- Offers remain steady, but deals closed at lower values

- Sponge iron falls INR 100/t w-o-w, billet down INR 550/t

Pellet prices in the domestic market were largely stable to soft over the past few days, with buying activity observed to be moderate. Local suppliers held offers steady, but some deals were closed at lower values. Additionally, buyers continued to procure on a need basis.

Price movements, trades

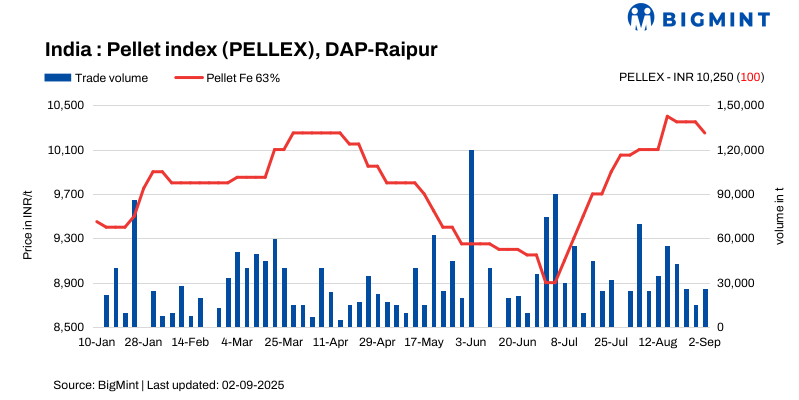

PELLEX, BigMint’s bi-weekly domestic pellet (Fe63%) index for Raipur, decreased by INR 100/tonne (t) to INR 10,250/t ($116/t) DAP on 2 September 2025 compared to the previous assessment on 29 August.

Raipur-based producers kept their offers for Fe63% (+/-0.5%) at INR 10,000-10,300/t ($113-117/t) exw. Deals for around 20,000 t were concluded at lower prices over the last couple of days by local pellet suppliers.

Odisha-based suppliers offered pellets at INR 9,900-10,400/t DAP in Raipur. Notably, 6,000 t were supplied by an Odisha-based seller to a local buyer.

A few deals were concluded from Odisha at slightly lower levels in Raipur, indicating weak demand in the domestic market, but confirmation from the transacted parties is still pending.

Market scenario

A market participant stated, “Buyers are only picking up material on a need basis, but suppliers are not aggressively reducing prices yet. There is no strong momentum in the market right now.”

Deal activity remained moderate, with some transactions done by steelmakers to cover immediate requirements. A few sellers were compelled to offload material at discounted levels due to mounting pressure from the downstream steel market, where prices remain under stress.

A buyer informed BigMint, “The steel market has been soft for the last couple of weeks, and this is directly impacting raw material sentiment. Pellet suppliers are finding it difficult to maintain margins.”

Market participants are now closely watching the upcoming NMDC price revision for September deliveries, which is expected to provide clearer direction for pellet trades. Steelmakers believe that prices could remain volatile in the near term, with some restocking activity likely once clarity emerges.

In the 29 August NMDC Chhattisgarh auction, 34,400-t DR CLO (Fe 67%) fetched a premium of up to INR 700/t, while 163,400-t fines (Fe 64%) remained unsold, though official confirmation is still awaited regarding the results. Prices are on FOR basis, inclusive of taxes.

Rationale

- PELLEX has been derived using data points, i.e., trades, offers, and bids. To download the detailed methodology, click here.

- Two (2) deals were reported in this publishing window, and one (1) was taken for calculation. Thus, the T1 trade category was accorded 50% weightage.

- Sixteen (16) firm offers, bids, and indicative prices were heard. Thirteen (13) were taken for price calculation and given a balance of 50% weightage.

Key market drivers

- Sponge iron tags fall w-o-w: P-DRI prices dropped by INR 100/t ($1/t) w-o-w to INR 23,200/t ($263/t) exw-Raipur on 29 August while remaining unchanged d-o-d. There was some recovery on the demand side, with increased bookings seen primarily by mills that had reduced their prices. However, not all sellers reduced their prices due to the high costs of raw pellets, and as a result, many were not making offers in the market.

- Billet prices drop w-o-w: Billet prices in Raipur declined by INR 550/t ($6/t) w-o-w to INR 36,450/t ($414/t) exw today. Prices decreased by INR 150/t ($2/t) d-o-d. Trading activity stayed limited, with spot offers coming under pressure amid persistent weakness in both semi-finished and finished steel segments. Buying was largely restricted to immediate requirements, as participants adopted a cautious stance amid bearish market sentiment.

Outlook

As per BigMint, Raipur pellet prices are expected to be volatile in the near term, with need-based deals expected. The pricing and dynamics of the pellet market are likely to be influenced by changes in downstream steel tags and revisions in NMDC iron ore rates.

Leave a Reply