- JSW’s intake rises further, SAIL stays steady

- Russia boosts exports, doubling shipments

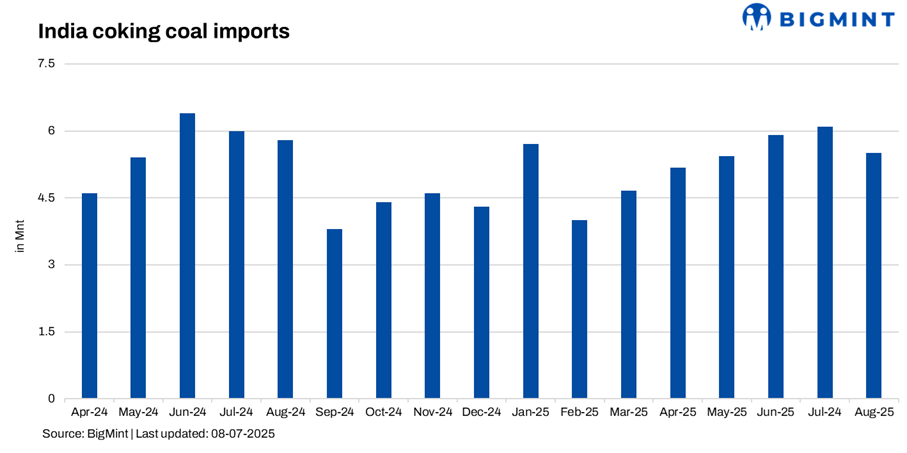

India’s coking coal imports fell 10% m-o-m to 5.5 million tonnes (mnt) in August 2025 from 6.1 mnt in July. Notably, July imports, at 6.1 mnt, were higher than the usual monthly average, owing to restocking needs and the arrival of vessels booked earlier, when prices had witnessed a drop.

The decline in August imports was led by lower arrivals at Paradip, Dhamra, and Jaigarh, though Gangavaram and Krishnapatnam recorded slightly higher inflows. Cumulative imports for April-August were up 8% y-o-y to 27.7 mnt against the same timeframe last year.

Australia still leads, Russia doubles shipments

Imports from Australia slipped to 2.5 mnt in August from 3.8 mnt in July, though it remained the largest supplier. Russia’s volumes nearly doubled to 1.2 mnt from 0.6 mnt. Mozambique also improved to 0.7 mnt, while shipments from the US remained nil in August compared to 0.6 mnt in July. Canada contributed 0.2 mnt, while minor volumes came from Indonesia (0.1 mnt).

JSW leads buyers, Tata scales down sharply

JSW Steel emerged as the top importer, raising intake to 1.7 mnt in August from 1.4 mnt in July. SAIL maintained steady buying at 1.1 mnt, while Tata Steel halved its intake to 0.5 mnt. RINL increased imports to 0.7 mnt from 0.5 mnt, while Jindal Steel and Power’s volumes remained unchanged at 0.5 mnt.

Factors contributing to lower coking coal imports

India’s imported coking coal prices surge m-o-m: BigMint’s premium hard coking coal (PHCC) index was assessed at a monthly average of $202/tonne (t) CNF India in August, up sharply by $9/t against $193/t in July. Bid-offer disparities led to lower trade activity in India.

Met coke prices edge up m-o-m: Indian met coke prices moved slightly higher m-o-m, with the BF-grade assessed at INR 29,000/t exy-Jajpur, up INR 300/t, while exy-Gandhidham tags rose INR 800/t to INR 30,000/t. The uptrend was supported by limited import availability, as post-QR allotments took longer to materialise, leaving buyers dependent on domestic met coke. This reliance on local supply provided firm support to prices.

BF-rebar prices dip m-o-m: Blast furnace (BF) route rebar (Fe500D) prices dipped by 1% to average INR 48,080/t exy-Mumbai, driven by subdued demand. Expecting a market rebound, Indian primary mills had increased list prices by up to INR 2,000/t for early-August 2025 deliveries. However, prices softened eventually, with inventories being higher by over 45% m-o-m.

Outlook

Indian steel mills may go for coking coal restocking following the withdrawal of the monsoon. Arrivals for previous bookings are also expected in September.

Leave a Reply