- Rising inventory, softening global demand pressure HRC prices

- Rebar prices drop as end-user demand continues to disappoint

- Capacity regulation may offer some support to steel prices

Morning Brief: After a significant surge in late-July 2025, Chinese steel prices continued to shed gains in August on weak end-user demand signals. Notably, surging futures, optimism due to a trade truce with the US and declining inventories at CISA-affiliated steel mills in late-July had offered support to prices.

Moreover, the rally in the raw materials markets fuelled price rise in August, Benchmark Australian iron ore fines prices gained $3/tonne (t) m-o-m to a monthly average of $102/t CFR China in August on production restrictions imposed in mid-August on certain steel mills in Tangshan to combat air pollution. Safety and environmental checks at coking coal mines and successive rounds of hikes in coke prices amid tight supplies continued to support steel prices.

However, in the second half of August, steel prices lost ground under the pressure of ample supply. Despite hot and damp weather in summer causing steel demand from end-users to wane, domestic steelmakers kept production high last month to rake in profits. A Mysteel survey showed that during 21-27 August, output of the five major carbon steel products among 184 steel mills across China totalled 8.8 million tonnes (mnt), higher by a remarkable 13.6% compared with the same period last year.

Snapshots of rebar, HRC price movements

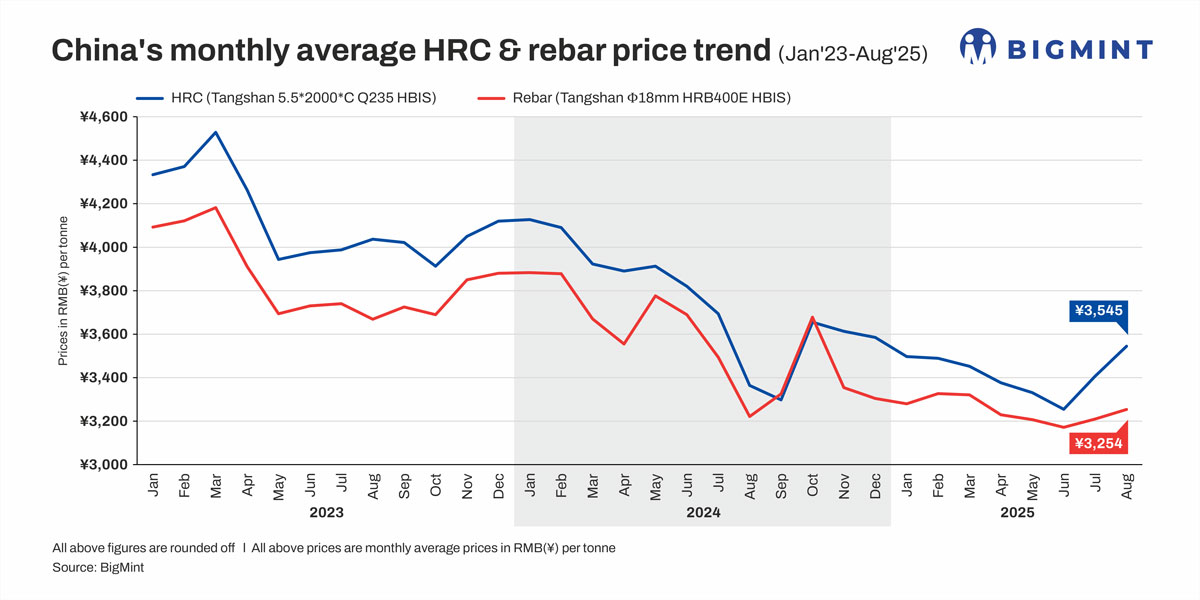

Supply overhang, sluggish demand weigh on rebar: Chinese rebar prices fluctuated through August, moving between RMB 3,220-3,320/t ($444-463/t), largely tracking SHFE futures volatility. Early in the month, futures-led declines and subdued end-user demand, weighed by heavy rainfall and high temperatures, pressured spot prices. Brief upticks occurred mid-month, but persistent weather disruptions, weak construction activity, and rising inventories soon dragged prices lower.

Most downstream buyers maintained cautious, just-in-time purchasing strategies, limiting market support. Overall, sentiment remained bearish, with supply overhang and sluggish demand dampening recovery prospects despite a temporary rebound.

Downtrend in export demand impacts HRC prices: Chinese HRC prices witnessed mixed movements through August, with domestic offers fluctuating in a narrow range between RMB 3,220-3,290/t ($449-458/t), tracking SHFE futures volatility. Export offers initially climbed to $490/t but later softened to $480/t as buying interest weakened amid higher prices.

Market sentiment reflected cautious optimism, yet fundamental pressures persisted from rising inventories, elevated production, and sluggish downstream demand. Seasonal slowdown, logistical challenges, and mill destocking weighed on trading activity, while environmental production curbs in northern China provided brief support. Overall, the market remained resilient but fragile, with undervalued prices and subdued export appetite shaping monthly trends.

Outlook

The steady decline of container export freight shows that steel demand from end-users overseas is shrinking. As the US tariff hikes continue for an extended period and are compounded by additional tariffs on steel, effective from 18 August, the pressure on China’s steel exports will intensify, and prices will edge lower.

Although many BF mills in North China had been required by local governments to halt operations late last month to improve air quality in the region, these mills will restart production during the first two weeks of September. Moreover, cost support for steel prices is expected to waver this month as prices of raw materials such as iron ore and coke are likely to retreat.

In January-July this year, steel production in China fell by 3.1% y-o-y to 594.47 mnt, which means a drop of 19 mnt compared to the same period in 2024. The rate of decline has slowed down compared to 50 mnt predicted in March-April. However, a recent document prepared by the Ministry of Industry and Information Technology, the Ministry of Natural Resources, the Ministry of Ecology and Environment, the Ministry of Commerce, and the State Administration of Market Regulation refers to “precise regulation” of capacities, the closure of obsolete equipment, and support for high-tech production.

According to market estimates, steel output in 2025 will be less than 980 mnt, which is at least 25 mnt lower than in 2024. If production regulation and the ‘anti-involution’ policy lead to output curtailment, steel prices may find some support in the last few months of 2025.

Leave a Reply