- Cautious buyer sentiment leads to price decline d-o-d

- Weak demand, oversupply pressure prices in Aug’25

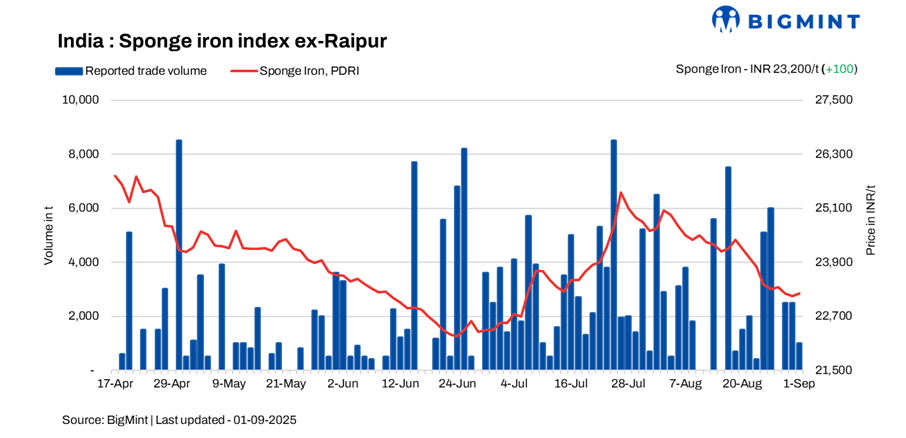

The Indian sponge iron market began September on a subdued tone, with prices declining by INR 50-150/t across major hubs. Durgapur witnessed the sharpest fall of INR 150/t, weighed down by restrained buyer participation.

- Market sentiment: Limited inquiries were observed, with buyers maintaining a wait-and-watch approach amid uncertainty in price direction.

- Deal volume: Confirmed deals totalled around 6,600 t, underscoring muted activity.

- Market activity: Both finished and semi-finished steel segments remained lacklustre, leading sponge iron transactions to be largely restricted to need-based buying.

- Buyer behaviour: Weak downstream demand reinforced buyer hesitation, keeping market confidence low.

Monthly recap – August 2025

The sponge iron market in India endured a weak August, with broad-based price corrections across all key trading regions. Subdued demand and regional oversupply drove the bearish sentiment, with elevated raw material costs pressuring margins.

M-o-m regional price movements

- Central India: Prices plunged INR 1,200-1,400/t, pressured by oversupply in the Raipur-Raigarh clusters, home to a dense concentration of sponge units.

- South India: A moderate fall of INR 200-400/t was seen, with prices cushioned by controlled production cuts that helped prevent steeper declines.

- East India: Prices corrected by INR 300-1,500/t across most hubs, except Durgapur, which saw an INR 800/t increase on localised demand and tighter supply.

Key factors behind price weakness in Aug’25

- Weak market demand: Weak demand from the construction and infrastructure sectors suppressed buying activity.

- Oversupply pressure: Central India’s high sponge production capacity led to inventory build-ups and aggressive price competition.

- Selling pressure: Producers, facing limited offtake, were compelled to liquidate stock at reduced rates.

- Monsoon impact: Heavy rainfall disrupted logistics and raw material supplies, delaying material movement and creating uncertainty.

Meanwhile, rising iron ore prices, as seen in the recent Odisha Mining Corporation (OMC) auctions, squeezed margins, leaving sponge iron producers struggling to maintain profitability.

Rationale

Prices have been derived based on transactions, offers, bids, and indicative price data sets. Transactions are considered as T1 and given a weightage of 50%, whereas other data sets are considered as T2 and given a weightage of the balance 50%.

Click here for detailed methodology

Leave a Reply