- AM/NS auction receives up to INR 400/t premium

- Market expects iron ore supply to improve in September

Iron ore prices in Odisha remained firm this week, supported by need-based buying from steelmakers and traders, despite limited material availability in the market. Lower-grade fines witnessed active buying interest, largely driven by improved activity in the export market.

Price update

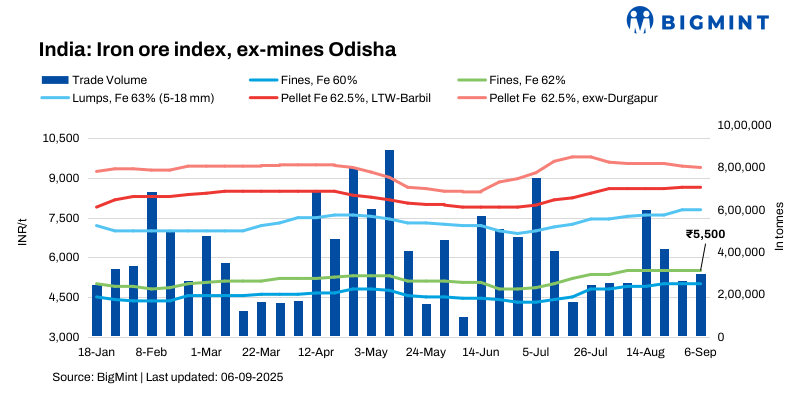

BigMint’s Odisha iron ore fines (Fe 62%) index remained stable w-o-w at INR 5,500/tonne (t) ($62.5/t) ex-mines on 6 September 2025. BigMint recorded deals for around 300,000 t in Odisha, concluded by direct sales. The market concluded Fe62% fines deals at the level of INR 5,500-5,600/t ex-mines this week with a need basis volume. Prices have remained firm since mid-June, showing the material scarcity along with active demand.

AM/NS sold around 300,000 t of iron ore from 352,000 t offered from Odisha on 3 September, with premiums of up to INR 400/t. From Thakurani mines, 120,000 t fines (Fe 57-59%) booked at INR 3,600-4,600/t (INR 100/t premium); 48,000-t lumps (5-18 mm, Fe 56.5-59%) remained unsold. Sagasahi mines sold 52,000-t lumps (5-18mm, Fe 58.5-62.5%) booked at INR 5,925-7,250/t (base prices INR 5,800-7,000/t) and 132,000-t fines (Fe 53.5-56.5%) at INR 2,775-3,600/t (base INR 2,350-3,400/t). Prices include royalty.

Market highlights

Market participants noted that downstream steel prices showed a slight uptrend, which in turn supported iron ore demand. However, buyers remained cautious as current offers from miners are on the higher side. A buyer informed, “Miners are largely accepting small-lot orders, while bulk deals have remained limited due to supply constraints.”

Market participants also noted that the ongoing shortage of high-grade fines has led to deals being concluded at prevailing offers without much negotiation. A steelmaker added, “High-grade fines are difficult to source at present, so buyers are agreeing to current levels for urgent requirements.”

Looking ahead, supply is expected to improve as the monsoon season slows down. A prominent miner commented, “Iron ore production and dispatches are likely to improve in September, which should boost trading activity and meet the increasing demand.”

Still, many buyers are waiting for the upcoming Odisha Mining Corporation (OMC) auction to secure bulk volumes at competitive prices, keeping advance restocking muted for now.

Factors affecting iron ore prices

Pellet offers drop w-o-w: Pellet (6-20 mm, Fe 62.5%) prices in Odisha’s Barbil fell by INR 100/t ($1/t) w-o-w to INR 8,600/t ($98/t) loaded to wagon. Pellet (Fe 62.5%, 6-20 mm) prices in Durgapur also inched down by INR 100/t ($1/t) w-o-w to INR 9,350/t ($106/t) exw on 5 September

Sponge iron prices rises w-o-w: According to BigMint’s assessment, sponge iron C-DRI (FeM 80%) prices in Rourkela increased by INR 500/t ($6/t) w-o-w to INR 26,100/t ($296/t) on 6 September.

Billet prices up w-o-w: Meanwhile, steel billet (100*100 mm) prices in Rourkela rose by INR 200/t ($2/t) w-o-w to INR 36,400/t ($413/t) today.

Rationale

- T1- Five (5) deals for Fe62% fines were recorded in the publishing window, and all were considered for price computation. These were given 50% weightage for index calculation.

- T2 – BigMint received seventeen (17) offers and indicative prices under the T2 category (offers, indicative, and bids) in this publishing window. Fifteen (15) were taken into consideration and given 50% weightage. To check BigMint’s iron ore assessment, pricing methodology, and specification document, click here.

Outlook

According to BigMint’s analysis, the Odisha iron ore market is likely to remain firm in the near term on the back of active demand, though prices could witness volatility as supply improves and auction activity gains pace.

Leave a Reply