t ($749/t) w-o-w to INR 3,166,000/t ($35,915/t) exw, tracking LME futures, which hit a two-year high of $25.93/lb on 8 September. Sellers lifted offers, but buyers stayed cautious, limiting trades to around 10 t last week. Global trends were mixed: Chinese prices eased, while US and European tags strengthened.

Ferro silicon: Prices dropped INR 5,200/t w-o-w to INR 86,000/t ($976/t) exw-Guwahati, aligned with Bhutan’s revised offers. Trades for about 500 t were recorded at similar levels.

Ferro chrome: Indian high-carbon ferro chrome (HC60%) prices rose INR 4,400/t w-o-w to INR 118,100/t ($1,342/t) exw-Jajpur.

Ferrous scrap: The imported scrap trade was quiet, with HMS bulk offers near $365/t CFR Kandla but bids closer to $345/t. UK-origin HMS 80:20 was offered at $330-335/t CFR, while buyers held bids at $325/t, stalling deals.

Outlook

The stainless steel market is likely to face more upward pressure in the coming weeks, with raw material costs, firm dollar exchange rates, and a potential hike by a leading stainless steel manufacturer shaping sentiment. While discounts may provide temporary relief for buyers, limited imports and liquidity constraints remain key challenges in the flats segment.

Leave a Reply