- Limited imports push up Australian zinc premiums

- LME futures hit 5-month high on sharp inventory drop

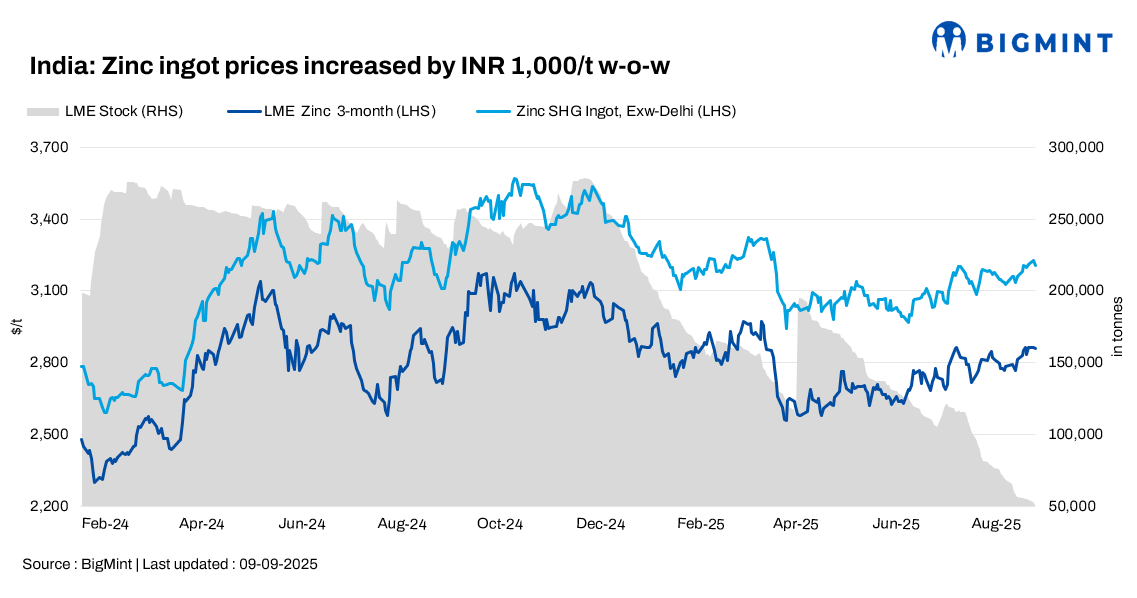

India’s zinc ingot (99.995%) prices rose by INR 1,000/tonne (t) w-o-w to INR 283,000/t ex-Delhi, as per BigMint’s assessment. The increase was driven by tight availability in key consumption hubs; higher premiums on Australian-origin material, despite stability in official pricing; and an unclear market outlook.

On 8 September 2025, Hindustan Zinc Limited (HZL) kept its zinc ingot prices unchanged after raising rates by INR 8,100/t on 4 September, tracking earlier supply constraints.

Traders highlighted that Special High Grade (SHG) zinc ingots were offered at INR 276,000/t ex-Mumbai, up INR 1,000/t from last week, with Australian-origin lots quoted at a premium of $700/t over LME prices at CFR Mundra Port amid limited imports.

In the import market, uncertainties due to BIS norms and lack of clarity on fresh orders reduced buying appetite, though some demand for Korean zinc persisted with trades at INR 282,000-284,000/t in Delhi.

In north India, Australian zinc was offered at INR 375,000/t ex-Delhi, up INR 10,000/t w-o-w, with expectations among traders that prices may approach INR 390,000/t in the near term amid supply shortages.

Market commentary

“The market is still in wait-and-watch mode. Seasonal rains have slowed everything down, especially in the north. Buyers are mostly purchasing only what they need — no one is taking large positions right now due to weak offtake and cash flow delays,” said a Delhi-based zinc trader.

“We have seen some pick-up in buying from infrastructure and auto component makers, but galvanisers and oxide units are still running at low capacity. Orders are slow, and the rains have not helped. It is not the time for bulk procurement yet,” noted a secondary ingot producer from Punjab.

Global zinc futures snapshot

LME zinc futures rose for a second straight day, reaching $2,876.5/t on 9 September, a five-month high. Prices gained 1.2% over two days, supported by a weaker US dollar and a sharp inventory drop. LME zinc stocks fell by 975 t to 53,075 t, with current levels marking a 49.3% decline compared to the end of last year. This significant supply reduction strengthened price momentum.

On the Shanghai Futures Exchange (SHFE), the September zinc contract hovered at around RMB 22,445/t, with Chinese demand showing gradual improvement amid restocking activities.

In India, MCX zinc September futures were assessed at INR 275,800-276,000/t, reflecting constrained supply and firm premiums in the spot market.

Outlook

The zinc market is likely to remain supported in the coming weeks due to persistent supply tightness and elevated import premiums, particularly for Australian-origin material. However, demand recovery is expected to remain selective, with infrastructure and auto component sectors showing limited pick-up, while galvanisers and oxide units stay cautious. Seasonal rains, regulatory uncertainties, and logistical challenges are expected to keep buyers hesitant, with market participants closely watching global cues and localised supply gaps for further price movement.

Leave a Reply