- Cautious sentiment prevails, with need-based buying

- Raw material prices drop, dragging down finished tags

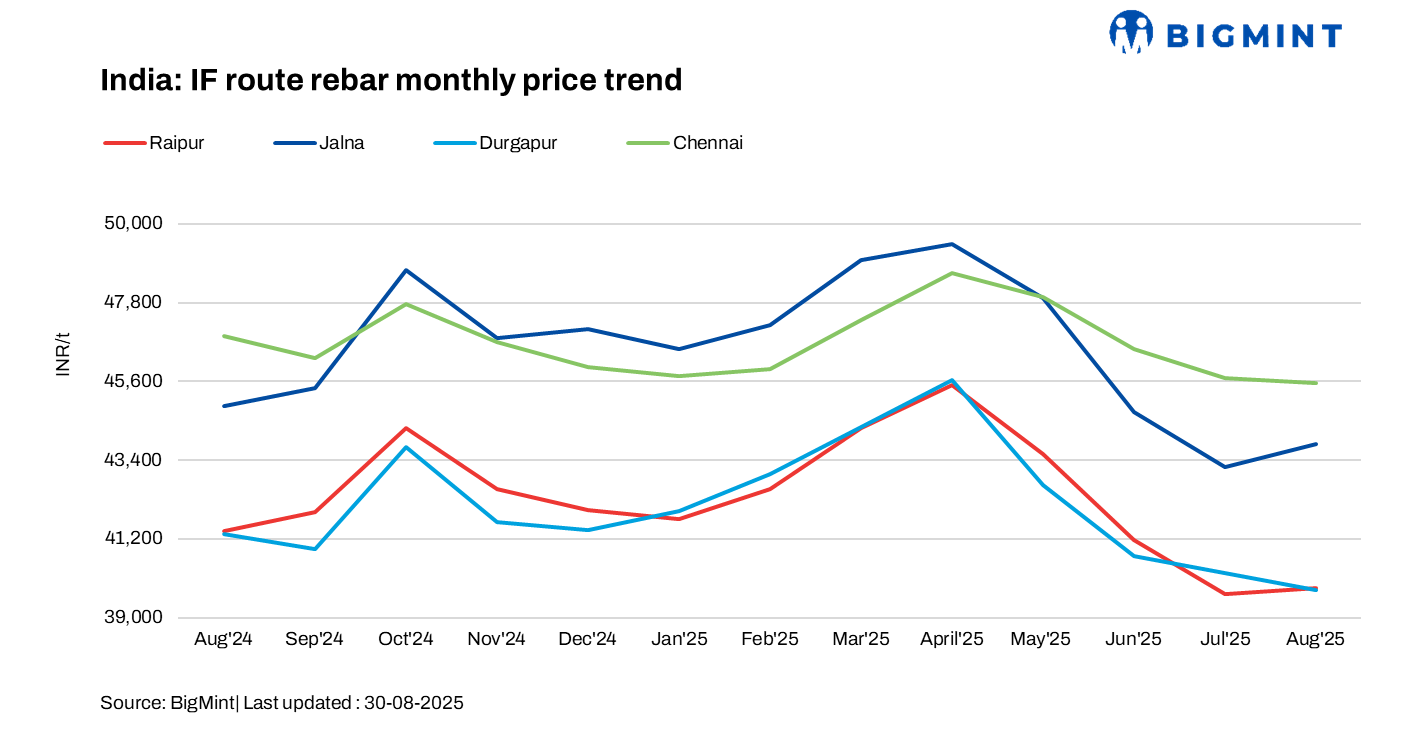

India’s induction furnace (IF) rebar prices witnessed a downtrend in August 2025, in the range of INR 200-2,700/tonne (t) m-o-m across regions, as per BigMint’s assessment.

The market faced a slowdown amid weak sentiment and limited customer inquiries, which resulted in sluggish order bookings. Purchases were restricted to immediate requirements, as buyers stayed cautious due to volatility in raw material prices — particularly sponge iron and billets — along with heavy monsoon rains and festival-related disruptions.

To stimulate sales and manage inventories, manufacturers reduced offers and extended trade discounts. Inventory levels increased to around 15-17 days in August from around 10-12 days in July.

As per Joint Plant Committee (JPC) data, India’s total rebar production through the IF and BF routes stood at 17.6 million tonnes (mnt) in April-July of FY’26, marking a significant 10% rise from around 16 mnt in the same period of FY’25, indicating continued growth momentum.

Region-wise price movements

Prices saw the most significant drops in the northern region. The Delhi market experienced a decrease of INR 2,700/t, while Jaipur saw a reduction of INR 1,500/t. The eastern region also witnessed a notable price drop, with Durgapur recording a reduction of INR 1,500/t.

In central India, prices experienced an INR 700/t decline in Raigarh, while Raipur, a major production hub, saw a more modest decrease of INR 200/t m-o-m. Additionally, markets in western India also saw a drop, with Ahmedabad prices down by INR 500/t.

In south India, the same trends prevailed. Hyderabad and Bangalore recorded declines of INR 2,000/t and INR 1,200/t m-o-m, respectively, while the Chennai market remained stable.

Factors impacting market

Raw material prices drop m-o-m: The drop in finished steel prices was largely driven by lower prices of key raw materials — steel billets and sponge iron — used in IF-route production. Dull buying interest and slow trade activity across several markets prompted manufacturers of both commodities to reduce their prices.

Considering Raipur as the benchmark, billet prices declined by INR 900/t m-o-m to INR 36,500/t exw, while sponge iron (PDRI FeM 80% ±1) saw a sharper decline of INR 1,500/t m-o-m to INR 23,100/t exw (prices taken from 31 July to 30 August 2025).

Demand slows down: The monsoon slowed down construction activities, prompting buyers to avoid bulk bookings and limit purchases to immediate needs. Festive holidays further contributed to the subdued pace of material procurement.

BF-route rebar prices drop m-o-m: Blast furnace (BF) route rebar prices declined by INR 700/t m-o-m in August 2025 to average INR 48,100/t exy-Mumbai, driven by weak trade channel demand. However, prices in the projects segment remained stable at INR 47,400/t FOR Mumbai. Market activity was muted as buyers adopted a cautious approach during the monsoon and festive week, while logistical hurdles further delayed projects and weighed on procurement.

Outlook

Domestic steel prices are likely to see a recovery, supported by firming raw material costs and the gradual withdrawal of the monsoon across several regions. A recovery in construction work will also help increase demand. With rebar prices already hovering at bottom levels, a rebound is expected very soon.

Leave a Reply