- GST rate cuts in autos, durables, and cement set to lift steel demand despite no direct tax change.

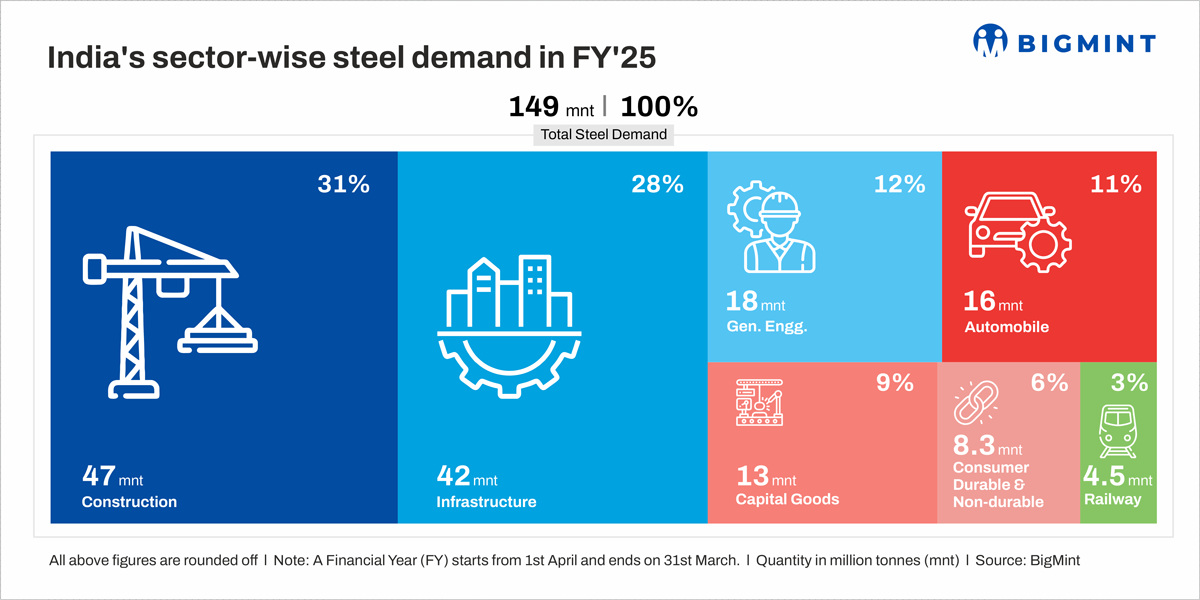

- Construction and infrastructure, with 59% steel demand share, gain major cost relief from GST reform.

The long-awaited reform and rate rationalization in Goods and Service Tax (GST) looks well-timed coming just before the beginning of the festive sales. The change eliminates 12% and 28% tax rate slab and brings 99% of items under three slabs of 0%, 5% and 18%. This would improve ease of compliance and reduce the scope of dispute. While the reforms bring down the tax rate for large number of goods and services, some of the luxury and sin goods would face higher taxes. As a result, against a gross loss of Rs 93,000 crore, net revenue loss is estimated at Rs 48,000 crore, with higher revenue from the other category partly offsetting it.

Steel Industry impact

While the steel industry does not see any change in rate, change in tax rate for key consuming sectors – the consumer facing goods such as automobiles and consumer durable goods (Air conditioners, TVs etc), and several goods essential for construction and infrastructure sector can led to demand boost. The consuming industries are also expected to get a push through imports replacement or higher exports with domestic production becoming more cost competitive. Also, while tax rate on kitchen utensils of steel (and other materials such as aluminium, iron and copper) has been reduced from 12% to 5%, the impact on total steel demand may not be significant.

Automobile sector is on top of the chart with reduction in tax rate from 28% (plus cess at different rates) to 18% for most of the two-wheeler, four-wheeler and commercial vehicles segments, whereas certain premium segment would see its rate come down to 40% from up to 50% currently. The only exception is high-end two wheelers (> 350 cc) where the rates have gone up to 40%. Automobile is an important demand driver for steel, accounting for 11% of total consumption in FY25, in volume terms, but a high value business. Steel consumption for the sector has grown at 10.5% CAGR during FY19-FY25, the highest of eight different segments tracked by BigMint, and 4 percentage points higher than rest of the industry. However, growth rate is projected to come down to 7% during FY25-30, as per BigMint, making the rate cut that much more important. Rate cut for consumer durables segment should also drive similar gains, although to a lesser extent with share in total demand at about 5%.

Construction and infrastructure

From steel demand point of view, construction and infrastructure are two important sectors, accounting for 31% and 28% of total demand. Both the sectors have got a boost with reduction in GST on cement from 28% to 18%, whereas construction gets additional benefit from reduction in rates for other building materials such as marble, granite etc. Yet, whether the cut would spur additional demand for construction would depend upon whether the industry players pass on the cost benefit, and whether the government is able to ensure that the rate cut is passed on, considering the complexity of the sector. Also, while the government led infrastructure sector would see a reduction in cost, this may not lead to sanctioning of more projects immediately.

To Sum Up

The GST reform has come about after the US tariff imposition threatened to derail India’s growth momentum and should lead to significant savings and demand boost and can spur a higher investment cycle. Several essential categories such as biscuit, chocolate, toothpaste, soaps etc, have seen sharp rate reduction, from 18% to 5%, which reduces the price gap between branded and unbranded goods, and should lead to more formalization of the economy. Yet, it would be essential to see how the consumers and producers react to the changes, before taking a firm view of the gains.

Leave a Reply